A Look At InterDigital (IDCC) Valuation After Q1 2026 Beat And Licensing Wins

InterDigital, Inc. IDCC | 0.00 |

InterDigital (IDCC) is back on investor radar after Q1 2026 results exceeded the company’s own guidance for revenue, adjusted EBITDA, and EPS, supported by fresh licensing deals with Xiaomi, LG, and Sony.

Despite Q1 results landing ahead of guidance and fresh licensing wins, the 7 day share price return of 21.17% and year to date share price return of 10.96% both point to fading short term momentum, while the 5 year total shareholder return of 342.02% shows a very strong longer term record.

If InterDigital’s recent volatility has your attention, it can be useful to see what else is moving in related areas, starting with 37 AI infrastructure stocks.

With Q1 beating guidance, annual revenue of US$828.924 million and net income of US$366.371 million, yet the share price retreating 21.17% over 7 days and 10.96% year to date, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 37.2% Undervalued

At a last close of $290.50 against a narrative fair value of $462.67, the widely followed thesis sees meaningful upside based on future licensing economics.

InterDigital now has leading smartphone manufacturers Apple and Samsung licensed through the end of the decade, covering almost 80% of the global smartphone market and bringing smartphone annualized recurring revenue (ARR) to a record $465 million, greatly enhancing revenue stability and reducing earnings volatility.

Want to see what underpins that confidence in recurring cash flows? The narrative leans heavily on projected revenue expansion, resilient profit margins, and a richer earnings multiple. Curious which assumptions really carry the valuation.

Result: Fair Value of $462.67 (UNDERVALUED)

However, that upside story leans heavily on smooth renewals and expansion beyond smartphones, while any setback in major deals or tighter licensing rules could quickly challenge it.

Another View: Cash Flows Point the Other Way

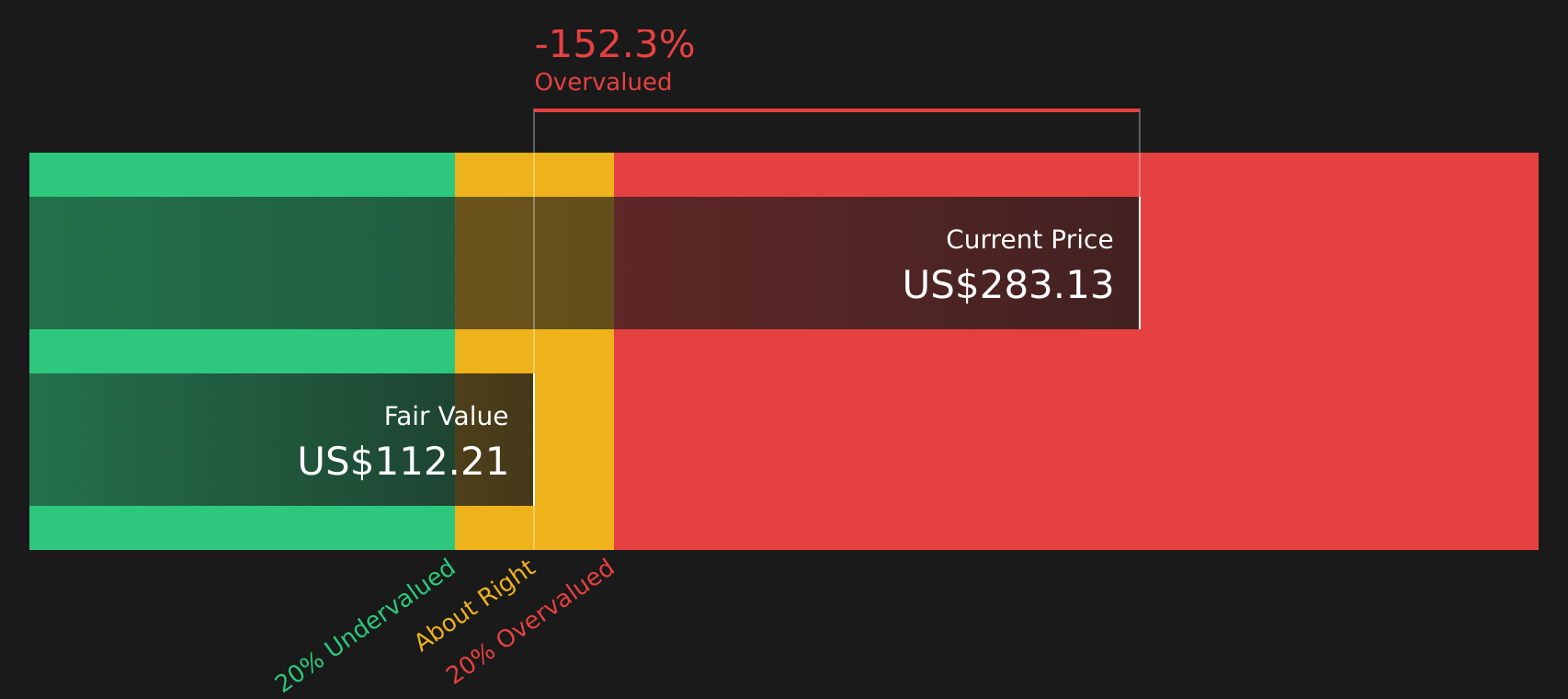

While the analyst narrative fair value sits at $462.67 and frames InterDigital as 37.2% undervalued, the SWS DCF model comes out far more cautious, with an estimate of $111.45. This would imply the shares are trading well above modeled future cash flows. That kind of gap raises a simple question: which story do you trust more, the earnings multiple or the cash flow math?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out InterDigital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such different signals on value and risk, it makes sense to look at the numbers yourself and decide where you stand, starting with 3 key rewards.

Looking for more investment ideas?

If InterDigital has sharpened your focus, do not stop here. Use the Simply Wall St Screener to find other ideas that could fit your portfolio.

- Target potential mispricings by scanning for companies that look underappreciated on quality and value using the 51 high quality undervalued stocks.

- Strengthen your income stream by hunting for companies with higher yields and resilient payouts through the 13 dividend fortresses.

- Prioritize resilience by filtering for businesses with robust finances and steady fundamentals in the solid balance sheet and fundamentals stocks screener (44 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.