Amazon (AMZN) Stock Could Be A Bargain Despite A 91% Run

Amazon.com, Inc. AMZN | 0.00 |

Amazon.com stock has returned 91.0% over the past three years, yet current valuation checks and intrinsic value estimates still suggest the shares are trading at a discount to what the underlying cash flows imply.

- A 91.0% gain over three years highlights how much investors have already repriced Amazon.com. This raises the bar for any further upside to be supported by fundamentals.

- Heavy spending on AI infrastructure and the large, volatile stake in Anthropic can support long term cash flow potential, but they also add capital intensity and execution risk that could affect how quickly that value is realized.

- Amazon.com screens as undervalued on both a Discounted Cash Flow (DCF) intrinsic value estimate and earnings multiples, yet earns a mixed score of 4 out of 6 on the broader checks. According to these valuation tests, the overall picture appears balanced rather than an obvious bargain.

The issue now is whether Amazon.com's current share price around US$245.98 already reflects a fair share of its AI and cloud ambitions, or if the combined signals still leave meaningful room relative to intrinsic value.

Is Amazon.com Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model here projects what Amazon.com’s future free cash flows could be worth in today’s dollars. On the latest twelve month numbers, Amazon.com generated about $37.1b of free cash flow, and the model assumes these cash flows keep growing rather than staying flat or shrinking.

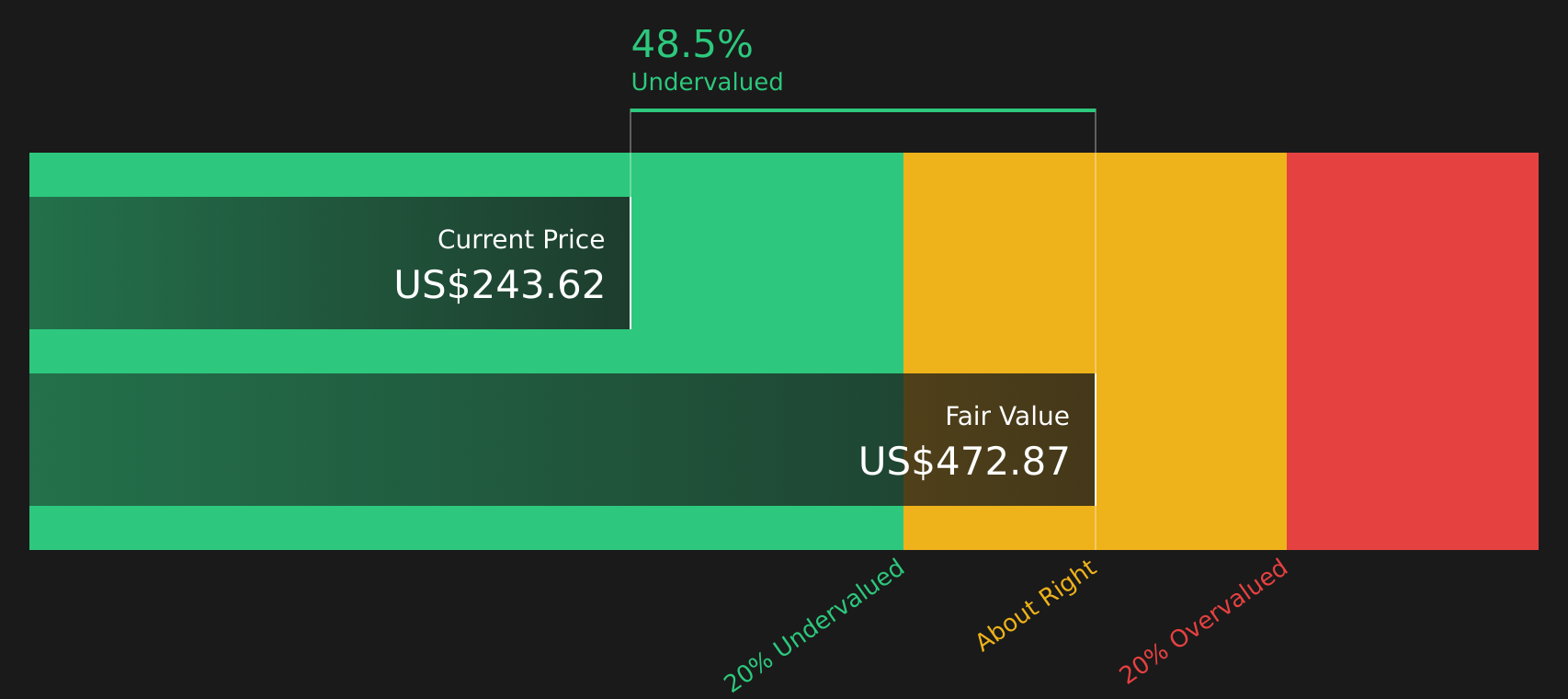

On that basis, the 2 Stage Free Cash Flow to Equity model points to an estimated intrinsic value of about $473 per share, compared with the current share price around $245.98. This implies the stock screens as roughly 48.0% undervalued. The recent $25b bond sale to fund AI infrastructure helps explain why the market is focusing on capital intensity even though the DCF places a higher value on those future cash flows.

Taken together, the discounted cash flow work suggests Amazon.com stock currently looks undervalued relative to the cash flows implied in this model.

Our Discounted Cash Flow (DCF) analysis suggests Amazon.com is undervalued by 48.0%. Track this in your watchlist or portfolio, or discover 45 more high quality undervalued stocks.

