Assessing ASML Holding’s Valuation After Strong Share Price Momentum And Premium P/E Multiple

ASML Holding NV ADR ASML | 0.00 |

Recent share performance and business scale

ASML Holding (NasdaqGS:ASML) has drawn fresh investor attention after a recent move that left the stock around $1,550 at the last close, with year to date and 1 year total returns both in positive territory.

The company reports revenue of €33.7b and net income of €10.0b from its semiconductor equipment business, with returns over the past month, past 3 months and 5 years all positive according to the data provided.

That 6.2% 1 day share price return, combined with a 33.2% year to date share price return and a 1 year total shareholder return of 111.7%, suggests strong momentum that has built over time rather than a short lived spike.

If you are looking beyond ASML to see where else capital is moving in chip related infrastructure, this could be a good time to scan 44 AI infrastructure stocks

With the stock around $1,550, revenue of €33.7b and net income of €10.0b, the key question now is simple: are you looking at an undervalued chip equipment leader, or has the market already priced in future growth?

Price-to-earnings of 51.2x: Is it justified?

ASML trades on a P/E of 51.2x, which sits above the SWS fair P/E estimate of 42.9x, even though it is below several key peer benchmarks.

The P/E ratio links the current share price to earnings per share, so a higher figure typically means investors are willing to pay more today for each unit of current earnings. For a company selling critical semiconductor equipment, that kind of premium often reflects expectations around future order demand, margins and the durability of earnings rather than just what has been reported so far.

Here, ASML looks expensive relative to the estimated fair P/E of 42.9x, a level that the market could move back toward if expectations cool. Yet it still screens as good value compared with the US Semiconductor industry average P/E of 63x and a peer average of 52.1x. That mix of signals suggests the current multiple sits in a premium zone, but not at the very top of sector valuations.

Result: Price-to-earnings of 51.2x (ABOUT RIGHT)

However, you also need to weigh risks such as softer semiconductor equipment orders or delays in customer capex, which could quickly cool sentiment around the stock.

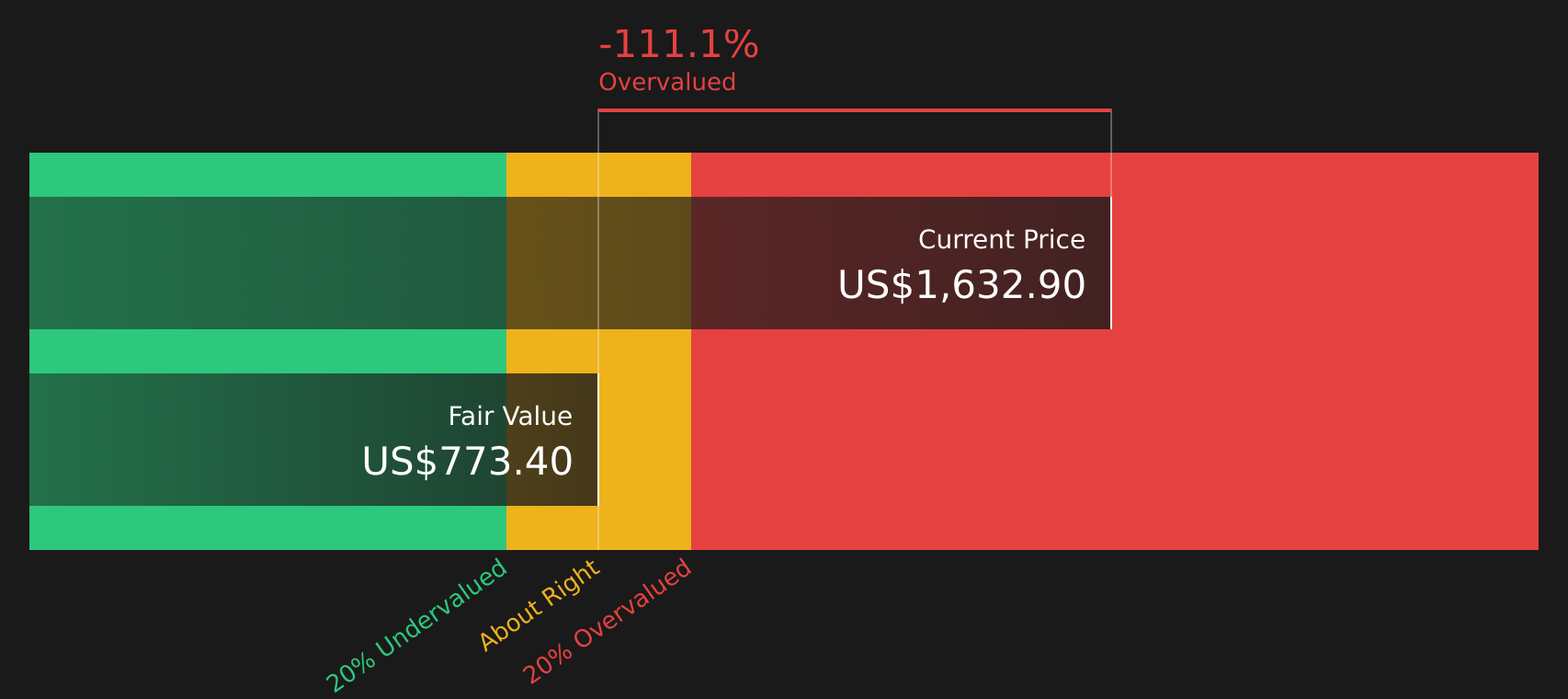

Another view: cash flows tell a different story

While the P/E of 51.2x looks roughly in line with peers, our DCF model presents a different perspective. With ASML at $1,550.13 and an estimated future cash flow value of $779.15, the stock appears overvalued on this framework, raising the question of how much optimism is already reflected in the price.

For a closer look at how the assumptions stack up, including growth, discount rates and cash flow forecasts, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ASML Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this all sounds optimistic, do not just take the headline multiples at face value. Instead, move quickly to review the underlying data and assumptions for yourself before weighing the 3 key rewards

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at a single stock. Use focused screeners to quickly surface fresh ideas that match your goals.

- Target quality at a discount by scanning 51 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their strengths.

- Strengthen your income stream by reviewing 10 dividend fortresses that aim to provide higher yields alongside resilient cash flows.

- Prioritise resilience by checking 67 resilient stocks with low risk scores designed to keep overall portfolio risk in check while still offering equity exposure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.