Adobe Is Priced for Too Much Bad News

Adobe Systems Incorporated ADBE | 0.00 |

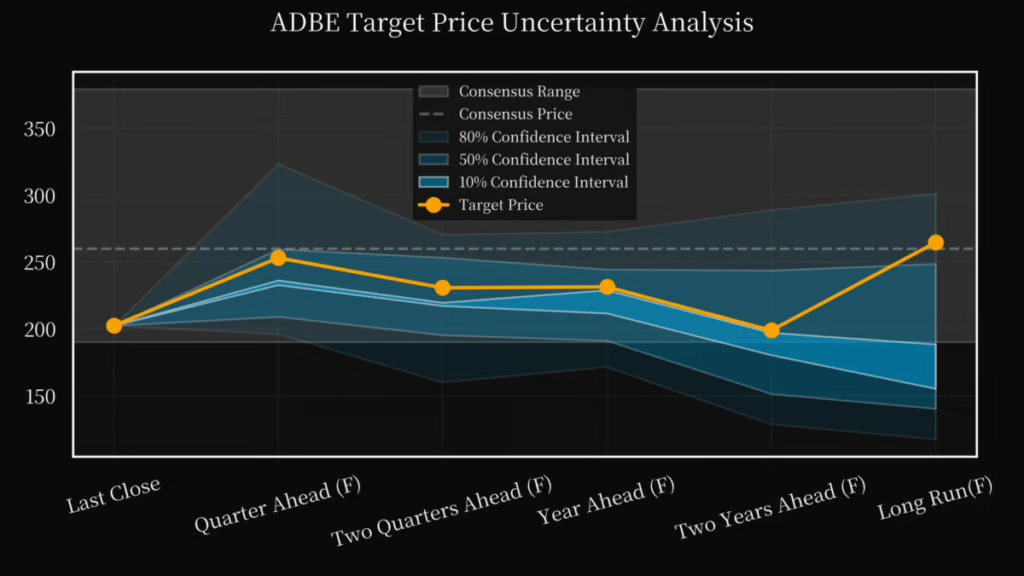

Adobe (NASDAQ:ADBE) has had a brutal year, and the ADBE stock forecast has rarely been more contested. Shares have fallen from above $400 in mid-2025 to around $202 today — a roughly 50% decline — driven by a CFO departure, investor skepticism about AI monetization timelines, and broad multiple compression across software. The Wall Street consensus has drifted to a lukewarm “Hold,” with an average street price target of approximately $282. But the operating data embedded in four consecutive quarters of SEC filings tells a more nuanced story.

ADBE Stock Price Targets: What the Model Shows

Valuation modeling using multi-scenario probability distributions across P/E, P/OCF, and DCF frameworks — calibrated against a Fed funds rate of 3.62%, stable GDP growth, and Adobe’s current financial profile — produces the following price targets:

| Horizon | Target Price | Implied Upside from $202.41 |

|---|---|---|

| One Quarter Ahead | $253.01 | +25% |

| Two Quarters Ahead | $230.68 | +14% |

Methodology Overview: The valuation framework combines traditional financial analysis with quantitative AI-driven forecasting. Large language models (LLMs), integrated with a financial knowledge graph, are used to analyze and project key valuation drivers including revenue growth, operating margins, interest rates, liquidity conditions, and broader macroeconomic indicators. These forecasts are calibrated against historical company and market data to estimate the relative impact of each factor on future valuation outcomes.

The model then performs Monte Carlo simulations across thousands of potential scenarios, generating a probability distribution of future valuations rather than a single deterministic estimate. The published target prices represent the central tendency of these simulated outcomes, while the valuation ranges reflect the uncertainty embedded in different operating and market environments.

For Adobe, the primary valuation drivers include revenue growth expectations, AI monetization assumptions, free cash flow generation, operating margin stability, and software-sector valuation multiples. The one-quarter target reflects a rebound driven by potential positive earnings revisions and stabilizing investor sentiment. The moderation at two quarters is deliberate — it anticipates a deceleration phase as the market reassesses EBITDA multiples and waits for evidence of freemium-to-paid conversion in Adobe’s AI products.

These are probability-weighted estimates across multiple scenarios, not single-point analyst price targets. The 80% confidence interval for the one-quarter horizon spans roughly $175 to $300. Position sizing should reflect that range, not just the midpoint. The framework also incorporates time-series decomposition and residual-error adjustments to reduce seasonal distortions across valuation horizons.

ADBE stock forecast. Source: Ian Financial Vision, ianfv.com

Why ADBE Stock Is Down 50%: Three Real Headwinds

Adobe’s Q2 2026 results beat revenue consensus — $6.62 billion, up 12.7% year over year — and management raised full-year guidance. So why did the stock keep falling? Three reasons:

1. The AI monetization pivot creates near-term ARR ambiguity. Management has explicitly shifted priority away from maximizing Annualized Recurring Revenue in the short term toward user acquisition and AI integration — expanding its freemium base through tools like Adobe Firefly and Adobe Express. This is a rational long-term move. It is also a clean opening for bears, who can argue that any ARR slowdown is structural. The market is discounting the lag between user acquisition and monetization, and that discount may persist for one or two more quarters.

