A Look At Lam Research (LRCX) Valuation After Earnings Beat New CEA Leti Partnership And Erste Downgrade

Lam Research Corporation LRCX | 0.00 |

Lam Research (LRCX) is in focus after fiscal second quarter results surpassed expectations, a new CEA-Leti partnership on energy efficient chips, and an Erste Group downgrade that highlighted margin and software related risks.

At a latest share price of US$218.44, Lam Research has seen a 9.6% 1 month share price return and an 18.0% year to date share price return, while its 1 year total shareholder return above 200% points to strong momentum supported by upbeat earnings, the CEA-Leti partnership and sustained interest from AI and quantum focused funds despite the recent Erste Group downgrade.

If Lam Research has put AI hardware on your radar, it may be worth broadening your search with our screener featuring 36 AI infrastructure stocks

With Lam Research posting fiscal results above expectations, a fresh CEA-Leti partnership and a 1 year total shareholder return above 200%, the key question now is whether the current US$218.44 share price still leaves room for upside or if the market is already pricing in most of the future growth.

Most Popular Narrative: 20.5% Undervalued

Compared with the latest close at $218.44, the most followed narrative points to a fair value of about $274.90, framing Lam Research as materially undervalued using a 10.59% discount rate and long term cash flow assumptions.

Rapidly rising AI workloads and the associated need for higher storage, bandwidth, and processing power are accelerating the adoption of advanced chip architectures (such as gate-all-around, 3D NAND, and advanced packaging). This increases demand for Lam's etch and deposition tools, supporting sustained revenue growth and robust order visibility.

Want to see what sits behind that growth story? The narrative leans on compounded revenue gains, firm margins, and a future earnings multiple that assumes Lam keeps its equipment edge. The key question is how those ingredients line up to justify a fair value well above today’s price.

Result: Fair Value of $274.90 (UNDERVALUED)

However, this upbeat case still hinges on China demand holding up and a concentrated customer base maintaining current spending plans. Both of these factors could quickly weaken the thesis.

Another View: Cash Flows Paint a Tougher Picture

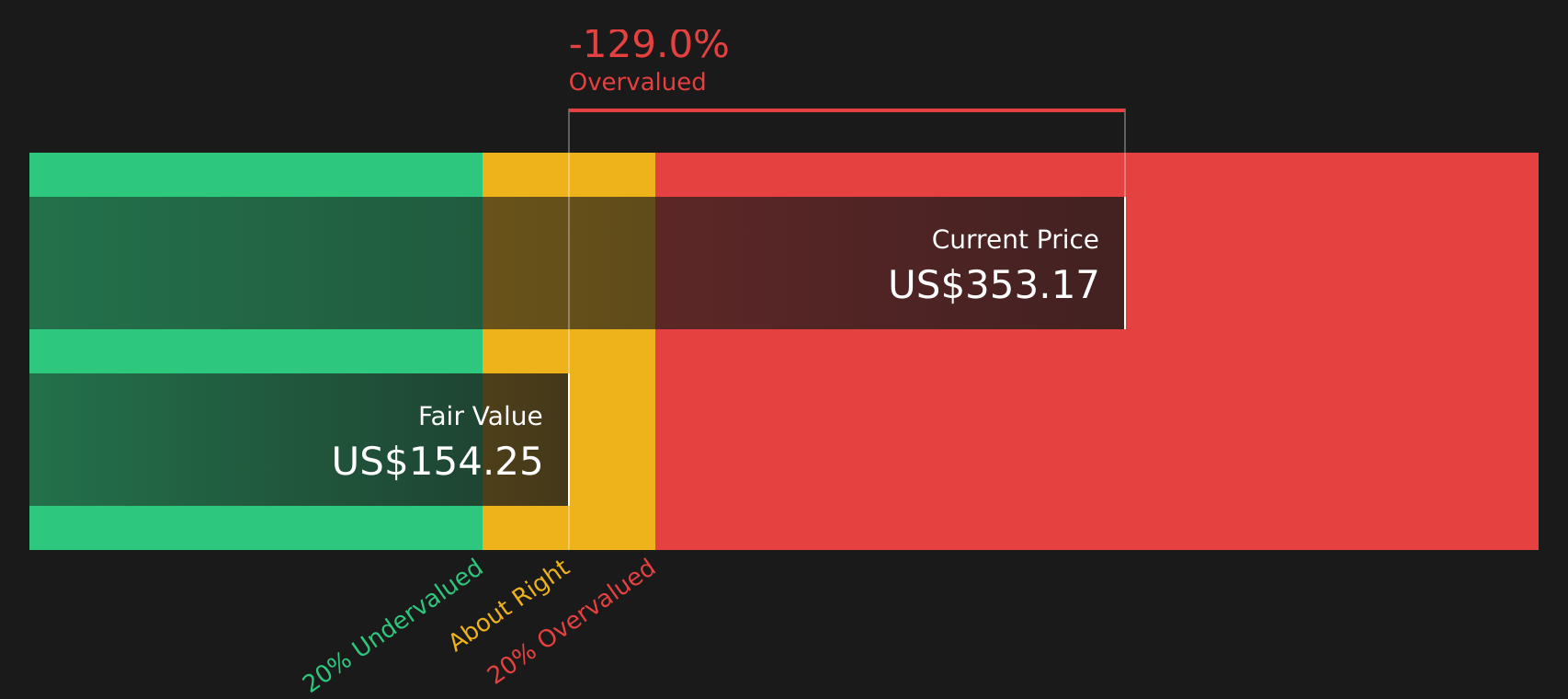

There is also a more conservative lens to consider. The SWS DCF model estimates Lam Research's future cash flows at about $114.63 per share, well below the current $218.44 price. This points to an overvalued outcome rather than the 20.5% undervalued narrative. Which story do you think fits your expectations better?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Lam Research for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 58 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed messages on value and risk so far? Take a moment to test the numbers yourself, then weigh up the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Lam Research has sharpened your interest, do not stop here; broaden your watchlist with a few focused stock ideas that match what you are looking for.

- Target resilient income by checking out 13 dividend fortresses that aim to combine higher yields with stability.

- Hunt for quality at a reasonable price by scanning 58 high quality undervalued stocks that pair strong fundamentals with attractive valuations.

- Stay on the front foot by reviewing 68 resilient stocks with low risk scores that rate well on balance sheet strength and business risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.