A Look At MGM Resorts (MGM) Valuation After Earnings Beat BetMGM Profitability And Record Macau EBITDAR

MGM Resorts International MGM | 38.36 38.36 | +4.44% 0.00% Post |

MGM Resorts International (MGM) is back in focus after posting fourth quarter earnings that topped analyst expectations, alongside a profitable year for its BetMGM joint venture and record EBITDAR in Macau.

The latest earnings beat and BetMGM profitability seem to have reset sentiment, with the 1 day share price return of 3.34% and 7 day share price return of 11.78% contributing to a 90 day share price return of 14.12%. However, the 3 year total shareholder return of a 14.46% decline shows longer term holders have had a tougher run.

If MGM's recent move has you thinking about where growth and risk might look different, it could be worth scanning our list of 22 top founder-led companies as a fresh starting point.

With earnings ahead of expectations, BetMGM turning profitable and the shares still trading below the average analyst price target, the key question is whether MGM is still undervalued or if the market is already pricing in future growth.Most Popular Narrative: 11.9% Undervalued

With MGM Resorts International last closing at $37.49 against a narrative fair value of $42.56, the gap in expectations is clear and centered on how future earnings, cash flows and capital allocation might play out.

The analysts have a consensus price target of $47.917 for MGM Resorts International based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $58.0, and the most bearish reporting a price target of $37.0.

Curious what assumptions bridge today’s earnings to that higher fair value and price target range? The narrative leans heavily on earnings growth, margin expansion and a richer future earnings multiple, all under a specific discount rate and buyback path that you can only fully see inside the full write up.

Result: Fair Value of $42.56 (UNDERVALUED)

However, you still need to weigh the risk that heavy long dated projects like Osaka or Dubai, as well as softer Las Vegas visitation, could derail those upbeat assumptions.

Another View: Market Multiple Sends a Different Signal

Our fair value estimate of $42.56 suggests MGM Resorts International is 11.9% undervalued on the narrative model, but the market is telling a different story when you look at the P/E ratio.

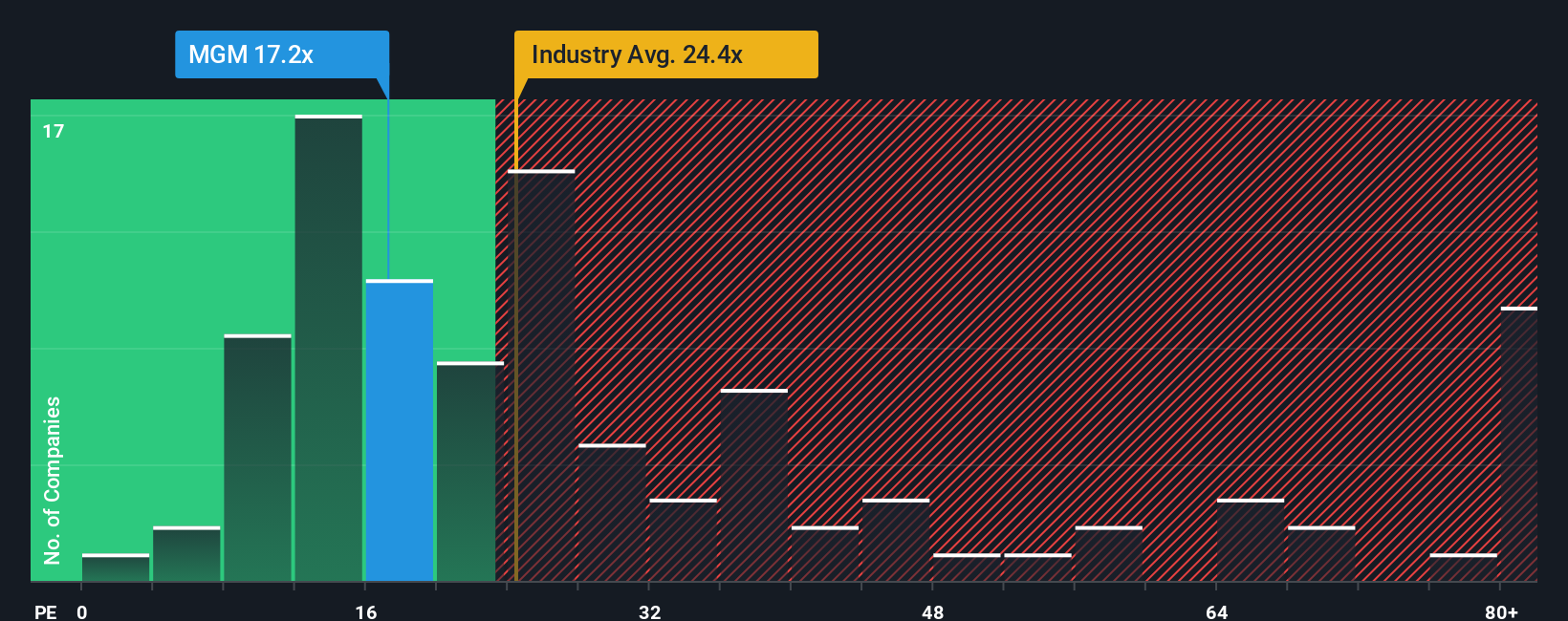

On current earnings, MGM trades on a P/E of 47x, compared with a fair ratio of 27.1x, the US Hospitality industry at 22x and a peer average of 16x. That gap points to meaningful valuation risk if expectations reset, so the question is whether you think MGM's earnings profile justifies paying that kind of premium.

Build Your Own MGM Resorts International Narrative

If this version of the story does not quite fit how you see MGM, you can stress test the numbers yourself and shape a fresh narrative in minutes: Do it your way.

A great starting point for your MGM Resorts International research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If MGM has sharpened your focus, do not stop here. The next compelling opportunity could be sitting just a couple of filters away in the Screener.

- Target quality at a discount by scanning our list of 52 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect them yet.

- Prioritise resilience by reviewing 82 resilient stocks with low risk scores, where companies score well on financial health and business risk so you can focus on staying invested with fewer surprises.

- Get ahead of the crowd by checking our screener containing 24 high quality undiscovered gems, highlighting underfollowed names that still pass strong fundamental checks before they land on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.