2. The Semrush acquisition clouds organic growth. Adobe’s $1.9 billion acquisition of Semrush Holdings boosted headline ARR, but investors are actively trying to strip out the inorganic contribution to assess underlying growth velocity. Until Adobe provides cleaner organic ARR disclosure, the market will apply a skepticism discount to reported figures.

3. CFO departure adds execution uncertainty. Adobe’s CFO exit introduces leadership risk during a period when financial communication matters most. Multiple compression at the CFO-transition stage is a well-documented pattern in software stocks — regardless of underlying operational health.

What the Bears Are Getting Wrong About Adobe

Beneath the narrative noise, Adobe’s core operating profile remains structurally strong.

Revenue trajectory is intact. Adobe has compounded revenue at roughly 11.2% CAGR over five years, with sequential quarterly growth of 3–4% showing no signs of deterioration. Q4 seasonality driven by enterprise year-end spending remains reliable.

Gross margins are holding near 88–89%. The slight erosion observed in 2026Q2 warrants monitoring but is not yet a trend. More importantly, cash flow quality — operating cash flow relative to net profit — has consistently exceeded 1.2x across all measured quarters. The earnings are not optical. The cash is real.

ROIC has been above 9% since early 2025. The divergence between ROI (volatile, reflecting strategic investment cycles) and ROIC (steadily rising) is the key signal here. A rising ROIC trend in a software business is a durable indicator of pricing power and capital efficiency — not something that reverses quickly.

Revenue per employee is widening versus the sector. Adobe’s per-employee revenue CAGR exceeds 10% in recent periods while the industry average remains flat and volatile. This gap has widened materially since 2023, suggesting genuine operational leverage rather than cost-cutting optics.

The Legitimate Bear Case

No ADBE stock forecast is complete without engaging the downside honestly. ROE remains below the industry average. Adobe’s return on equity troughed at 4.01 in 2024Q1, against a sector average of 12.52 at the time. It has recovered since but has not yet reached peer parity. The aggressive share repurchase program ($8.8 billion spent against a $25 billion authorization) will mechanically lift ROE by compressing the equity base — but only if earnings grow proportionally.

SG&A costs are structurally elevated. Adobe’s SG&A expense ratio has run 2.5–3.5 percentage points above the industry baseline throughout the observed period. The 2024Q4 spike to 35.53 — versus the sector peak of 32.96 — is a flag. Adobe is spending aggressively on customer acquisition, which is coherent strategy for building a freemium-to-paid funnel. The question is payoff timeline.

Asset-light efficiency is deteriorating relative to peers. This is the most underappreciated risk in Adobe’s operating data. While Adobe’s Asset-Light Ratio has held in the 7–8 range, the industry average has climbed from roughly 11 to 16 over the same period. Adobe is getting less scalable relative to software peers, not more — a meaningful concern as AI infrastructure costs grow.

Two Metrics That Will Move the Stock

Two data points will determine whether the one-quarter target of $253 materializes:

Organic ARR disclosure. If Adobe begins separating Semrush-attributed ARR from organic ARR growth in its Q3 2026 reporting, the market will have cleaner data to work with. Clarity alone could be a re-rating catalyst.

Freemium conversion rate. The shift from ARR maximization to user acquisition only creates value if free users eventually convert to paid subscribers. Any management commentary in the next earnings call quantifying conversion velocity — even directionally — will move the stock.

The two-quarter target of $230.68 implies a deceleration after an initial rebound. That plateau is not a bearish call; it reflects the likely reality that full re-rating requires one to two quarters of evidence, not just rhetoric.

Bottom Line: A 50% Decline May Be More Than Enough

ADBE at $202 is a stock, where near-term narrative is doing most of the talking. The AI pivot, CFO transition, and Semrush noise are real concerns — but they are already reflected in a price that represents a 50% haircut from 2025 highs and sits at multi-year support levels.

The medium-term operating story — robust free cash generation, stable gross margins, compounding ROIC, and an 11%+ revenue CAGR that has not broken — is being systematically discounted. The one-quarter price target of $253 represents the scenario where that discount begins to close. The two-quarter target of $231 reflects a more measured re-rating as investors wait for execution proof.

That is the crux of any near-term ADBE stock forecast: not whether Adobe’s moat is intact — it is — but whether management can communicate the transition clearly enough to rebuild investor confidence. Watch organic ARR and freemium conversion. Everything else is noise.

Valuation analysis sourced from Ian Financial Vision (ianfv.com), an AI-native financial research platform providing institutional-grade valuation models for individual investors. Price path estimates represent probability-weighted scenario distributions across multiple valuation frameworks, not single-point forecasts. This article is for informational and educational purposes only and does not constitute investment advice. Readers should conduct their own due diligence and consider consulting a financial advisor before making investment decisions.

Disclosure: The author is affiliated with Ian Financial Vision, which produced the underlying valuation analysis referenced in this article. No positions in ADBE are held by the author at the time of publication.

image credit: Author

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.