A Look At Procter & Gamble’s Valuation As Dividends Rise And Disaster Relief Partnership Expands

Procter & Gamble Company PG | 0.00 |

Why P&G’s steady dividends and social initiatives are drawing attention

Procter & Gamble (PG) is back on investor radars after lifting its dividend by 3% for the 70th consecutive year and deepening a disaster response partnership alongside Walmart and Matthew 25: Ministries.

Despite the long dividend streak and growing disaster response presence, recent price action has been soft, with the stock down over the past quarter and year, while longer term total shareholder returns over three and five years remain positive. This suggests that momentum has cooled after earlier gains.

If you want to broaden your watchlist beyond consumer staples, this could be a useful moment to check out 20 top founder-led companies

With the stock down over the past year despite ongoing dividends and an indicated intrinsic discount, the key question is whether you are seeing a solid consumer staples company on sale or whether the market already reflects its future growth.

Most Popular Narrative: 15.8% Overvalued

According to the most followed valuation narrative, Procter & Gamble's fair value sits at $121.06, compared with the last close of $140.19.

Procter & Gamble, despite being within a very competitive industry, still has some competitive advantages shown in its higher operating margin above the ~20% mark and the Morning Star Wide Moat. Also, the fact that the ROIC is double the Cost of Capital means its capital allocation is being well managed.

The narrative leans heavily on strong margins, a wide moat rating, and returns comfortably above the discount rate, yet still points to a lower fair value. It is worth examining which revenue, cash flow, and payout assumptions pull that number down from today’s share price.

Result: Fair Value of $121.06 (OVERVALUED)

However, this overvaluation case could be challenged if Procter & Gamble sustains its recent revenue and net income growth, or if market sentiment lifts consumer staples valuations.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

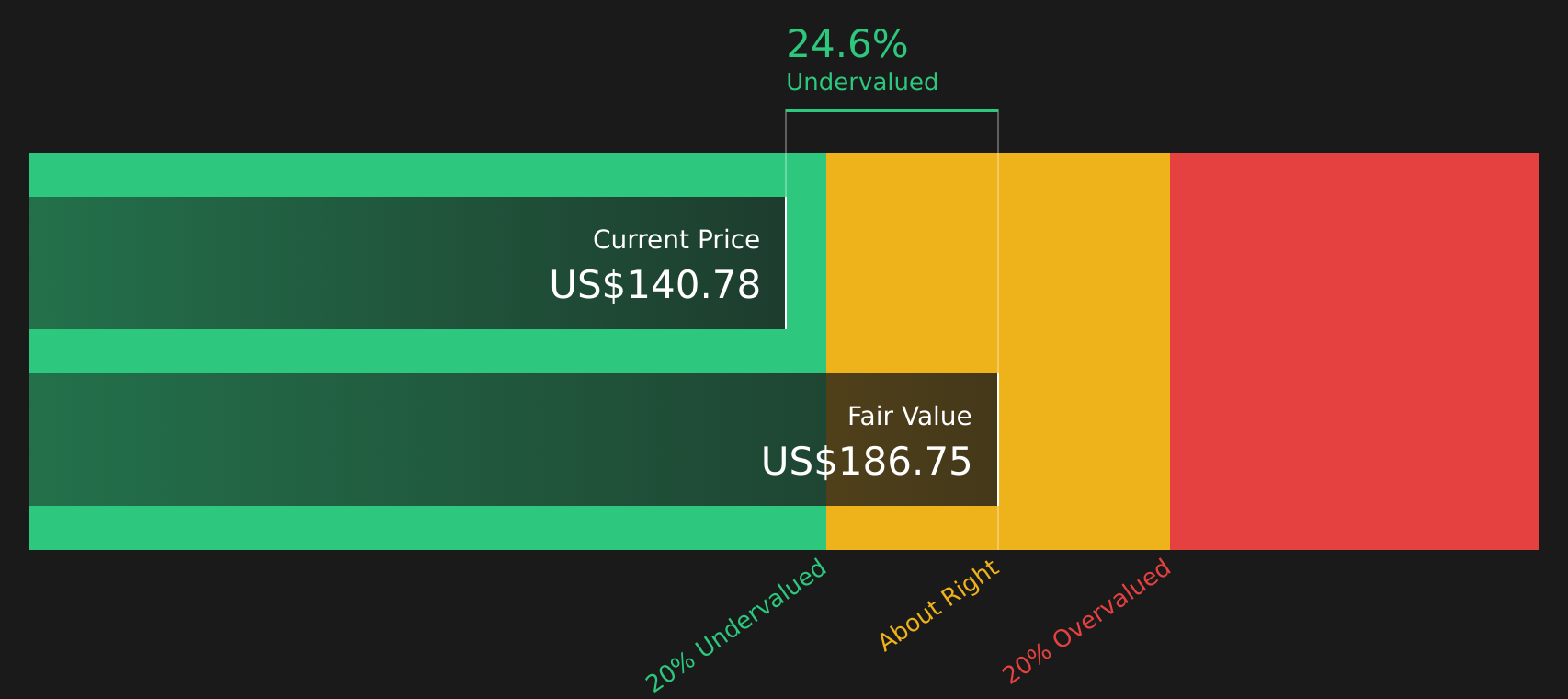

Another angle on value: SWS DCF model

While the user narrative points to a fair value of $121.06 and an overvalued stock, the Simply Wall St DCF model tells a very different story. It calculates an estimated future cash flow value of $186.75, putting the current $140.19 price at a 24.9% discount. Which set of assumptions do you find more convincing?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Procter & Gamble for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing mixed signals on Procter & Gamble so far? Take a closer look at the data, evaluate both the potential upsides and the concerns, and then review the 4 key rewards and 1 important warning sign

Ready for more investment ideas?

Once you have a view on Procter & Gamble, do not stop there. Broaden your opportunity set and let data driven filters surface stocks that fit your style.

- Target potential upside by scanning 47 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their underlying metrics.

- Strengthen your income focus by checking 10 dividend fortresses that pair higher yields with an emphasis on stability.

- Prioritize resilience by reviewing 63 resilient stocks with low risk scores designed to highlight companies with lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.