A Look At Philip Morris International’s Valuation As Smoke Free Growth And Regulatory Catalysts Gain Attention

Philip Morris International Inc. PM | 0.00 |

What PMI’s $1.5b bond issue means for equity investors

Philip Morris International (PM) has been in focus after issuing US$1.5b in new notes, a move that sits alongside growing smoke free revenues, fresh earnings guidance and potential regulatory shifts around nicotine products.

The bond issue and updated earnings guidance come after a mixed few months for the stock, with a 6.36% 30 day share price return partly offsetting a 6.30% 90 day share price decline. At the same time, the 3 year total shareholder return of about 105% and 5 year total shareholder return of about 125% highlight how sentiment around the smoke free transition and recent regulatory signals has been building over a longer period.

If Philip Morris International’s shift toward smoke free products has your attention, it can be useful to compare it with other consumer facing businesses that still have founder level oversight and long term focus. This could be a good time to broaden your search with the 21 top founder-led companies

With the stock up over 6% in the past month but roughly flat over 1 year, and smoke free products now a major revenue driver, a key question is whether Philip Morris International is undervalued at this level or whether the market is already pricing in future growth.

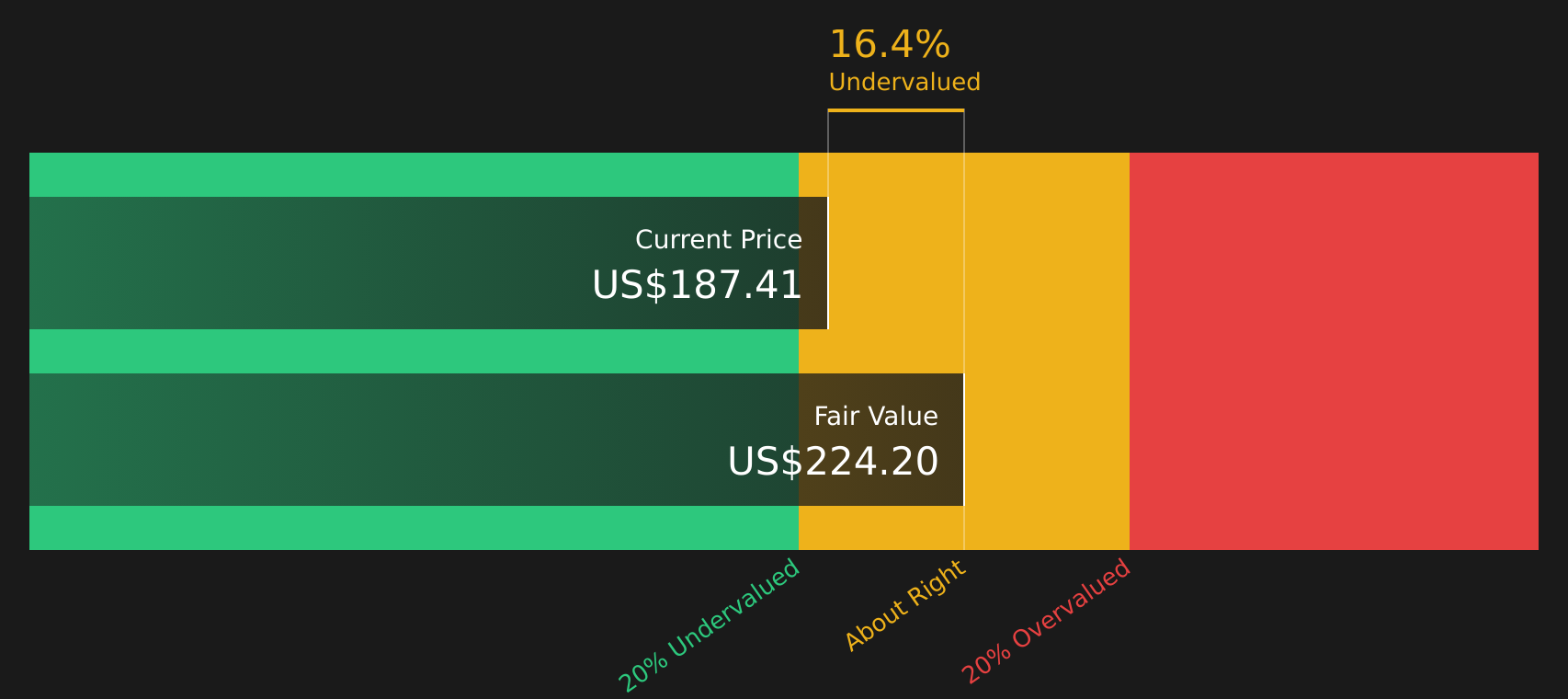

Most Popular Narrative: 11.5% Undervalued

With Philip Morris International last closing at $170.53 against a most-followed fair value estimate of $192.60, the narrative centers on whether smoke free momentum and earnings resilience justify that higher number.

The accelerating global adoption of smoke-free alternatives, driven by increasing health awareness and regulatory moves away from combustibles, is fueling strong double-digit volume and margin growth in PMI's IQOS, ZYN, and VEEV platforms. This secular shift enables the company to capture new consumer segments, expand its addressable market, and structurally boost net revenues and operating margins over time.

Want to see how this shift translates into that higher fair value? The narrative leans heavily on earnings, margins, and a richer future profit multiple. The discount rate and growth path are already mapped out. The question is whether you agree with the scale of that step up.

Result: Fair Value of $192.60 (UNDERVALUED)

However, this hinges on smoke free growth holding up and regulatory or tax changes not tightening faster than analysts currently build into their models.

Another Angle on Value

The popular fair value estimate of $192.60 leans on earnings forecasts and a richer future profit multiple, but Simply Wall St’s own discounted cash flow view is more cautious, with a value of $159.73 versus a recent price around $169.46. So which story do you think fits PMI better: a higher earnings multiple or a lower cash flow value?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Philip Morris International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 48 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment split between opportunity and caution, this is a moment to move quickly, review the numbers for yourself, and weigh up the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If PMI is on your radar, do not stop there. Use this moment to line up your next ideas before the market moves without you.

- Target resilient performers with 73 resilient stocks with low risk scores and reduce the chance that a single stock decision dominates your results.

- Spot potential bargains early by scanning the 48 high quality undervalued stocks and see which stocks the numbers suggest are trading below their fundamentals.

- Strengthen your income stream by reviewing the 13 dividend fortresses and focus on companies combining higher yields with a focus on consistency.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.