A Look At Waste Management (WM) Valuation After Solid Q1 2026 Earnings And Reaffirmed Full Year Targets

Waste Management, Inc. WM | 0.00 |

Waste Management (WM) just posted first quarter 2026 results that featured higher sales, net income and earnings per share, supported by stronger operating EBITDA, expanded margins, renewable energy growth and increased free cash flow funding dividends and buybacks.

Despite the solid first quarter update, Waste Management’s recent price action has been fairly muted. The 30 day share price return shows a 3.22% decline and the year to date share price return is 4.33%, while total shareholder return sits at 71.94% over five years, indicating that longer term momentum remains intact.

If this earnings story has you thinking about where to find the next opportunity in infrastructure linked themes, it could be worth scanning 36 power grid technology and infrastructure stocks

With the stock easing 3.2% over the past month yet still up year to date, and trading only modestly below some intrinsic value estimates, the key question is simple: is there still upside here, or has the market already priced in future growth?

Most Popular Narrative: 10% Undervalued

At a last close of $227.85 versus a narrative fair value of $253.12, the widely followed view sees Waste Management trading at a discount, with that gap explained by detailed assumptions on cash flows, growth and required return.

The company's strategic investments in sustainability, particularly in the areas of recycling and renewable energy, are showing strong, high-return growth, which could drive future revenue increases. The integration and optimization of WM Healthcare Solutions are on track to deliver significant synergies, anticipated to reach $250 million annually by 2027, positively impacting earnings.

Curious what kind of revenue mix, margin uplift and long term growth path need to line up to justify that fair value gap? The narrative leans on a specific blend of steady expansion, improving profitability and a premium future earnings multiple to anchor its $253.12 estimate.

Result: Fair Value of $253.12 (UNDERVALUED)

However, you also need to weigh up risks such as revenue volatility from exiting lower margin business and higher leverage after the Stericycle deal if integration disappoints.

Another View: Market Multiple Paints a Richer Picture

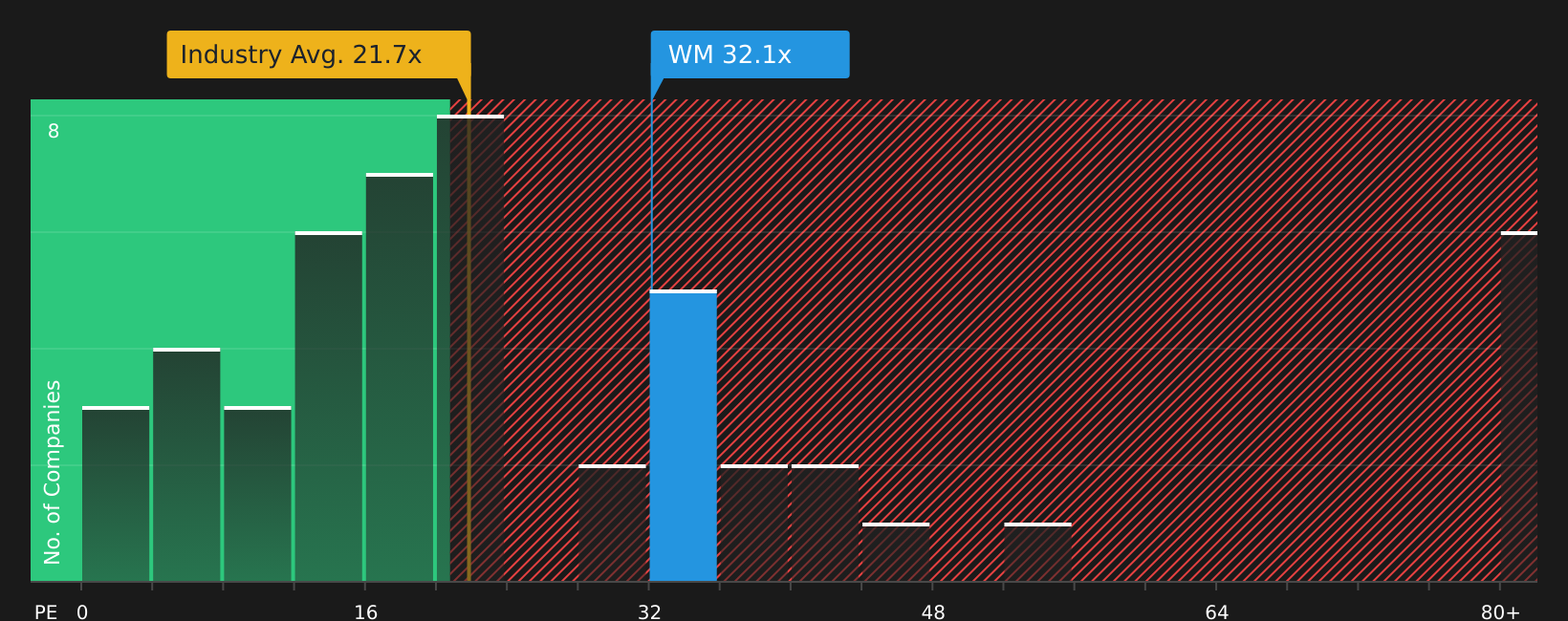

While the narrative fair value suggests Waste Management is around 10% undervalued, the current P/E of 32.7x tells a tighter story. It sits above the US Commercial Services industry at 21.5x and above the fair ratio of 30.1x, even though it is below the peer average of 35x.

That mix of a premium versus the industry, a smaller gap to peers, and a P/E above the fair ratio hints at less margin of safety and more sensitivity if expectations slip. The question is how comfortable you are with paying up for quality in this case.

Next Steps

Mixed signals so far, right? If you want to move quickly and build your own view from the ground up, start by weighing the 4 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that better fit your goals, risk comfort and income needs.

- Target stability and sleep easier at night by scanning 70 resilient stocks with low risk scores that have already cleared strict risk filters.

- Pursue value by checking 48 high quality undervalued stocks built around companies with solid fundamentals and prices that look appealing.

- Grow your income stream by reviewing 12 dividend fortresses that focus on higher yielding dividend payers with robust profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.