Assessing Nike (NKE) Valuation As Shares Rebound After Recent Volatility

NIKE, Inc. Class B NKE | 0.00 |

NIKE (NKE) is back in focus after recent share price volatility, with the stock closing at US$44.19. Investors are weighing this move in relation to the company’s current earnings profile and recent return trends.

The recent 4.2% 1 day share price gain and 4.4% 7 day share price return come after a tougher spell, with the 90 day share price return down 32.7% and the 3 year total shareholder return declining 56.8%. This suggests recent momentum is trying to rebuild from a weaker long term trend.

If this kind of volatility has you looking beyond a single consumer stock, it could be a good moment to broaden your watchlist with 20 top founder-led companies

With NIKE stock down sharply over the past year, yet trading below some analyst price targets and with recent revenue and net income growth, you now face a key question: is this a buying opportunity, or is future growth already priced in?

Most Popular Narrative: 49.7% Undervalued

According to the most followed narrative on NIKE, the fair value sits at $87.90, well above the recent close at $44.19, which sets up a very different picture from the recent share price slide.

Most Immediate Catalysts (1–2 Years)

• DTC Growth Acceleration: Nike is prioritizing Nike.com, SNKRS, and flagship stores, improving margins and reducing reliance on wholesalers.

• Innovation in Running & Performance: Launch of Alphafly 3, Vaporfly 4, and next-gen sportswear can drive higher demand.

• Women’s Market Expansion: Increasing focus on women’s footwear & apparel through exclusive collections and athlete partnerships.

• Cost-Saving Initiatives: Efficiency programs (including layoffs) aimed at improving margins.

Want to see what justifies almost half the current price being added on top? The narrative leans heavily on rising profitability, faster earnings growth and a richer future earnings multiple. Curious how those inputs fit together and what kind of long term revenue path is being assumed to reach that $87.90 figure? The full breakdown connects each of these moving parts to that fair value call.

Result: Fair Value of $87.90 (UNDERVALUED)

However, this upbeat view could be knocked off course if competition continues to chip away at market share, or if China and wholesale partners remain structurally weaker.

Another Take on NIKE’s Value

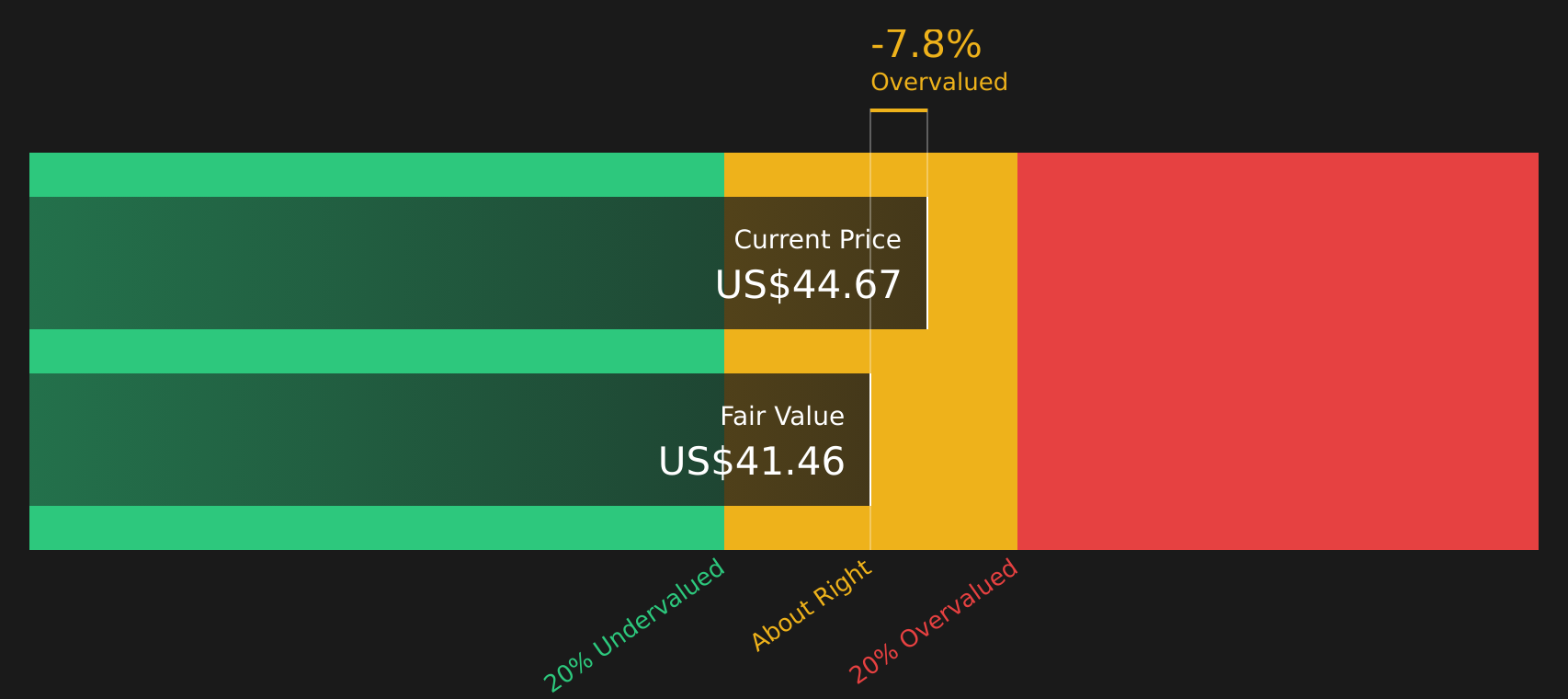

Our DCF model points in a different direction to the popular undervalued narrative, with NIKE at $44.19 trading above an estimated future cash flow value of $41.48. That suggests a modest premium, raising the question of whether the bullish fair value assumptions are too generous.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NIKE for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on value and sentiment running in both directions, it makes sense to move quickly, test the assumptions yourself, and weigh 1 key reward and 2 important warning signs.

Ready to hunt for more investment ideas?

NIKE might be front of mind today, but your next strong idea could come from stocks you have not checked yet, so do not leave that on the table.

- Target steadier opportunities by reviewing companies screened as 67 resilient stocks with low risk scores, which aim for resilience when conditions get choppy.

- Spot potential value plays by scanning 51 high quality undervalued stocks, which combine quality fundamentals with prices that may not fully reflect them.

- Get ahead of the crowd by searching screener containing 21 high quality undiscovered gems before they land on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.