A Look At Oracle (ORCL) Valuation After Major AI Contracts And Strong Q3 FY2026 Results

Oracle Corporation ORCL | 0.00 |

Oracle (ORCL) is back in focus after a series of AI and cloud announcements, including defense contracts for classified environments, strong Q3 FY2026 revenue and backlog figures, and fresh customer wins with Ishan Technologies and Samsung.

Those AI and cloud headlines are arriving after a sharp run, with Oracle’s share price gaining 13.63% over the past month and 20.49% over 90 days, while its 1-year total shareholder return of 21.43% and 5-year total shareholder return of 161.23% point to momentum that has built over time rather than just on recent news.

If Oracle’s AI push has your attention, it can be worth widening your radar to other companies building the infrastructure behind AI. You can start with 42 AI infrastructure stocks

With Q3 FY2026 revenue of US$17.19b, annual revenue growth of 28.45%, and an intrinsic value estimate that sits about 36% above the current US$192.95 share price, is Oracle still mispriced or already reflecting years of AI driven growth?

Most Popular Narrative: 50.5% Undervalued

Oracle’s most followed narrative pegs fair value at $389.81 per share, compared with the last close at $192.95. This frames the AI contract surge in a very different light.

The story of Oracle’s transformation is a narrative of strategic repositioning that has culminated in the company emerging as an indispensable infrastructure partner for the world’s most demanding Artificial Intelligence (AI) workloads. This strategic shift, defined by massive infrastructure investment, a landmark partnership with OpenAI, and the rise of colossal superclusters, has driven an unprecedented surge in its contract backlog, fundamentally reshaping Oracle’s long-term growth trajectory and competitive landscape.

Want to understand why this narrative points to such a gap between price and fair value? According to TickerTickle, the thesis leans heavily on aggressive contract-backed growth, rising AI infrastructure usage and ambitious margin assumptions tied to Oracle’s full stack model. The tension between those projections and today’s share price is where the story gets interesting.

Result: Fair Value of $389.81 (UNDERVALUED)

However, this hinges on Oracle actually delivering capacity fast enough and on AI projects avoiding the high failure rates that could cool today’s contract-driven enthusiasm.

Another Angle on Value

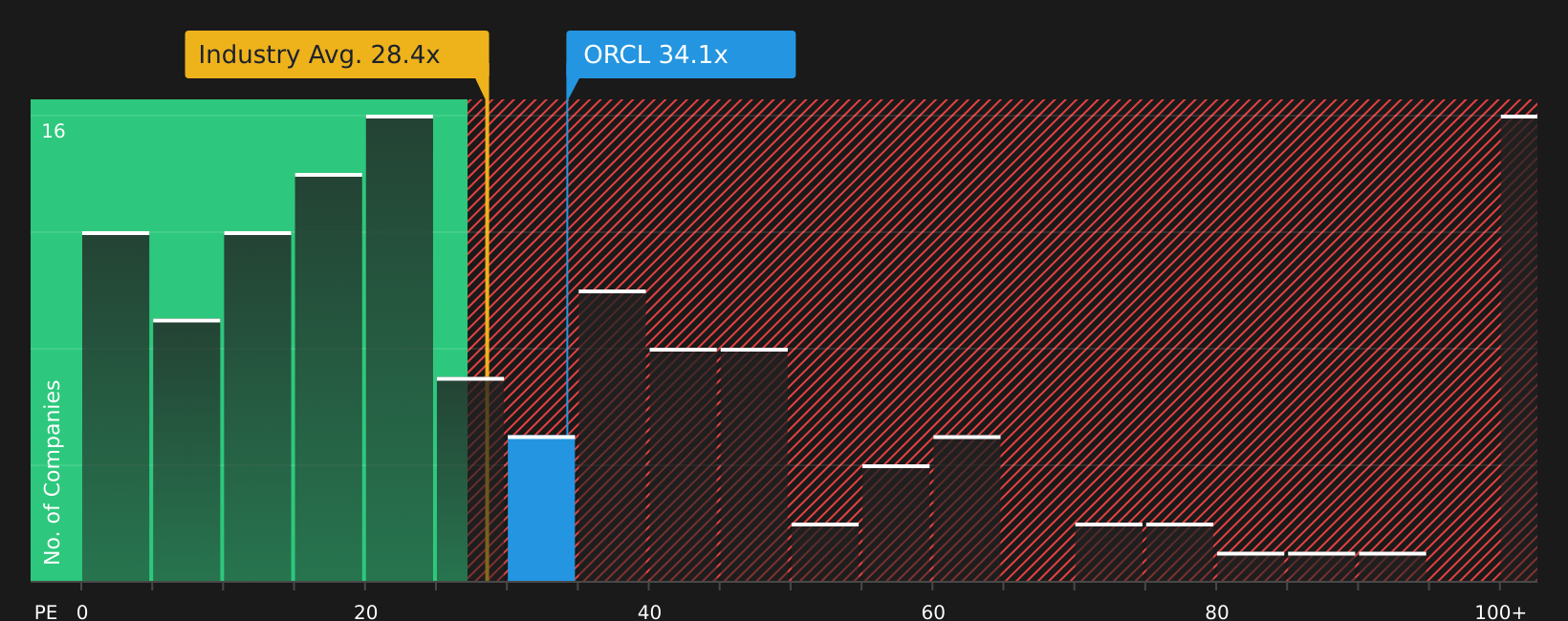

Oracle screens as expensive on a P/E of 34.3x compared with the US Software industry at 28.4x, yet cheaper than a peer average of 70.1x and below an estimated fair ratio of 61.2x. That mix of premium and discount raises a simple question: how much valuation risk are you really taking here?

For a closer look at how these comparisons stack up and what the fair ratio suggests the market could move toward over time, check out See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals across valuation, AI growth, and contract momentum, the sentiment is far from settled. Consider acting promptly and weighing the balance of risks and rewards for yourself by checking the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop at Oracle, you could miss other stocks that fit your style, so put the Simply Wall Street Screener to work and expand your watchlist.

- Target potential mispricings by scanning 50 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their financial profile.

- Build a smoother ride for your portfolio by checking 66 resilient stocks with low risk scores where company risk scores sit on the lower side.

- Get ahead of the crowd by searching screener containing 22 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.