A Look At Rackspace Technology (RXT) Valuation After AMD AI Partnership And Return To Profitability

Rackspace Technology, Inc. RXT | 0.00 |

Rackspace Technology (RXT) has drawn fresh attention after two closely timed events: a new multiyear partnership with AMD focused on an Enterprise AI Cloud for regulated workloads, and first quarter 2026 results showing a return to profitability.

The share price has reacted sharply to these updates, with a 1 day share price return of 26.34%, a 7 day share price return of 107.10%, and a 30 day share price return that is almost 5x. At the same time, the 1 year total shareholder return of 478.57% and 3 year total shareholder return of 495.10% point to strong momentum from a longer term base, despite a 5 year total shareholder return that declined 63.82%.

If this kind of AI focused move has caught your eye, it could be worth seeing how other specialized AI infrastructure stocks are trading through our 40 AI infrastructure stocks

With Rackspace now back in profit and the AMD AI partnership in place, you are looking at a stock with sharp recent gains and mixed long-term returns. The key question is whether there is still upside potential or whether the market is already pricing in any future growth.

Most Popular Narrative: 236.5% Overvalued

Rackspace Technology's most followed narrative points to a fair value of about $2.17 per share, compared with the latest close at $7.29, which sets up a clear tension between model and market.

Expansion of higher-value Professional Services, Elastic Engineering, and AI-driven service offerings (e.g., CloudOps, FAIR) is accelerating the mix shift away from low-margin infrastructure resale toward recurring, higher-margin services, positively impacting gross margins and operating profit.

There is a detailed playbook behind that fair value. It blends modest revenue growth, improving margins, and a low implied future earnings multiple. The mix of assumptions matters more than any single headline.

Result: Fair Value of $2.17 (OVERVALUED)

However, there are still clear pressure points, including declining Public and Private Cloud revenues and ongoing margin compression, that could challenge the optimistic fair value story.

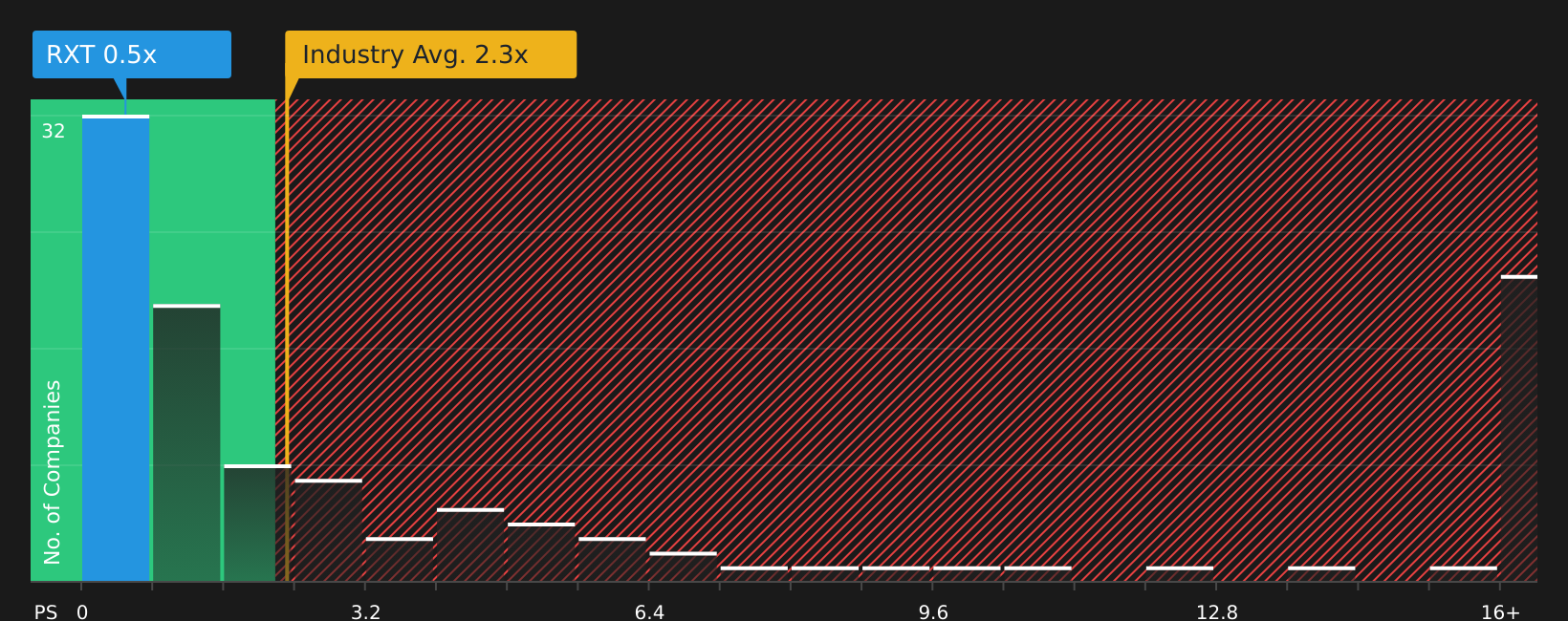

Another View: Market Price Versus Sales Based Valuation

That $2.17 fair value comes from the narrative model, but the preferred yardstick in the checks is the P/S ratio. On this measure, Rackspace trades at about 0.7x sales, compared with 2x for the US IT industry and 5.3x for peers, and a fair ratio of 1.9x. If the market is already paying far less per dollar of sales than both peers and that fair ratio, is the overvalued label telling the whole story or just one side of it?

Next Steps

With sentiment this mixed, you do not need to wait for a consensus to form. Instead, use the full breakdown of 1 key reward and 4 important warning signs

Looking for more investment ideas?

If you stop at a single stock, you could miss other opportunities that fit your style, so consider putting a few more names on your radar using focused screeners.

- Target value by hunting for companies that combine quality fundamentals with prices that may not fully reflect them through the 47 high quality undervalued stocks

- Strengthen your income stream by checking out stocks that pair higher yields with resilience using the 13 dividend fortresses

- Protect your downside first by scanning for companies with lower risk profiles through the 67 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.