A Look At Waste Management (WM) Valuation As Earnings Approach After Prior Revenue And Income Miss

Waste Management, Inc. WM | 0.00 |

Upcoming earnings put Waste Management (WM) in focus

Waste Management (WM) is set to report earnings after the bell on Tuesday, following a quarter in which it slightly missed revenue and adjusted operating income estimates. The market now expects slower year on year revenue growth.

WM’s share price at US$226.20 has had a modest 3.57% year to date share price return. The 3 year total shareholder return of 42% and 5 year total shareholder return of 74.24% point to steadier long term compounding despite recent softness into earnings.

If upcoming results have you reassessing where growth could come from next, this is a good time to scan the market for other opportunities through a focused screener like 33 power grid technology and infrastructure stocks

With WM trading near US$226.20, showing an intrinsic discount of about 3% and a roughly 13% gap to the average analyst price target, you may want to consider whether there is still a buying opportunity here or whether potential future growth is already reflected in the price.

Most Popular Narrative: 10.6% Undervalued

Against WM’s last close at $226.20, the most followed narrative points to a fair value of $253.12, suggesting the current price sits below that estimate and is underpinned by detailed growth and margin assumptions.

The company's strategic investments in sustainability, particularly in the areas of recycling and renewable energy, are showing strong, high-return growth, which could drive future revenue increases. The adoption of automation and technology, such as automated recycling facilities, is leading to improved EBITDA margins, which might provide stronger future earnings.

Curious what sits behind that valuation gap? The narrative leans on a specific mix of revenue expansion, margin uplift and a premium earnings multiple that is usually reserved for faster growing names. The exact combination of growth rates, profitability targets and discount rate assumptions is what gets this fair value to $253.12.

Result: Fair Value of $253.12 (UNDERVALUED)

However, this narrative could be challenged if economic pressure on industrial customers or regulatory shifts in renewable energy and recycling squeeze margins more than expected.

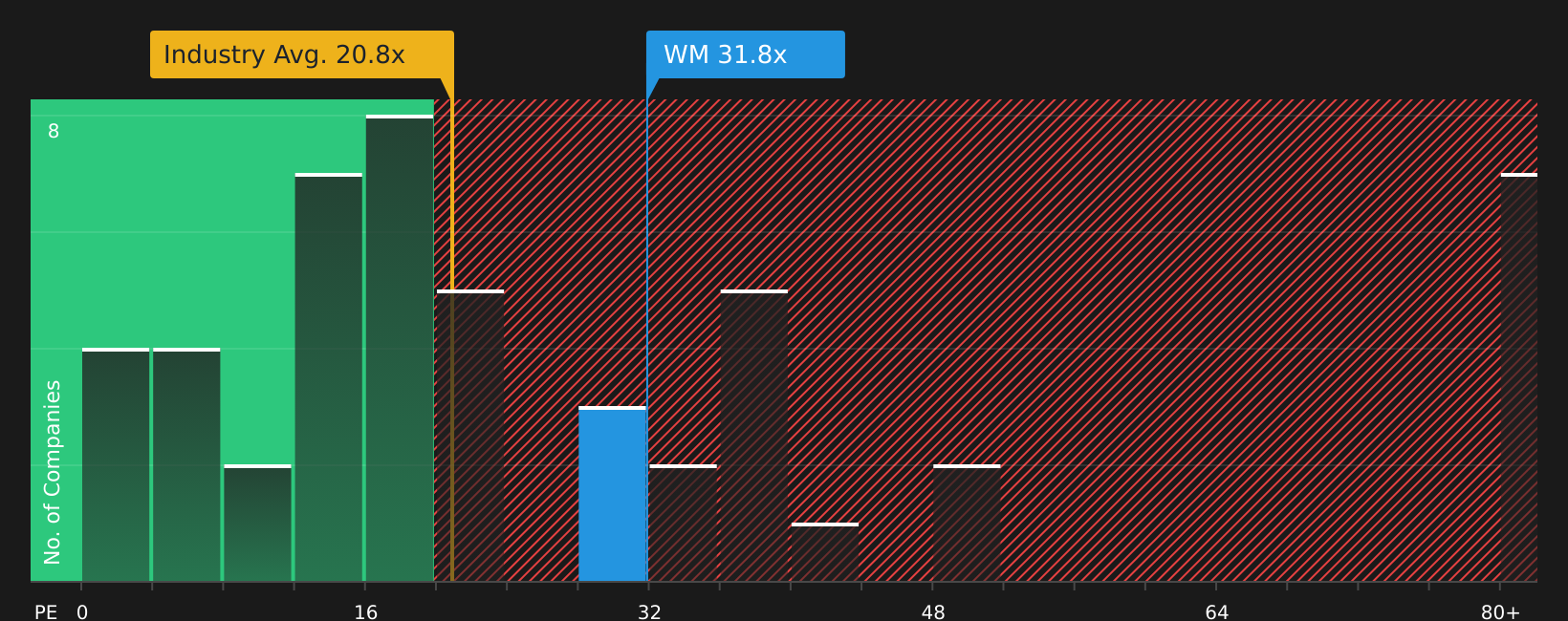

Another View: What Earnings Multiples Are Saying

The narrative-based fair value of $253.12 suggests WM is 10.6% undervalued, but the earnings multiple sends a more cautious signal. WM trades on a P/E of 33.7x, which is higher than the US Commercial Services industry at 22.8x and above its own fair ratio of 30.2x, pointing to valuation risk if expectations cool.

Put simply, the market is already paying more for each dollar of WM earnings than for the industry average, and even more than the ratio our fair ratio suggests the market could move toward. That tension between an undervalued DCF style estimate and a rich earnings multiple raises a practical question for you: which signal do you trust more at today’s price?

Next Steps

This mix of optimism and concern can feel conflicting, so move quickly, review the underlying data, and weigh the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If WM is already on your radar, broaden your watchlist now with a handful of focused ideas you can act on before the next wave of earnings hits.

- Target future income by scanning companies built around dependable payouts with the 13 dividend fortresses.

- Spot opportunities where quality and price still line up using the 53 high quality undervalued stocks.

- Prioritise resilience first by checking companies that score well on financial strength through the 73 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.