Assessing Mastercard (MA) Valuation After Recent Share Price Weakness And Conflicting Undervaluation Signals

Mastercard MA | 0.00 |

Recent performance snapshot

Mastercard (MA) has drawn fresh attention as the stock has slipped, with the share price down about 1% over the past day, 1% over the past week and 2% over the past month.

Looking beyond the recent pullback, Mastercard’s share price has declined 12.45% year to date, while its 3 year total shareholder return of 36.54% and 5 year total shareholder return of 41.07% point to a steadier long term record. This suggests current weakness reflects a period of fading momentum rather than a break in the broader story.

If you are weighing Mastercard alongside other opportunities in payments and financial infrastructure, it can help to widen the lens with a curated set of founder led compounders by checking the 20 top founder-led companies

With Mastercard’s share price weaker this year, solid recent revenue and net income growth near 10% and some valuation models pointing to a discount, are you looking at a genuine entry point, or is future growth already priced in?

Most Popular Narrative: 14.9% Undervalued

Against the last close at $493.01, the leading narrative for Mastercard points to a fair value of $579.41, suggesting the market price lags that thesis.

Diversified, non-card revenue growth: increasing value-added services (data/analytics, security, gateway) enhance revenue per transaction and reduce pure-volume dependence.

Have a read of the narrative in full and understand what's behind the forecasts. Read the complete narrative.

Curious what kind of revenue growth, margins and future earnings multiple are baked into that figure? The narrative focuses on long term cash generation and capital returns. The full story links those elements into a single valuation roadmap.

Result: Fair Value of $579.41 (UNDERVALUED)

However, tighter regulation or faster adoption of alternative payment rails could cap pricing power and weaken the long term cash flow story behind that valuation.

Another angle on valuation

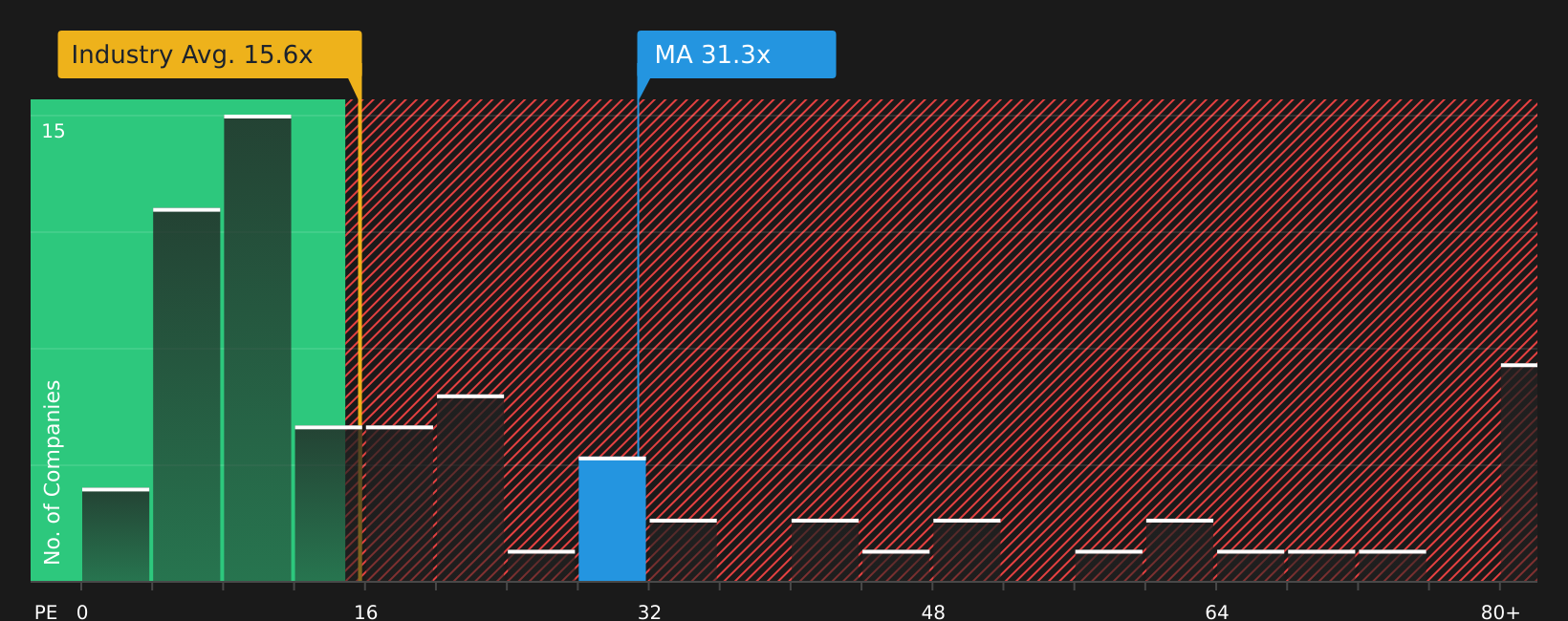

While the user narrative points to a fair value of $579.41 and calls Mastercard undervalued, the current P/E of 28x is higher than both the US Diversified Financial industry at 17.9x and peers at 24x, and above a fair ratio of 20.3x. This points to valuation risk if sentiment cools.

For a closer look at how those earnings multiples stack up against what the fair ratio suggests the market could move toward, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals on valuation, risks and rewards, now is the moment to look through the numbers yourself and decide where you stand, starting with the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Mastercard is only one part of your watchlist, now is a good moment to look more broadly so you do not miss other potentially compelling setups.

- Explore potential mispricing by scanning 46 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect them.

- Focus on resilience by reviewing 65 resilient stocks with low risk scores that score well on financial stability and business risk.

- Look for potential future leaders at an early stage by checking the screener containing 22 high quality undiscovered gems before the wider market focuses on them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.