Amazon (AMZN) Stock Valuation After Recent Pullback And Long Term Returns

Amazon.com, Inc. AMZN | 0.00 |

Amazon.com stock in focus

Amazon.com (AMZN) is back on investors’ radar after recent share price moves, with the stock down 10% over the past month but showing a gain over the past three months.

That recent pullback sits against a mixed backdrop, with the 30 day share price return down 9.69%, the 90 day share price return up 12.66%, and the 3 year total shareholder return at 90.09%. This suggests that momentum has cooled in the short term but remains stronger over a longer period.

If Amazon.com’s recent moves have you thinking about where the next big themes could come from, this is a good time to scan 48 AI infrastructure stocks

With Amazon.com shares pulling back recently yet still showing stronger multi year returns, the key question is whether current valuations reflect its retail, cloud and advertising mix or whether markets are already pricing in future growth.

Most Popular Narrative: 47% Undervalued

Compared with the last close at $238.55, the most followed narrative suggests a fair value of $450 per share, implying a large valuation gap based on long term assumptions.

Amazon is sacrificing short-term margins to secure long-duration dominance in AI infrastructure, advertising, and automated commerce. These investments are already working, and margins are positioned to inflect upward by the end of 2026.

Curious how a retail, cloud, and advertising mix supports that higher price tag? The narrative leans heavily on compounding earnings power, richer margins, and patience from investors.

Result: Fair Value of $450 (UNDERVALUED)

However, this bullish setup can unravel if heavy AI and infrastructure spending weighs on profits for longer than expected, or if AWS growth slows relative to investor hopes.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

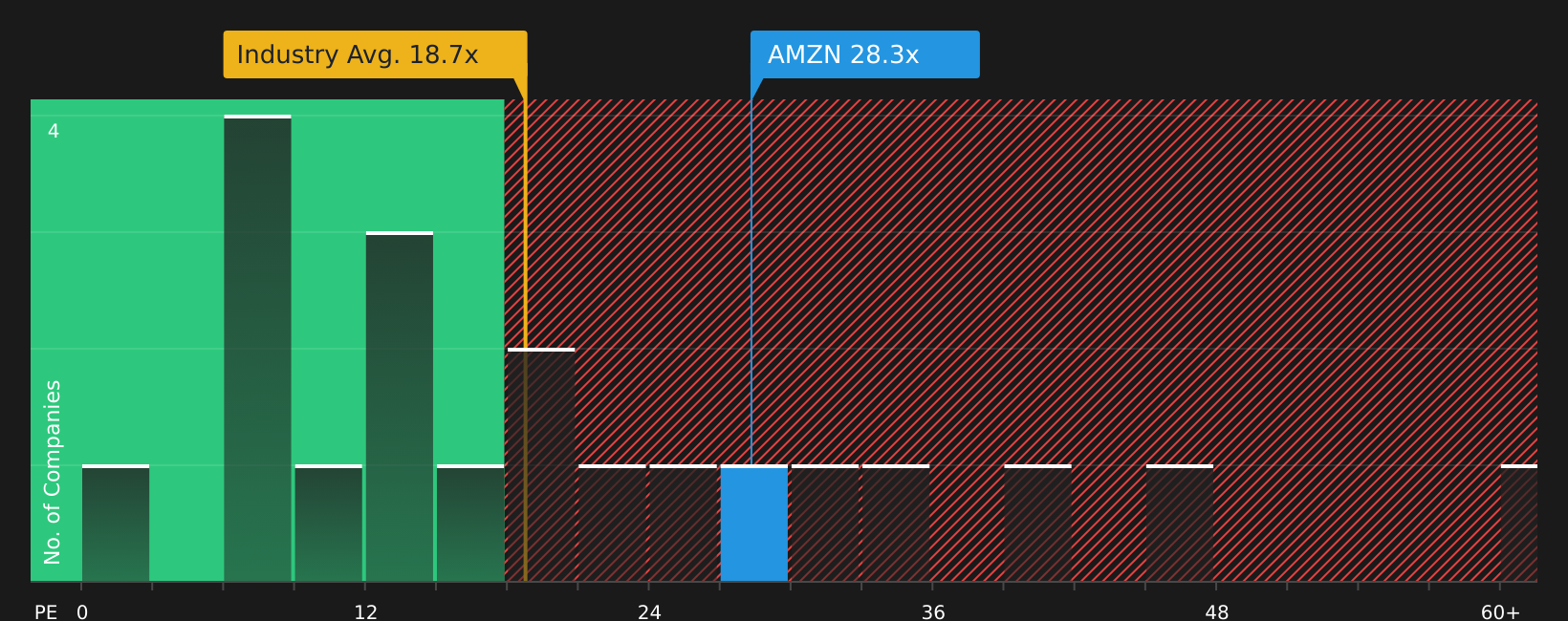

Another View: What P/E Says About Amazon.com

While the narrative points to a fair value of $450, the current P/E of 28.3x sits above both the peer average of 22.7x and the Global Multiline Retail average of 18.7x, yet below an estimated fair ratio of 44.9x. This leaves you weighing valuation risk against possible upside.

To see how that gap could close, and what the numbers imply for future valuation shifts, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this combination of optimism and caution leaves you undecided, quickly move from reading to reviewing the data yourself with our breakdown of 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with just one stock, you could miss opportunities that fit your goals better, so put a few minutes into scanning wider with focused screeners.

- Spot potential bargains early by reviewing companies filtered through the screener containing 20 high quality undiscovered gems.

- Prioritise resilience by checking companies highlighted in the 71 resilient stocks with low risk scores.

- Target dependable cash generators by scanning the 8 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.