ASML (NasdaqGS:ASML) Stock May Look Fully Valued After South Korea Chip Investment

ASML Holding NV ADR ASML | 0.00 |

ASML Holding stock has delivered a very strong 166.1% return over the past five years, yet the valuation checks now lean toward the shares looking expensive rather than like an obvious bargain.

- Over five years, ASML Holding has returned 166.1%, which places more pressure on today’s share price to be supported by future cash flow and earnings growth.

- South Korea’s planned multi hundred billion dollar semiconductor investment can support demand expectations for ASML’s lithography equipment. However, any slowdown or delay in capital spending by major chipmakers remains a key risk for how much of that demand ultimately translates into orders.

- On Simply Wall St’s broader valuation checks, ASML Holding scores 2 out of 6, which suggests the stock currently leans expensive rather than offering clear value.

The issue now is whether ASML Holding’s current price still leaves enough valuation support after such a strong multi year run.

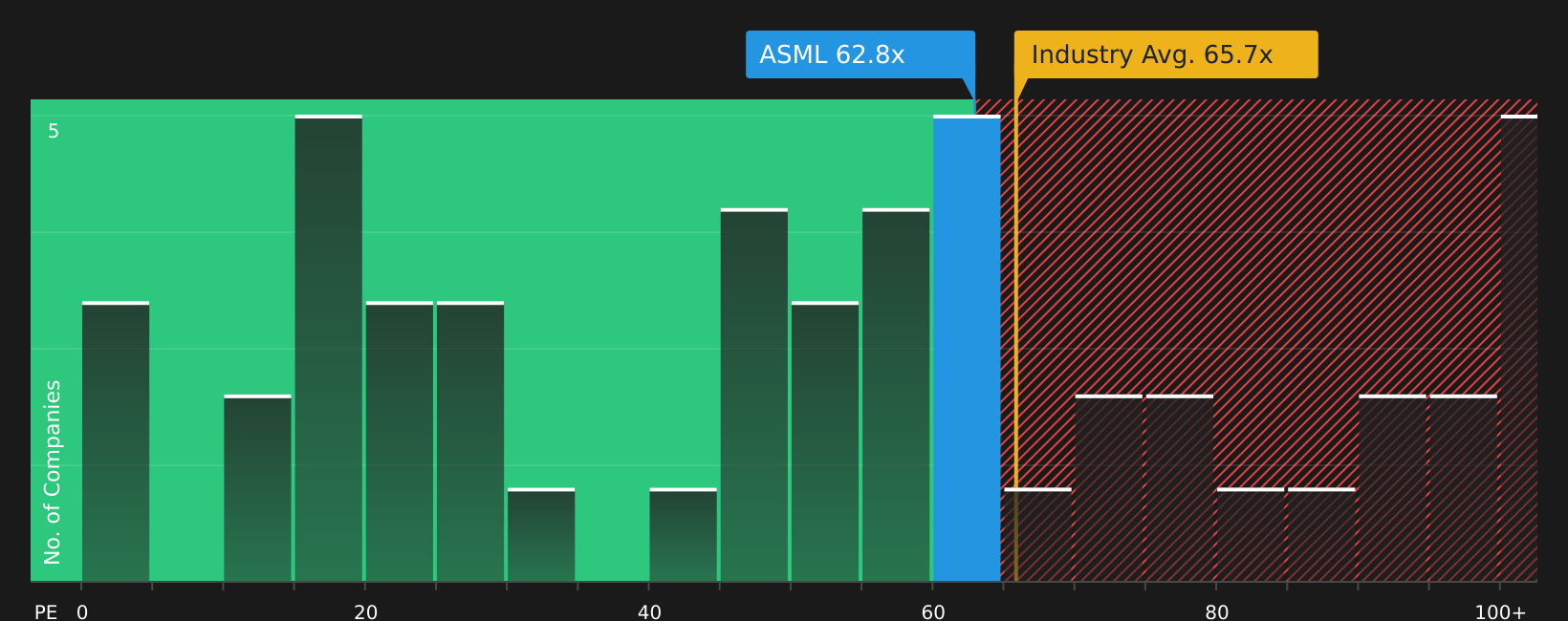

Does ASML Holding Look Pricey on Earnings?

The P/E ratio is a useful way to think about ASML Holding because earnings remain a core driver of how investors are valuing the business today. ASML Holding currently trades at about 62.8x earnings, which sits slightly below the semiconductor industry average of around 65.7x and just under the broader peer group at roughly 63.8x.

However, Simply Wall St’s model suggests a fair P/E closer to 52.9x, which is meaningfully lower than the current level. That gap implies investors are paying a premium to what the model indicates would be reasonable given ASML Holding’s earnings profile and risk factors, even after the strong sentiment around large semiconductor investment plans. On this P/E yardstick, ASML Holding appears expensive relative to the earnings that analysts currently expect it to generate.

The ASML Holding Narrative: What Would Justify Today's Price?

Simply Wall St’s Narratives for ASML Holding pick up where the valuation puzzle leaves off by spelling out which combinations of future growth, margins and earnings would need to play out for ASML Holding’s stock to be worth meaningfully more or less than it is today. Each scenario links its numbers to a specific view on how the company’s growth, profitability and risks could evolve, giving you something concrete to revisit as fresh information comes through.

Share a Narrative on ASML Holding to put numbers around your view on whether South Korea’s planned semiconductor build out ultimately delivers for the company, and track how that thesis holds up as new data comes through. Add your voice to the Simply Wall St community and set out the growth, margin and risk trade offs you think really matter from here.

Do you think there's more to the story for ASML Holding? Head over to our Community to see what others are saying!

The Bottom Line

ASML Holding now screens as overvalued on the main market multiple checks, with the P/E sitting above what Simply Wall St’s framework points to as a more grounded level. That does not rule out further upside, but it does mean today’s price already bakes in confident expectations on future earnings and industry demand. From here, the key question is whether ASML Holding can deliver the growth and resilience implied by that premium, especially if large chipmakers adjust or slow their capital spending plans.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.