A Look At IBM (IBM) Valuation After Recent Pullback And Long Term Return Profile

IBM Corp IBM | 0.00 |

Recent Share Performance and Business Mix

International Business Machines (IBM) has drawn investor attention after a recent pullback, with the stock showing negative returns over the past month and past 3 months and sitting below its year to date level.

At a last close of US$225.74 and a market value of about US$215.3b, the company combines sizeable revenue from software, consulting, infrastructure and financing. This provides several business drivers to watch within a single stock.

IBM’s recent momentum, including a 30 day share price return of 8.51% and a year to date share price return of -22.56%, contrasts with a 3 year total shareholder return of 102.31%. This indicates that long term investors have seen strong value creation despite the current pullback.

If you are weighing IBM’s recent pullback against trends in enterprise tech and AI infrastructure, it can help to compare it with peers using the 38 AI infrastructure stocks

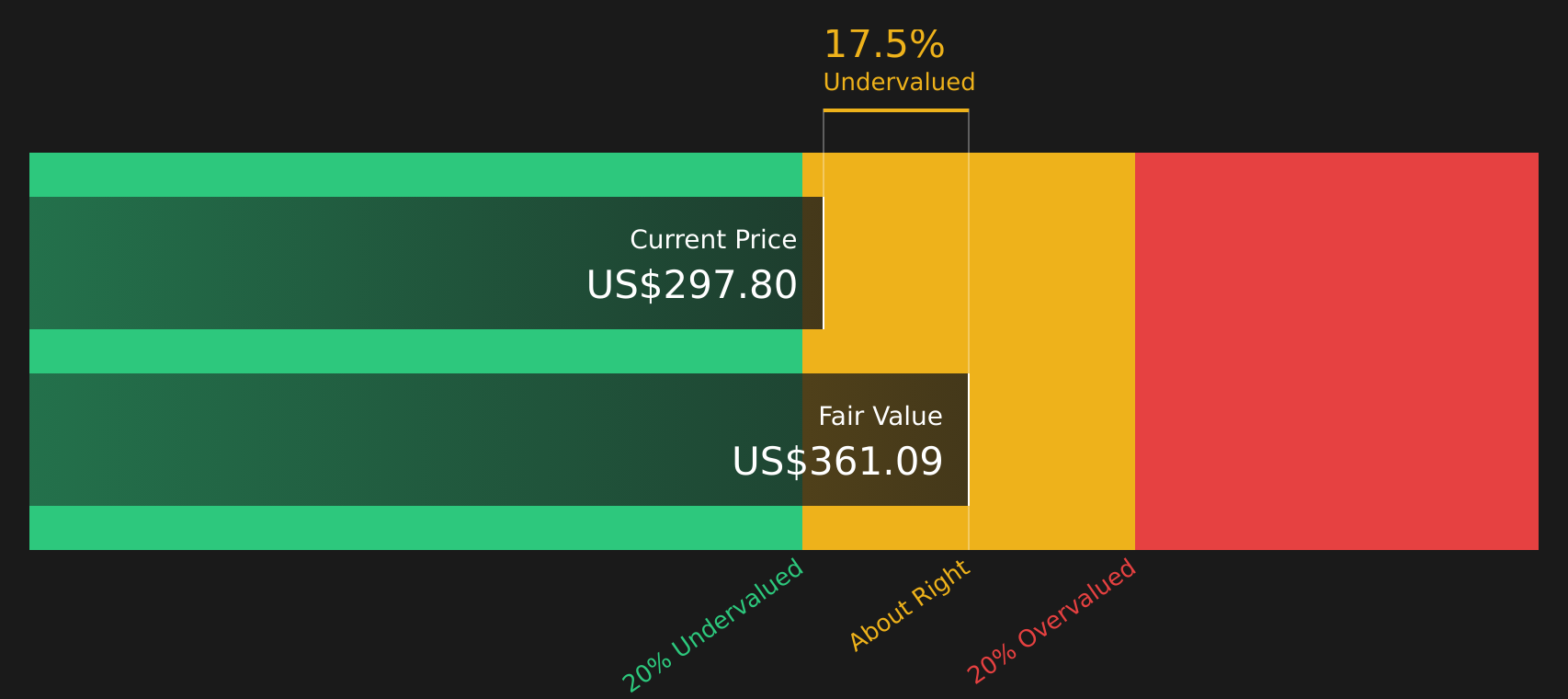

With IBM trading at US$225.74, an indicated intrinsic discount of 33.67% and a 23.23% discount to the average analyst price target, the key question is whether this gap signals an opportunity or if markets are already pricing in future growth.

Most Popular Narrative: 25.3% Undervalued

On the most followed narrative, IBM’s fair value sits at about $302 per share, comfortably above the last close of $225.74, with the gap tied to expectations around software, quantum and long term earnings power under a 9.70% discount rate.

IBM's focused strategy on hybrid cloud and AI is driving solid revenue growth, providing cost savings, productivity gains, and scalability for clients, which is expected to continue supporting their revenue trajectory.

The launch of the z17 mainframe with enhanced AI acceleration and energy efficiency is anticipated to drive significant customer adoption, positively impacting infrastructure revenue and possibly net margins due to differentiation and pricing power.

Curious what sits behind a fair value above $300 with only mid single digit growth forecasts, richer profit margins and a higher future earnings multiple baked in? The full narrative lays out how these moving parts combine into that 25% undervaluation call.

Result: Fair Value of $302.05 (UNDERVALUED)

However, this narrative can quickly be tested if software growth underwhelms or if macro pressures lead clients to delay discretionary consulting projects and cloud migrations.

Another Angle On Valuation

The SWS DCF model values IBM at about $340.34 per share, compared with the earlier fair value estimate of roughly $302 and the current price of $225.74. Both methods indicate undervaluation, but the DCF gap is wider. The central question is which set of assumptions you consider more reliable.

Next Steps

With mixed signals across valuation models and recent share performance, it may be helpful to review the numbers yourself and move quickly. To weigh up both sides properly, start by reviewing the 5 key rewards and 1 important warning sign

Looking for more investment ideas?

Do not stop your research at one stock. Broaden your watchlist with focused stock ideas that fit different goals, risk levels and income needs.

- Target potential upside by scanning a curated set of companies trading below their estimated worth using the 44 high quality undervalued stocks

- Strengthen your income stream by reviewing companies that offer higher yields and robust payout histories with the 12 dividend fortresses

- Prioritise capital preservation by checking companies with steadier risk profiles through the 74 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.