Assessing KKR (KKR) Valuation After Insider Buying And Record Assets Under Management

KKR & Co KKR | 103.85 103.85 | +3.41% 0.00% Pre |

User interest in KKR (KKR) has picked up after a director bought 50,000 shares and the firm used a major conference to highlight record assets under management and its Arctos acquisition plans.

The recent insider purchase and focus on record assets under management come after a sharp reset in the share price, with a 30 day share price return of 22.59% decline and a year to date share price return of 21.08% decline, even though the 3 year total shareholder return of 86.75% and 5 year total shareholder return of 135.36% show that longer term holders have still seen strong gains. This suggests recent news and earnings are being weighed against a solid multi year track record.

If this mix of insider buying, acquisitions and fundraising has you thinking more broadly about private markets, it could be a good moment to scan 23 top founder-led companies as potential next ideas.

With KKR trading at $101.73 after a 30 day share price decline of 22.59% and an intrinsic value marker implying a premium, investors have to ask whether sentiment is too gloomy or the market is already pricing in future growth.

Most Popular Narrative: 35.2% Undervalued

KKR's widely followed narrative pegs fair value at about $157.10, well above the last close at $101.73, which puts a spotlight on its future fee and earnings potential.

Expansion of credit and asset-based finance platforms, with KKR now a leader in a $6 trillion+ market poised for further growth, provides a broader and more durable base of fee-related earnings while also increasing the potential for performance fees as these businesses scale. This diversification reduces earnings volatility and supports long-term earnings growth.

Curious what kind of earnings growth, margins and valuation multiple are baked into that fair value, and how analysts think KKR gets there from here? The full narrative lays it out in detail.

Result: Fair Value of $157.10 (UNDERVALUED)

However, the story can change quickly if fundraising slows under competitive pressure, or if credit and asset based finance exposures run into asset quality and liquidity issues.

Another View: Earnings Multiple Sends a Very Different Signal

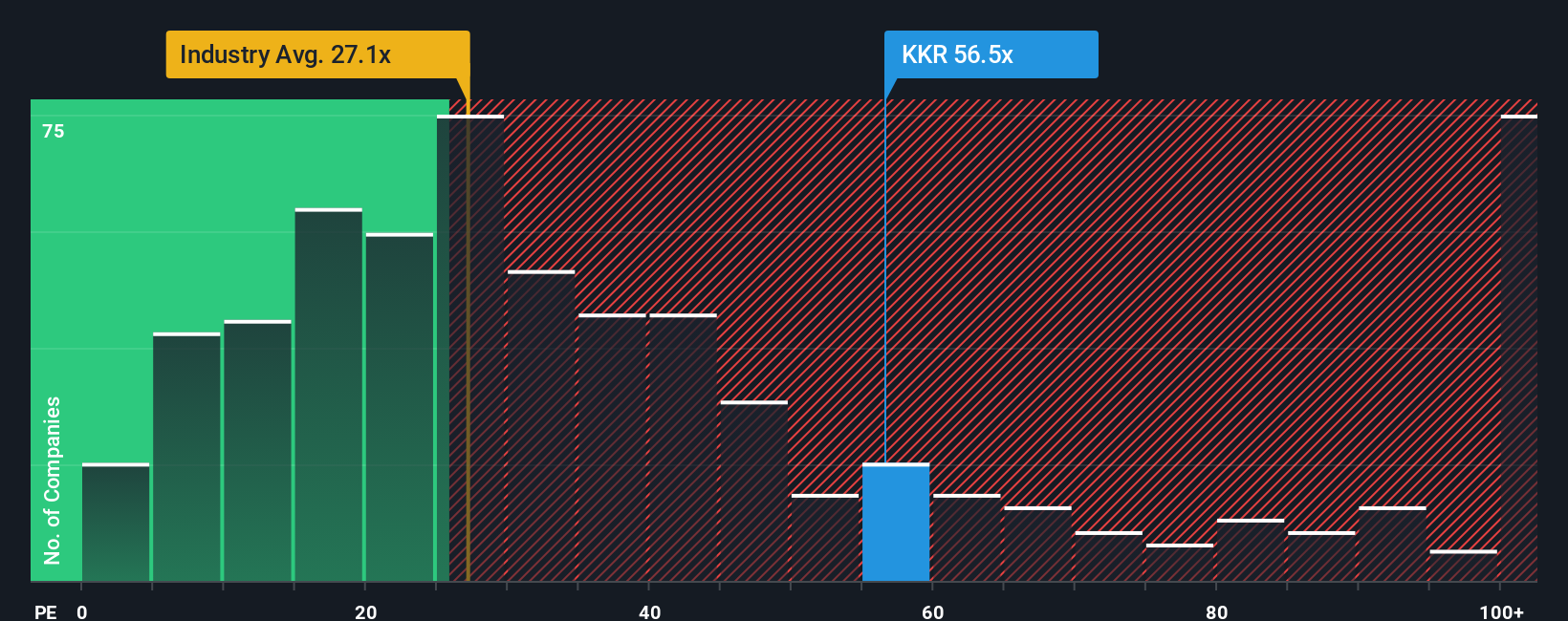

If you put the DCF work to one side and just look at the earnings multiple, KKR tells a different story. The shares trade on a P/E of 40.3x, compared with 23.1x for the US Capital Markets industry, 34.3x for peers, and a fair ratio of 27.4x.

That gap means you are paying a much higher price for each dollar of current earnings than both the sector and what the fair ratio suggests the market could move towards. The question is whether the long term growth narrative you have in mind is strong enough to justify that premium.

Next Steps

If the mixed signals in this article leave you on the fence, it makes sense to move quickly and review the numbers yourself, starting with 2 key rewards.

Looking for more investment ideas?

If this KKR story has you thinking bigger, do not stop here. The screener can surface other names you might wish you had checked sooner.

- Spot potential bargains early by scanning 55 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect their underlying strength.

- Prioritize staying power by reviewing solid balance sheet and fundamentals stocks screener (44 results) where companies show financial foundations that may better handle pressure.

- Target reliable income streams by checking 13 dividend fortresses that focus on companies with higher dividend yields.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.