Assessing Nvidia (NVDA) Valuation After New AI Infrastructure Deals With Corning And IREN

NVIDIA Corporation NVDA | 0.00 |

NVIDIA (NVDA) stock has been in focus after the company announced two large infrastructure deals: one with Corning to expand U.S. optical manufacturing and another with IREN to deploy up to 5 gigawatts of AI capacity.

Those infrastructure deals have arrived while momentum in the stock has picked up, with a 30 day share price return of 18.75% and year to date share price return of 11.99%, on top of a 1 year total shareholder return of 80.24%. This suggests investors are responding to both current execution and NVIDIA's role in the broader AI build out.

If you want to see what else is moving as AI infrastructure expands, it is worth scanning other potential opportunities using our 40 AI infrastructure stocks

With NVIDIA now valued at about US$5,049b and the stock up 6.41x over three years, plus trading roughly 27% below the average analyst price target, the key question is simple: is this still an opportunity, or is the market already pricing in what comes next?

Most Popular Narrative: 24.2% Overvalued

According to the most followed narrative, NVIDIA's fair value sits at $170.26 compared with the last close at $211.50, implying a premium that the market is currently paying.

$400b annual revenue assumes Nvidia continues to be dominant in GPU design and AI software stack. Successful competition from AMD, Intel, or a Chinese firm could undermine this. Uptake of an open-source, cheaper, or better platform than Nvidia's CUDA would heavily undermine Nvidia's moat and enable any sizeable firm to directly engage semiconductor manufacturers, such as TSMC, to produce their own chips, stealing away Nvidia's high margin products (similar to what Apple did with its M-Series chips).

Want to see how this revenue ambition translates into that fair value estimate? According to KiwiInvest, the story hangs on aggressive data center growth, rich margins and a premium future earnings multiple.

Result: Fair Value of $170.26 (OVERVALUED)

However, the narrative could still shift quickly if competitors win meaningful GPU or AI software share, or if tighter regulation slows data center investment.

Another View on Value: Earnings Multiple vs Fair Ratio

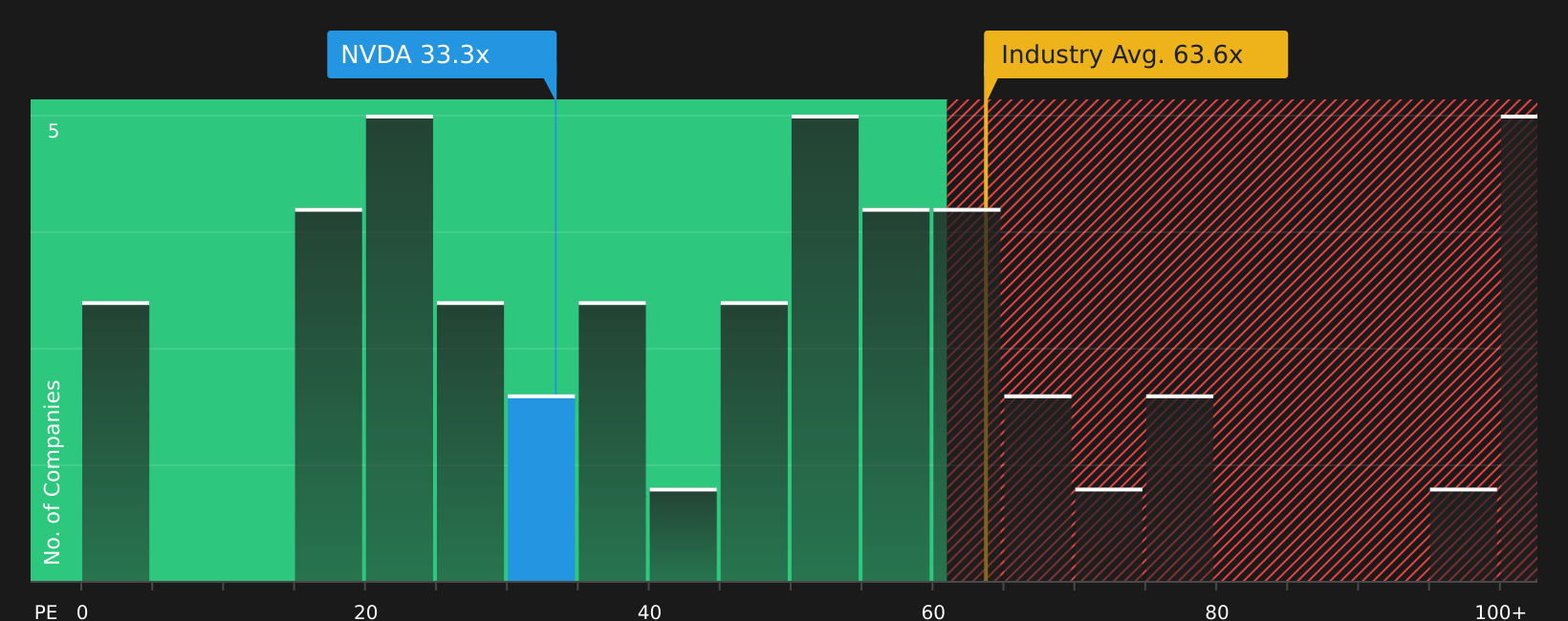

The narrative above treats $170.26 as fair value, implying NVIDIA is 24.2% overvalued at $211.50. Yet the current P/E of 42.8x sits well below both the US Semiconductor industry average of 59.4x and a peer average of 73x, and below an estimated fair ratio of 51.9x.

That gap suggests the market is already pricing in strong expectations, but not at the top end compared with peers or the fair ratio that prices could move toward. This leaves you weighing whether this is a cushion against downside or a sign expectations still need to be tested.

Next Steps

With mixed signals on valuation and growth expectations, now is the time to look through the numbers yourself, weigh both sides, and decide how comfortable you are with the trade off between risk and reward by reviewing the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If NVIDIA feels richly debated, broaden your watchlist now. Some of the most interesting opportunities often sit just outside the headlines.

- Focus on quality at a discount by scanning companies that combine strong fundamentals with attractive pricing using the 51 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks that aim to offer resilient 5%+ yields and robust payout profiles through the 12 dividend fortresses.

- Dial back risk while staying invested by filtering for companies with healthier balance sheets and steadier financial profiles using the 72 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.