A Look At Palomar Holdings (PLMR) Valuation After New US$450 Million Credit Facility And Q4 2025 Earnings Setup

Palomar Holdings PLMR | 130.03 130.03 | -0.66% 0.00% Pre |

Palomar Holdings (PLMR) heads into its Q4 2025 earnings release today at 4:00 PM Eastern, shortly after securing a new US$450 million unsecured credit facility that increases its financial flexibility and funding options.

The stock has picked up near term momentum, with a 1 day share price return of 2.14% and 7 day share price return of 6.04%. The 1 year total shareholder return of 17.16% sits against a much stronger 3 year total shareholder return of about 7x, which hints that the recent move is building on a longer period of strong compounding rather than starting a new trend from scratch.

If Palomar’s latest financing and earnings setup has you thinking more broadly about where growth could come from next, it might be worth scanning 23 top founder-led companies as a way to uncover other potential compounders with aligned management incentives.

With earnings expectations high, a US$450 million credit line in place, and the shares trading below analyst price targets and some intrinsic value estimates, is Palomar still underappreciated, or is the market already pricing in the next leg of growth?

Most Popular Narrative: 19.6% Undervalued

With Palomar Holdings last closing at $129.25 against a narrative fair value of about $160.67, the widely followed model leans toward a meaningful valuation gap built on specific growth, margin, and discount rate assumptions.

Ongoing investment in proprietary technology, data analytics, and advanced underwriting disciplines is improving risk assessment and pricing accuracy, already reflected in strong combined ratios and low loss ratios, which should continue to enhance underwriting profitability and expand net margins over time.

Curious what kind of revenue pace, earnings trajectory, and future P/E multiple need to line up for that fair value to hold? The narrative leans on ambitious top line growth, firm but slightly slimmer margins, and a premium earnings multiple that still sits above the sector. If you want to see exactly how those pieces fit together, the full story lays out the numbers in plain view.

Result: Fair Value of $160.67 (UNDERVALUED)

However, investors still need to weigh catastrophe exposure, which could hit earnings in a bad year, and the risk that tougher reinsurance terms could squeeze future margins.

Another Way to Look at Valuation

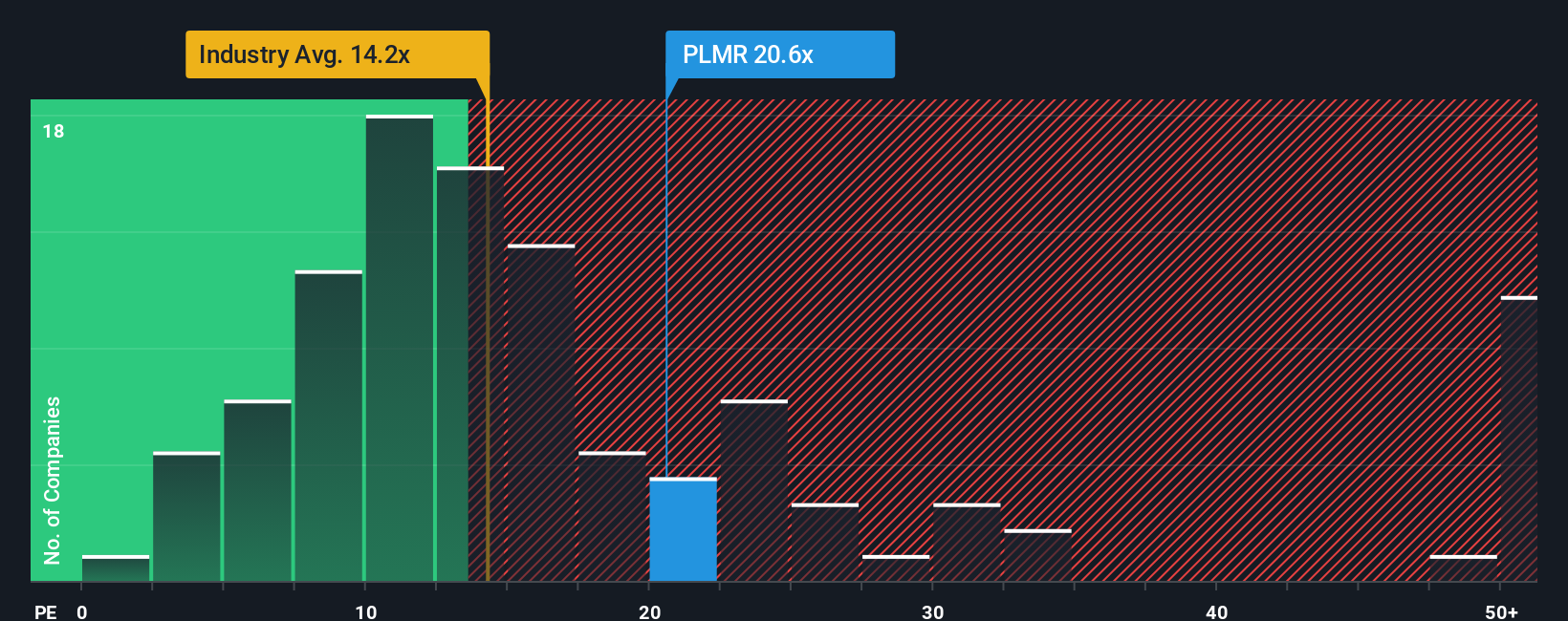

The narrative and DCF style work suggest Palomar is undervalued, but the market is asking you to pay a P/E of 19.5x. That is well above the US Insurance industry at 12.6x, the peer average at 8.5x, and even the fair ratio of 15.2x. This points to clear valuation risk if expectations cool.

Build Your Own Palomar Holdings Narrative

If you look at the assumptions and think the story should read differently, you can test the data yourself and shape a version that fits your view in just a few minutes, Do it your way.

A great starting point for your Palomar Holdings research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Palomar has sharpened your focus, do not stop here. Use the screener to compare different types of opportunities and pressure test your next move.

- Target long term value by scanning companies trading below their estimated worth with 51 high quality undervalued stocks which already filters for quality fundamentals.

- Strengthen your downside protection by reviewing businesses with robust finances through solid balance sheet and fundamentals stocks screener (45 results) which highlights resilient balance sheets and cash flows.

- Boost your income research by checking reliable payout ideas inside 14 dividend fortresses which focuses on higher yielding companies with staying power.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.