Amgen (AMGN) Could Be 45% Below Fair Value As Court Blocks Enbrel Price Cap

Amgen Inc. AMGN | 0.00 |

Amgen (AMGN) is back in focus after a federal judge blocked Colorado’s proposed 70% price cap on Enbrel, which removed an immediate regulatory threat to one of the company’s key revenue drivers.

The court decision has come on top of an already strong run in Amgen’s stock, with a 1-day share price return of 3.55% and a year to date share price return of 14.20%, while total shareholder return sits at 29.22% over one year and 87.63% over three years. This suggests momentum has been building despite recent regulatory noise around products like Tavneos and Corlanor.

If this regulatory win has you rethinking healthcare exposure, it may be worth widening your search to other drug developers and tools providers supported by AI by checking out 40 healthcare AI stocks

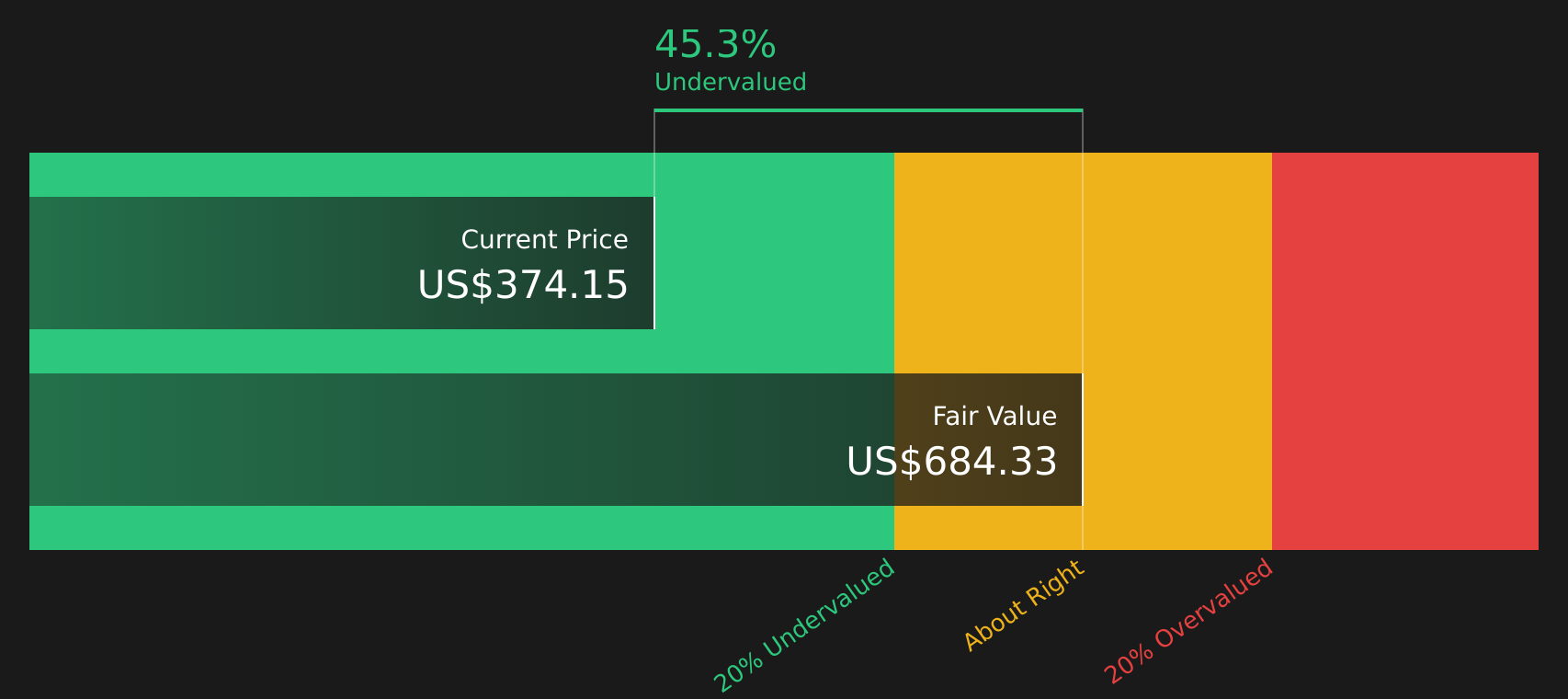

With Amgen now trading at $374.15, above one fair value estimate of $353.58 yet showing a 45.33% intrinsic discount on another model, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 6.2% Overvalued

With Amgen at $374.15 against a widely followed fair value estimate of about $352, the current price sits modestly above that narrative benchmark while still reflecting a business with meaningful earnings and revenue.

Advancements in personalized and targeted therapies, reflected in the robust late-stage pipeline (e.g., MariTide for obesity/type 2 diabetes, Repatha and olpasiran for cardiovascular, multiple bispecific T-cell engagers for oncology), position Amgen to launch high-margin, first-in-class products that drive both top-line growth and margin expansion in the coming years.

Read the complete narrative. Read the complete narrative.

The fair value hinges on measured revenue growth, higher profit margins, and a richer future earnings multiple. Want to see how those three ingredients come together and which assumptions really move the dial on Amgen's valuation story?

Result: Fair Value of $352.23 (OVERVALUED)

However, Amgen’s story can still be challenged if drug pricing pressures intensify or if biosimilar competition on key products eats into revenue and margins.

Another View: Amgen Through the DCF Lens

The earlier fair value of about $352 per share paints Amgen as modestly overvalued, but the SWS DCF model points in a different direction. On that measure, Amgen at $374.15 is trading below an estimated future cash flow value of $684.33, suggesting the cash flow story is far more generous than the price tag implies. Which version of fair value do you think better reflects the risks and rewards in front of you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Amgen for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Amgen split between opportunity and caution, now is a good time to review the numbers, stress test the assumptions, and decide where you stand using the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Amgen?

If the Amgen story has sharpened your focus, do not stop here. Use the Simply Wall St Screener to uncover other stocks that fit your approach.

- Target potential value opportunities by checking companies that currently look mispriced using the 44 high quality undervalued stocks.

- Strengthen your income approach by reviewing stocks that feature higher yields and consistent payments through the 7 dividend fortresses.

- Prioritize resilience by focusing on companies with robust finances and sensible fundamentals via the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.