A Look At Hershey’s (HSY) Valuation After Its Recent Share Price Momentum

Hershey Company HSY | 197.68 198.10 | +0.04% +0.21% Post |

With no fresh headline driving Hershey (HSY) today, the stock’s recent performance still stands out, with gains over the month, past 3 months, year to date, and the past year drawing investor attention.

Hershey’s recent 30 day share price return of 21.12% and 90 day share price return of 28.46%, against a 1 year total shareholder return of 49.44%, point to momentum building again after a softer multi year profile.

If this move has you thinking about where else capital could work hard, it might be a good time to check out 23 top founder-led companies as potential next ideas to research.

With Hershey trading at $229 against an analyst target of about $226.68 and an estimated intrinsic value implying roughly a 23% discount, you have to ask yourself: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 18% Overvalued

Against Hershey’s last close of $229, the most followed narrative pegs fair value near $194, framing today’s price as a premium to its long term cash flow outlook.

The Discount Rate is up slightly to about 6.96% from roughly 6.78%, which points to a marginally higher required return being applied in the model.

Revenue Growth has edged down slightly in the model to about 3.19% from roughly 3.24%, indicating a small trim to long-term top-line assumptions.

Want to see what kind of earnings power and margins are baked into that fair value, and how rich a future P/E the narrative leans on? The full story connects slower revenue growth, shifting profitability and a higher required return into one tight valuation puzzle.

Result: Fair Value of $194 (OVERVALUED)

However, there are still watchpoints here, including the risk of higher cocoa and tariff costs, or softer demand if value focused consumers pull back on treats.

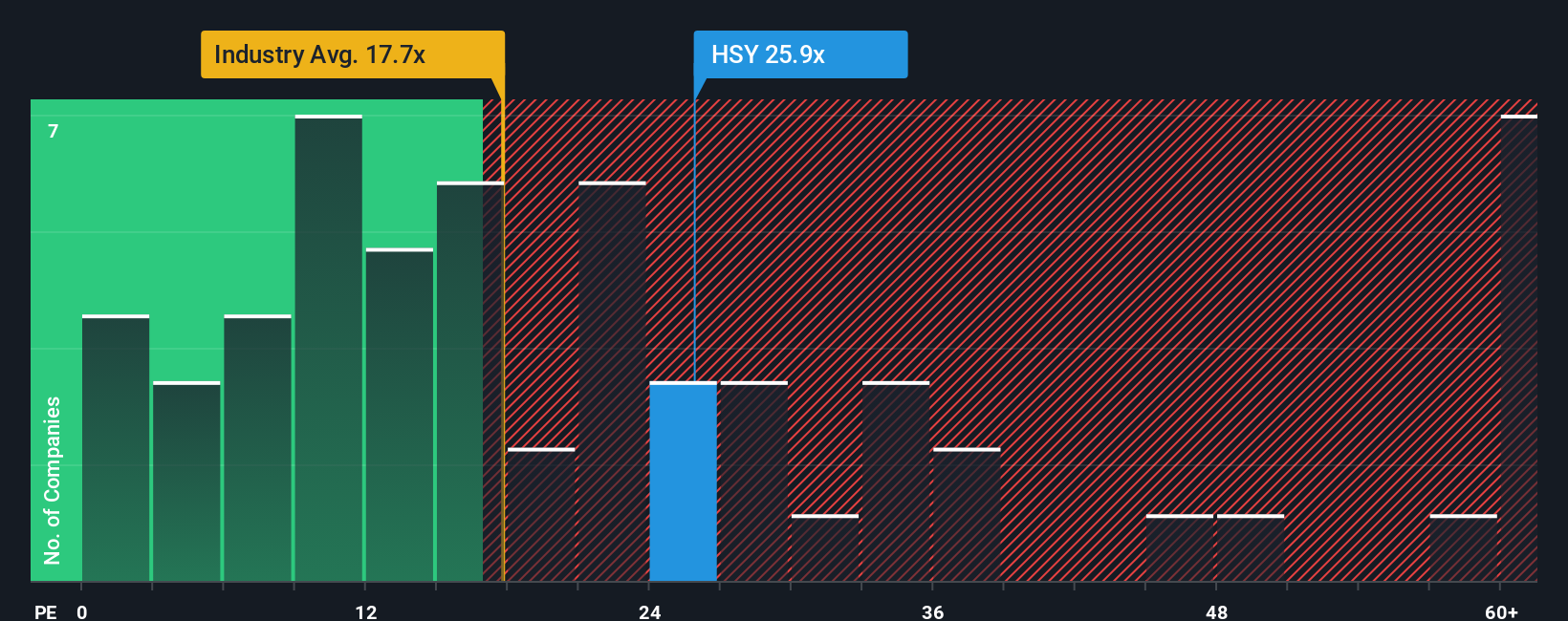

Another View: Earnings Multiple Flashes Caution

While our DCF model suggests Hershey at $229 is trading around 23% below an estimated future cash flow value of $299.03, the current P/E of 52.6x paints a very different picture. It sits well above both the fair ratio of 27.8x and the US Food industry average of 23.5x, as well as the 45x peer average. This introduces clear valuation risk if sentiment or growth expectations cool.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hershey for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Hershey Narrative

If you see the assumptions differently or prefer to work through the figures yourself, you can build and test your own Hershey story in minutes: Do it your way.

A great starting point for your Hershey research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you want to keep your portfolio ideas fresh and not stop at Hershey, use the Simply Wall St screener to spot other opportunities before everyone else.

- Target resilient value by checking companies our screener flags as 51 high quality undervalued stocks that might warrant a closer look.

- Prioritise stability and sleep better at night by scanning 83 resilient stocks with low risk scores that score well on our risk checks.

- Spot quality that others may be overlooking with a screener containing 24 high quality undiscovered gems that could deserve a place on your watchlist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.