Assessing Intuitive Surgical (ISRG) Valuation After Strong Q4 Results And New da Vinci 5 Cardiac Clearance

Intuitive Surgical, Inc. ISRG | 467.22 | +1.80% |

Event driven interest in Intuitive Surgical

Intuitive Surgical (ISRG) is back in focus after better than expected fourth quarter results and fresh FDA clearance expanding da Vinci 5 into cardiac procedures, prompting investors to reassess the stock’s risk reward profile.

Despite the latest 2.5% 1 day share price return taking Intuitive Surgical to $488.15, the 30 day share price return of 17.6% and 1 year total shareholder return of 16.3% highlight how the recent pullback contrasts with strong gains over three and five years. This comes as investors weigh upbeat quarterly results and new da Vinci 5 cardiac approvals against earlier enthusiasm.

If this FDA news has you thinking more broadly about medical technology, it could be worth scanning 26 healthcare AI stocks as a starting point for other potential ideas in the space.

With shares up strongly over three and five years but showing a 17.6% 30 day decline and a 16.3% 1 year total shareholder return, the real question is whether this pullback leaves Intuitive Surgical undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 18.1% Undervalued

Compared with Intuitive Surgical's last close at $488.15, the most followed narrative points to a fair value of about $596.36, supported by detailed revenue and margin assumptions under a 7.68% discount rate.

Strong global procedure growth (18% total; 17% da Vinci specifically), increasing installed base, and rising system utilization indicate that Intuitive is effectively capturing surging demand for minimally invasive, robotic-assisted surgeries as chronic disease rates rise and populations age globally, which directly supports long-term recurring revenue and margin stability.

Curious what underpins that higher fair value? The narrative leans on steady double digit top line expansion, firm margins, and a premium future earnings multiple that stands out for a medical equipment name.

Result: Fair Value of $596.36 (UNDERVALUED)

However, there are still real pressure points, including tighter hospital budgets in key regions and rising competition in instruments, that could challenge the bullish utilization story.

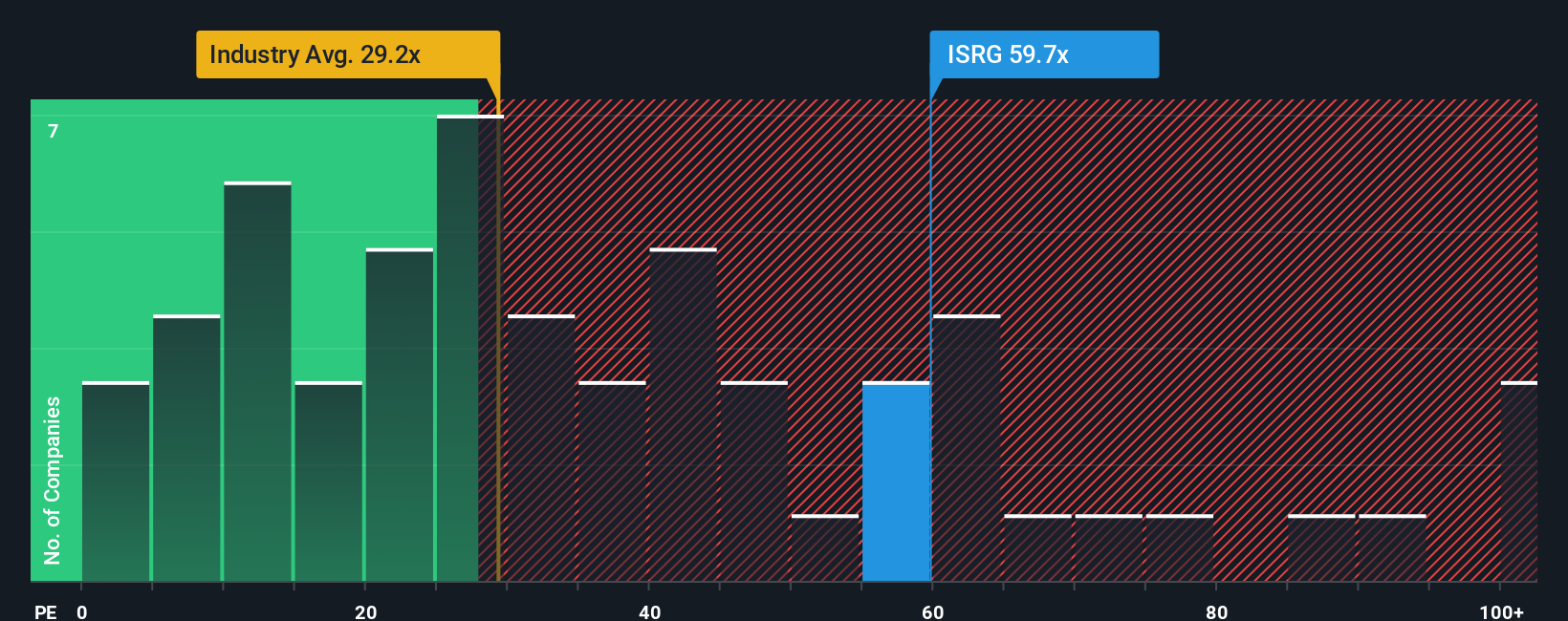

Another View: High P/E Puts The Brakes On The Bull Case

That 18.1% "undervalued" narrative runs into a very different message once you look at the current P/E. Intuitive Surgical trades on roughly 60.7x earnings, versus about 30.7x for the US Medical Equipment industry, 34.6x for peers, and a fair ratio of 37.6x that our models suggest the market could move towards. For you, that wide gap points more to valuation risk than a clear bargain. The real question is whether the quality of the business justifies paying this kind of premium multiple.

Build Your Own Intuitive Surgical Narrative

If you look at these numbers and come to a different conclusion, or just want to stress test the assumptions yourself, you can build a custom narrative in a few minutes by starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Intuitive Surgical.

Looking for more investment ideas?

You have seen how one company can spark fresh thinking. Now back that curiosity with a wider search so you do not miss other compelling opportunities.

- Spot potential value early by scanning screener containing 25 high quality undiscovered gems that have solid fundamentals but still fly under most investors' radar.

- Strengthen your foundation by checking solid balance sheet and fundamentals stocks screener (45 results) so you can focus on companies that pair resilience with quality financials.

- Put income on your radar through 14 dividend fortresses and quickly see which companies offer higher yields backed by durable business models.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.