Assessing Energy Transfer (ET) Valuation As AI Contracts And New Gas Projects Support Multi Year Growth

Energy Transfer ET | 0.00 |

Energy Transfer (ET) is back in focus after lifting its 2026 adjusted EBITDA guidance, advancing new pipeline projects, and signing long-term natural gas transport contracts with AI data centers, all supported by strong first quarter results.

Those contract wins and project approvals appear to be feeding into momentum, with a 1 month share price return of 8.11% and year to date share price return of 22.91%, while the 5 year total shareholder return of 205.94% points to strong longer term compounding.

If the AI driven demand story around pipelines has your attention, it could be a good moment to look beyond Energy Transfer and scan 35 power grid technology and infrastructure stocks

With Energy Transfer trading at $20.39 and third party estimates pointing to an intrinsic discount of about 51%, the key question is simple: is there still real upside here, or is the market already pricing in future growth?

Most Popular Narrative: 8.4% Undervalued

Compared with the last close at $20.39, the most followed narrative pegs Energy Transfer's fair value at $22.26, describing a modest valuation gap that hinges on long dated gas projects and contracted cash flows.

The company's NGL export capacity expansions at the Nederland terminal and new pipeline loopings position it to benefit from increased U.S. hydrocarbon exports to international markets, supporting sustained throughput and export revenues as global energy demand rises.

Want to see what is baked into that fair value? Revenue growth, slightly higher margins, and a richer future earnings multiple all sit at the core of this narrative. Curious how those ingredients fit together and what analysts think they add up to by the late 2020s? The full story connects those moving pieces directly to that $22.26 figure.

Result: Fair Value of $22.26 (UNDERVALUED)

However, that upside story depends heavily on large, multi-year gas projects and long-term fossil fuel demand, where delays or weaker utilization could quickly challenge the thesis.

Another Angle On Valuation

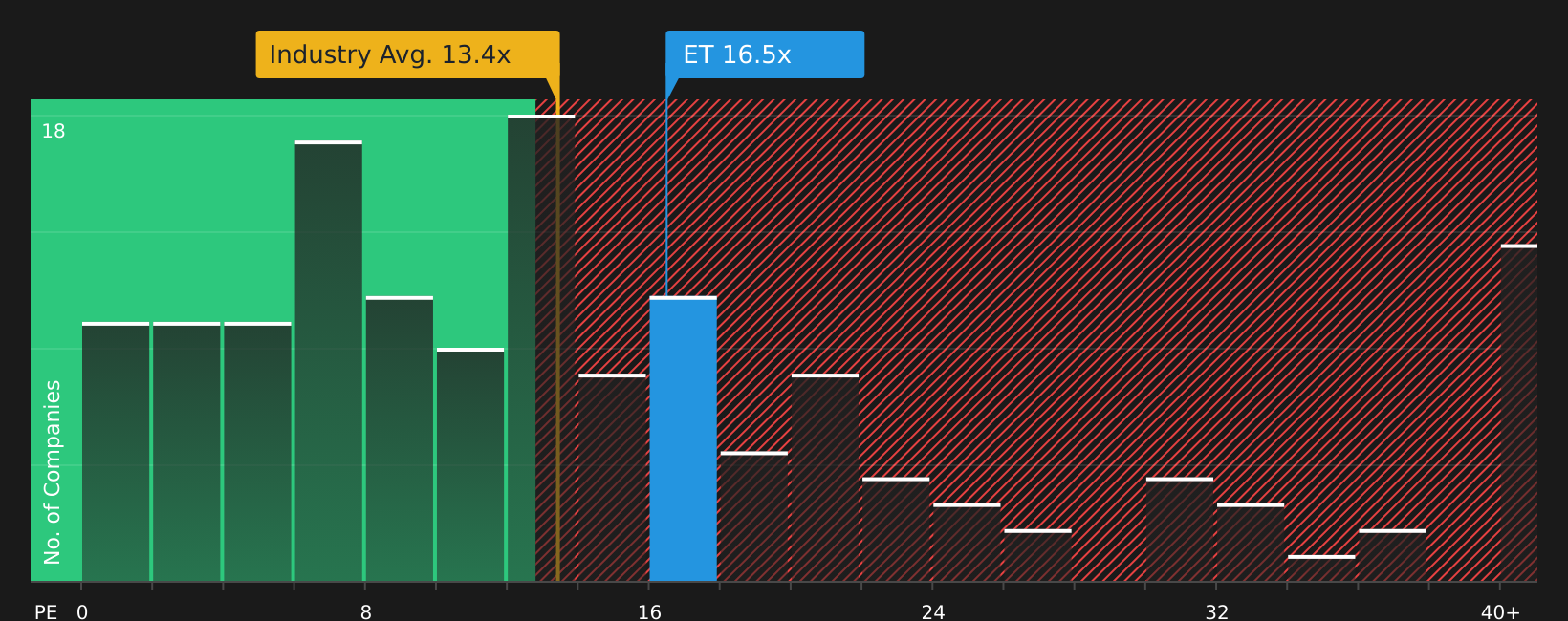

While the earlier narrative leans on future cash flows and growth assumptions, the current P/E of 17.1x paints a different picture. It is higher than the US Oil and Gas industry at 14.9x, but lower than peers at 19.5x and the fair ratio estimate of 29.8x. This raises a simple question: is this a risk premium or a potential opportunity?

Next Steps

Seeing both optimism and caution in this story and wondering where you land? Move quickly, review the key data points, and then weigh up the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If this story has you thinking more broadly about your portfolio, do not stop at a single stock when there are focused ideas you can review in minutes.

- Spot opportunities others might overlook by scanning the screener containing 21 high quality undiscovered gems.

- Strengthen your foundation with companies highlighted in the solid balance sheet and fundamentals stocks screener (46 results).

- Prioritize resilience and sleep better at night by reviewing the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.