Is Amazon.com Still Cheap on Earnings?

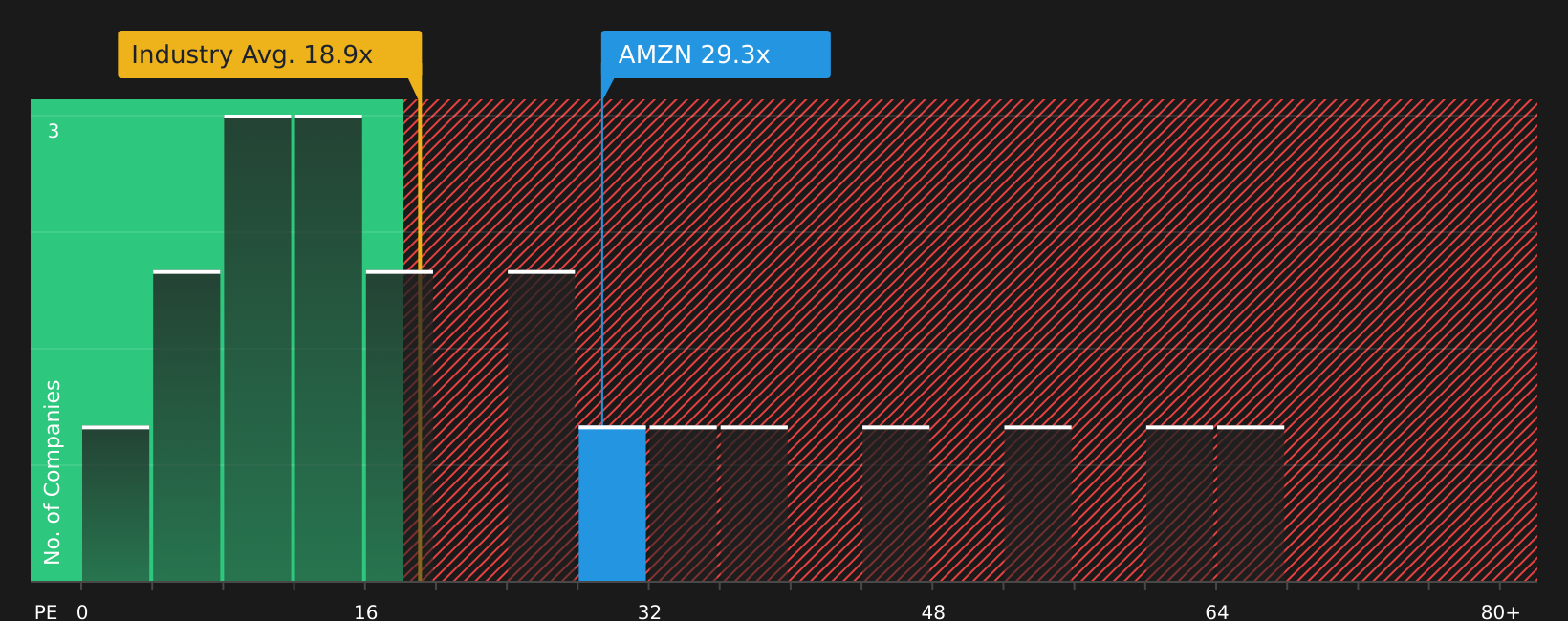

P/E tends to be a useful yardstick for Amazon.com because earnings have become a clearer driver of how the stock is priced. Right now, Amazon.com trades on a P/E of about 29.1x, slightly above the peer average of 27.6x and well above the broader Multiline Retail industry average of 18.9x. This reflects how differently the market views its mix of e-commerce, cloud and AI exposure versus traditional retailers.

However, the Fair P/E Ratio implied by the checks is about 44.3x, which is materially higher than where Amazon.com trades today. That gap suggests the current 29.1x multiple is below what would typically be expected once you factor in the company’s scale, profitability profile and risk mix. On this framework the stock screens on the inexpensive side rather than priced for perfection.

On the P/E multiple alone, Amazon.com stock appears undervalued relative to the earnings-based fair ratio implied by these checks.

The Amazon.com Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Amazon.com sit on the Community page and act as the link between the mixed valuation signals above and the specific futures that could make the stock worth materially more or less than today’s price. Each narrative ties its number to a clear view on how Amazon.com's growth, margins and risk profile might evolve, giving you a structured reference point to revisit as new information comes through.

The community is split on Amazon.com, with one camp arguing the market is underestimating the AI buildout while another sees the stock roughly in line with its fundamentals.

Bull case: 45% undervalued

"Amazon is sacrificing short-term margins to secure long-duration dominance in AI infrastructure, advertising, and automated commerce..."

Bear case: roughly fairly valued

"The only two negatives I took from it was AWS not growing to revenue expectations and then also during the Q and A they were asked about AI innovation and so on, and they never really never answered the questions and were just very vague..."

Do you think there's more to the story for Amazon.com? Head over to our Community to see what others are saying!

The Bottom Line

For Amazon.com, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple checks point to the stock looking undervalued rather than stretched. The broader set of valuation checks is mixed, which suggests the apparent discount comes with real questions about capital intensity, AI spending and execution. From here, the crux is whether Amazon.com converts its heavy AI and cloud investment into sustained, high quality cash flows without eroding returns, or whether that required spend is exactly what the current price is already accounting for.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.