American Airlines Group (AAL) Could Be 16% Above Fair Value After Index Changes

American Airlines Group Inc. AAL | 0.00 |

Index changes put American Airlines Group in focus for investors

American Airlines Group (AAL) was recently removed from several Russell value benchmarks, a technical shift that can alter how index funds and quantitative strategies treat the stock in portfolios.

These index removals do not directly affect American Airlines Group operations, but they can influence trading flows as passive funds adjust holdings, potentially changing liquidity patterns and ownership mix around the stock.

Set against this index reshuffle, American Airlines Group’s share price has been strong, with a 30 day share price return of 23.43%, a 90 day share price return of 62.35% and a 1 year total shareholder return of 56.86%. However, longer term total shareholder returns over three and five years have been broadly flat to negative, suggesting recent momentum has picked up after a weaker stretch.

If you are looking beyond airlines and want to see what else is moving, this is a good time to widen your search through the 20 top founder-led companies

With American Airlines Group now outside key value indices but showing recent share price strength, the real question is whether the current valuation still offers upside or whether the market is already pricing in future growth.

Most Popular Narrative: 16% Overvalued

American Airlines Group last closed at $18.07, above the most widely followed fair value estimate of $15.61, which frames how some analysts view the recent share price strength.

The analysts have a consensus price target of $15.61 for American Airlines Group based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $24.0, and the most bearish reporting a price target of just $10.0.

There is one core story running through this valuation, a mix of stronger earnings power, modest revenue expansion, and a future earnings multiple that needs those assumptions to hold. Curious which specific profit and cash flow paths sit underneath that fair value line, and how sensitive the outcome is to even small changes in those inputs.

Result: Fair Value of $15.61 (OVERVALUED)

However, this hinges on American Airlines Group managing higher labor costs and a sizable debt load. Any stumble here could quickly challenge the current bullish narrative.

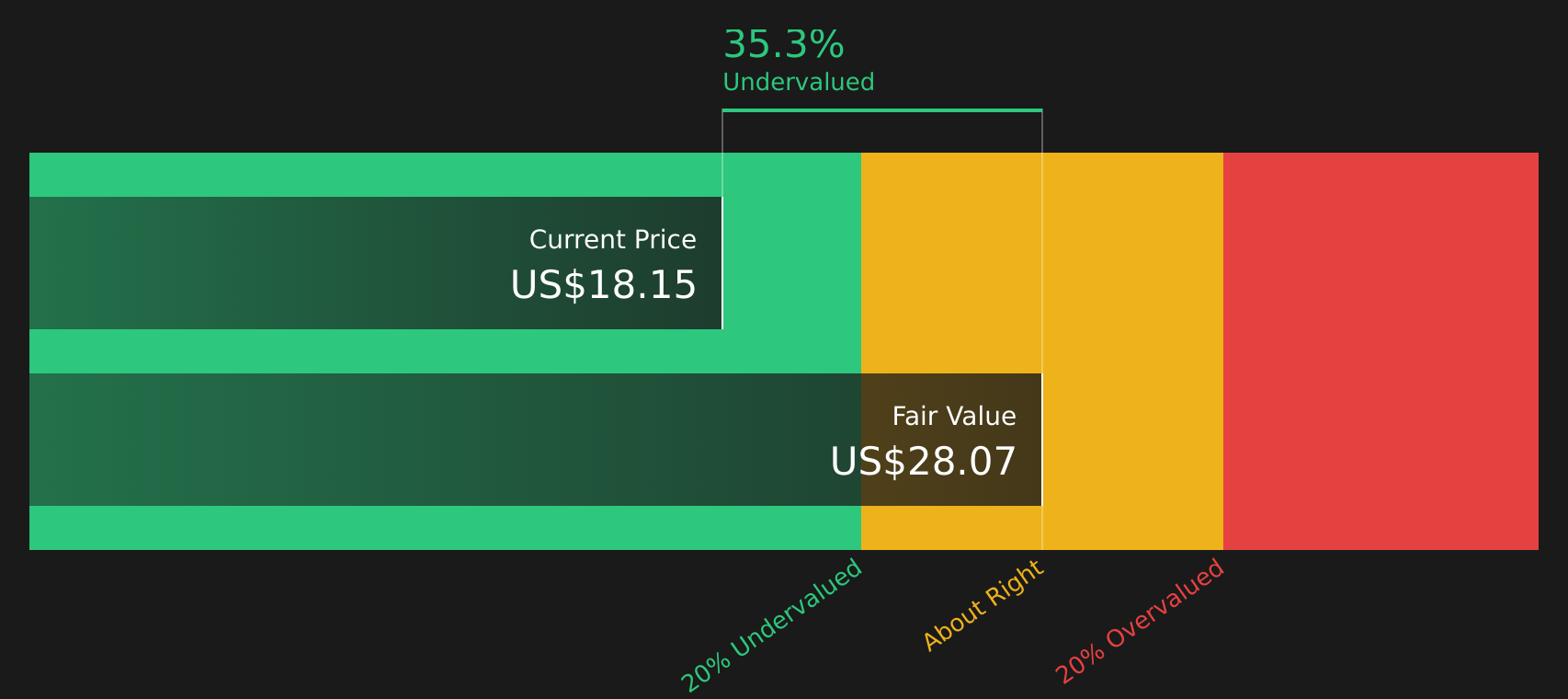

Another View: SWS DCF model points to slight undervaluation

While analyst targets suggest American Airlines Group is about 16% overvalued at $18.07 versus a $15.61 fair value, the SWS DCF model points the other way, with a fair value of $18.56, implying the stock trades roughly 2.6% below that estimate. Which lens do you trust more for the long haul?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out American Airlines Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across valuation models and sentiment around American Airlines Group, this is a moment to act quickly and review the underlying data for yourself, including the 2 key rewards and 4 important warning signs

Looking for more investment ideas beyond American Airlines Group?

Do not stop with American Airlines Group. Broaden your watchlist with fresh ideas so you are not relying on a single story to drive your portfolio.

Use the Simply Wall Street Screener to quickly scan for stocks that fit what you care about most, whether that is quality, value, income, or resilience.

- Target potential mispriced opportunities before the crowd by checking out screener containing 19 high quality undiscovered gems

- Strengthen your portfolio’s foundation with companies that prioritize financial resilience using the solid balance sheet and fundamentals stocks screener (48 results)

- Explore income focused ideas that pay you while you hold by filtering through the 10 dividend fortresses

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.