AES (AES) Stock Still Looks Cheap On Fair Value Despite A 43% Gain

AES Corporation AES | 0.00 |

AES stock has delivered a 43.1% return over the past year, yet valuation checks and an intrinsic value estimate based on a Discounted Cash Flow (DCF) model both suggest the shares still trade at a discount to what the underlying cash flows may support. With a recent last close of US$14.66 and a history that includes weaker multi year returns, the tension for investors is whether today's price properly reflects the company’s changing outlook and capital needs.

- AES is up 43.1% over the past year, which puts recent gains in focus after a weaker three and five year share price record.

- The approved acquisition by a Global Infrastructure Partners and EQT led consortium and ongoing rate decisions for AES Indiana can support expectations around future cash flows, while fresh debt issuance and regulatory scrutiny over electricity prices may weigh on how much investors are willing to pay for those cash flows.

- AES screens as undervalued across most of Simply Wall St’s checks, with the broader valuation work suggesting the stock looks cheap on 5 of 6 metrics compared with its fundamentals.

The issue now is whether AES’s current share price offers enough margin against the intrinsic value suggested by the Discounted Cash Flow (DCF) and the broader valuation checks.

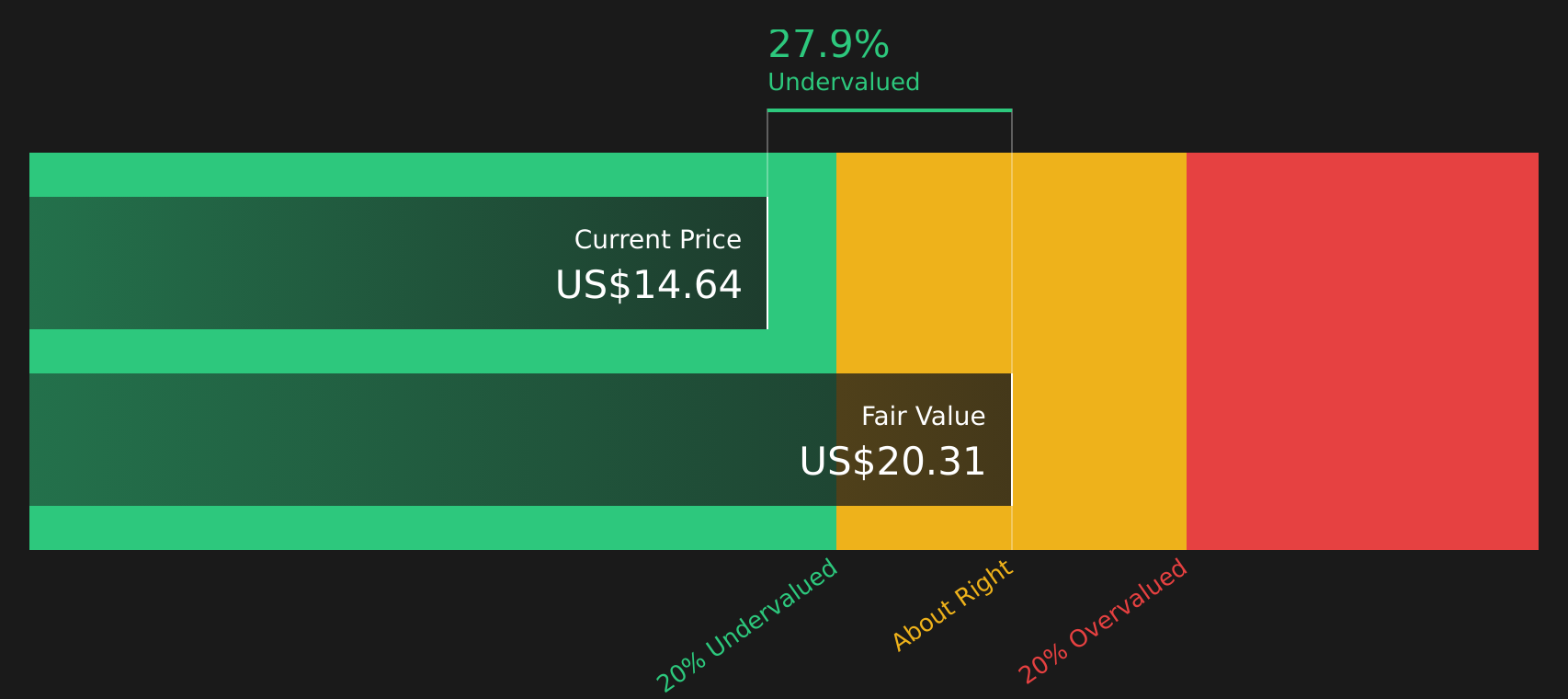

Is AES a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) model values AES by projecting future free cash flows and discounting them back to today. For AES, the latest twelve month free cash flow is a loss of $2.19b, yet the model assumes cash flows recover to positive territory over the coming years, consistent with the 2 Stage Free Cash Flow to Equity approach used.

Based on those assumptions, the DCF points to an estimated intrinsic value of about $19.65 per share, compared with the recent price of $14.66, implying the stock appears roughly 25.4% undervalued according to this model. The approved acquisition by the Global Infrastructure Partners and EQT led consortium helps explain why the market is assigning value to future cash flows even while recent free cash flow is weak.

Overall, the DCF output indicates that AES may be undervalued relative to the cash flows implied by this analysis.

Our Discounted Cash Flow (DCF) analysis suggests AES is undervalued by 25.4%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Is AES a Bargain on Earnings?

P/E is a useful measure for AES because earnings are a key focus for regulated and contracted utilities. On this measure, AES trades on a P/E of about 7.6x, which is less than half the Renewable Energy industry average of 15.6x and far below the peer group average of 34.2x. That comparison suggests the market is assigning a much lower earnings multiple to AES stock than to many sector peers.

The fair P/E ratio implied by Simply Wall St’s model is about 21.5x. This reflects what investors might typically pay given AES’s industry, risk profile and fundamentals. Set against the current 7.6x, that is a wide gap and indicates the shares change hands at a sizeable discount to this tailored benchmark. For readers weighing the recent acquisition approval and regulatory decisions, this earnings multiple suggests the market is cautious, but possibly more cautious than the fundamentals imply.

On the P/E multiple, AES stock appears undervalued compared with both its industry and the model’s fair ratio.

The AES Narrative: What Would Justify Today's Price?

To help make sense of AES' valuation puzzle, Simply Wall St Narratives set out the specific paths for growth, margins and earnings that would need to hold for the stock to be worth meaningfully more or less than today’s price, and they sit on the company’s Community page. Each narrative links its number to a clear view on how AES' opportunities, profitability and risks might evolve, giving you a reference point to revisit as fresh information comes through.

One of the top community narratives on AES: roughly fairly valued

"AES's leading, long-term pipeline of renewables and energy storage projects, backed by robust, multi-year Power Purchase Agreements (PPAs) with data center and corporate customers, positions the company to capitalize on rapidly rising electricity demand from AI/data centers…"

Do you think there's more to the story for AES? Head over to our Community to see what others are saying!

The Bottom Line

For AES, both the Discounted Cash Flow (DCF) estimate and the earnings multiple view point in the same direction, suggesting the stock screens as undervalued on current assumptions. The key question is whether the cash flows that underpin that intrinsic value, and the earnings that support a higher P/E, materialise in a way that justifies closing the gap. From here, what matters most is whether AES can turn its project pipeline and regulatory outcomes into stable, visible cash generation that convinces the market the discount is too wide rather than a reflection of ongoing risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.