A Look At Robinhood Markets (HOOD) Valuation After Q4 Revenue Miss And Crypto Trading Slump

Robinhood HOOD | 86.85 | -0.54% |

Robinhood Markets (HOOD) is back in focus after its fourth quarter earnings missed revenue expectations, with a 38% drop in crypto transaction revenue and softer trading activity weighing on near term sentiment.

That revenue miss and 38% drop in crypto transaction revenue hit sentiment hard, with the share price falling 30.1% over the past month and 35.7% over 90 days. This comes even though the 1 year total shareholder return is 25.7% and the 3 year total shareholder return is roughly 7x, which points to fading near term momentum following a very strong multi year run.

If volatility around Robinhood has you looking wider, this could be a good moment to see what else is moving. You can check out 16 cryptocurrency and blockchain stocks for other crypto exposed names on your radar.

With Robinhood now trading well below recent analyst targets, yet still carrying a premium valuation score of 0 and an intrinsic discount flag of roughly 61% over fair value, you have to ask: is this a fresh entry point, or is the market already baking in future growth?

Most Popular Narrative: 61% Undervalued

At $75.97, the most followed narrative on Robinhood Markets pegs fair value at $194.61, which frames the recent pullback in a very different light.

Robinhood (NASDAQ: HOOD) is no longer just the app that eliminated trading commissions. Over the past few years, the company has been reshaping itself into a broader financial platform, one that blends investing, cash management, derivatives, and crypto under a single consumer-facing interface. That evolution has helped Robinhood reignite growth, but it has also raised new questions. As product complexity increases, so does the importance of monetization quality, user behavior, and regulatory discipline. The company’s future depends less on attracting new users and more on how effectively it deepens engagement with existing ones.

Curious what justifies that gap between price and fair value? The narrative leans heavily on accelerating monetization, richer per user economics, and a profitability profile more often associated with much larger brokers. Want to see which growth, margin, and valuation assumptions support that conclusion? Read the full breakdown behind this fair value call.

Result: Fair Value of $194.61 (UNDERVALUED)

However, sustained revenue dependence on trading activity and crypto cycles, along with tightening regulatory scrutiny around tokenization, could quickly challenge the thesis that the stock is 61% undervalued.

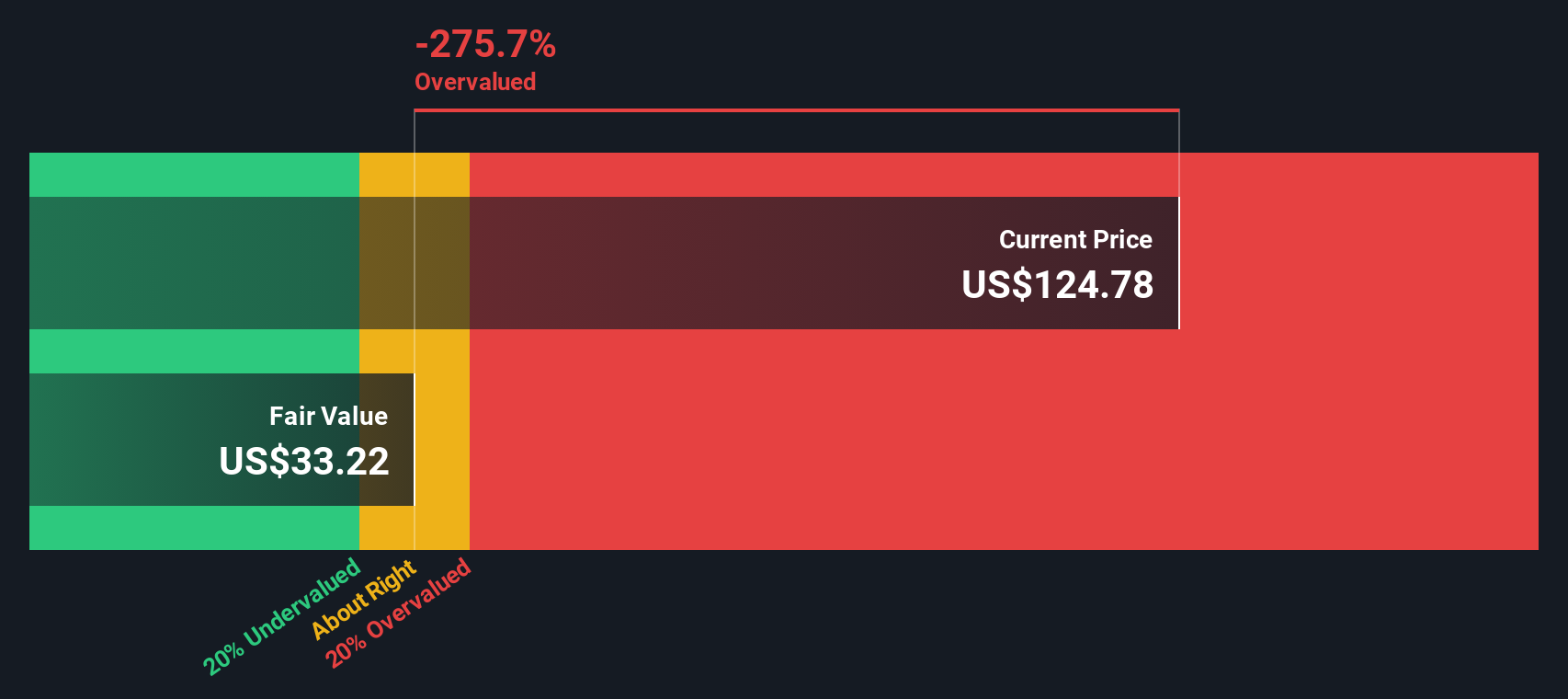

Another View: Pricing Signals Look Very Different

The user narrative leans on a $194.61 fair value, but the SWS DCF model tells a different story. At $75.97, Robinhood sits above an estimated future cash flow value of $47.10, which frames the shares as overvalued on that lens. Which story feels closer to how you invest?

Next Steps

If the split views in this article feel mixed to you, that is exactly the point.

Looking for more investment ideas?

If this Robinhood story has you thinking more broadly about your portfolio, use this moment to scan fresh ideas before the next wave of opportunities moves without you.

- Target value first and see which companies make the cut in our 55 high quality undervalued stocks built from fundamentals, cash flows and balance sheet strength.

- Prioritize resilience and check out the 81 resilient stocks with low risk scores to focus on companies that score well on financial health and business stability.

- Spot earlier stage opportunities by reviewing our 29 elite penny stocks with strong financials that combine smaller market caps with more robust underlying metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.