Assessing Amazon.com (AMZN) Valuation As AI And Cloud Partnerships Draw Fresh Investor Focus

Amazon.com, Inc. AMZN | 0.00 |

Amazon.com (AMZN) is back in focus after a fresh wave of AI and cloud related news, including deeper ties with Anthropic and Snowflake and heavy capital spending on data center infrastructure.

The recent AI and cloud headlines sit on top of strong market interest, with a 30.5% 90 day share price return and a 33.2% 1 year total shareholder return, suggesting momentum has been building rather than fading.

If you are curious what other AI focused companies are attracting attention right now, it could be a good moment to scan the market using our screener of 47 AI infrastructure stocks

With Amazon trading at $274.00 and sitting about 14.1% below the average analyst price target and roughly 31% below one intrinsic value estimate, the key question is simple: is this genuine mispricing, or is the market already baking in years of AI driven growth?

Most Popular Narrative: 39.1% Undervalued

Against a last close of $274.00, the most followed narrative sets fair value at $450.00 per share, framing Amazon as materially mispriced rather than fairly valued.

Amazon is sacrificing short-term margins to secure long-duration dominance in AI infrastructure, advertising, and automated commerce. These investments are already working, and margins are positioned to inflect upward by the end of 2026.

This raises the question of what kind of growth and margin profile could justify a move from $274 to $450 per share. The narrative emphasizes AI-led cloud services, higher margin advertising, and a more profitable retail engine. The full story links those elements into a single valuation roadmap.

Result: Fair Value of $450.00 (UNDERVALUED)

However, this upbeat view can be tested if AI and cloud spending fail to translate into stronger profitability, or if heavy capital investment keeps margins under pressure for longer than expected.

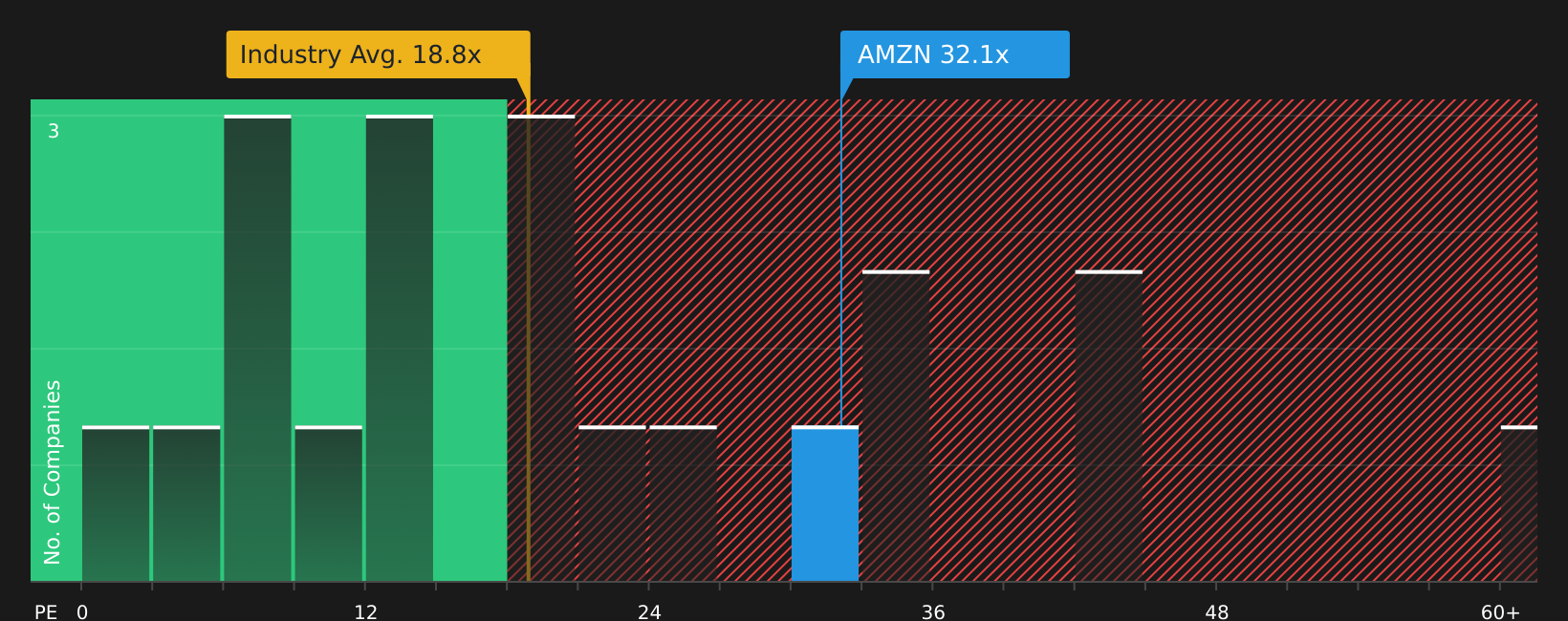

Another View: What The P/E Ratio Is Saying

While the user narrative leans on a $450 fair value, the current P/E of 32.5x tells a different story. It sits well above the global Multiline Retail industry at 18.9x and above a 24.1x peer average, yet below a 41.6x fair ratio that the market could move toward. For investors, that mix of premium pricing and theoretical headroom raises a simple question: is this justified strength or valuation risk if expectations cool?

Next Steps

With so much optimism and concern in the mix, it helps to see the full picture for yourself and decide where you stand. To weigh both sides in one place, review the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Amazon has your attention, do not stop there. Broaden your watchlist with other focused stock ideas that could sharpen your overall approach.

- Spot potential long term compounders by scanning a curated set of 46 high quality undervalued stocks that pair quality fundamentals with prices below one estimate of fair value.

- Strengthen your income focus by reviewing 10 dividend fortresses that combine higher yields with an emphasis on durability of payouts.

- Prioritize resilience by checking 64 resilient stocks with low risk scores that aim to keep overall risk scores on the lower side while still offering equity upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.