Assessing Nvidia (NVDA) Valuation After Record Results Dividend Hike And US$80b Buyback

NVIDIA Corporation NVDA | 0.00 |

NVIDIA (NVDA) just reported record quarterly results, paired with a 25x dividend increase to US$0.25 per share and a new US$80b buyback. This puts capital returns and AI growth firmly in focus for shareholders.

Despite a slight pullback around the results, with the share price down 1.9% over the last day and 4.4% over the past week, NVIDIA still shows firm momentum, with a 30 day share price return of 3.4% and a 1 year total shareholder return of 64.1% on the back of record AI demand, Vera CPU announcements and the expanded capital return program.

If NVIDIA’s results have you rethinking your AI exposure, this is a good moment to look beyond the giants and see what else is emerging in AI infrastructure through 46 AI infrastructure stocks

With record revenue, a very large dividend hike and a US$80b buyback now on the table, NVIDIA is clearly rewarding shareholders. At a US$5.2t market cap, however, is the stock still mispriced or already reflecting years of future AI growth?

Most Popular Narrative: 36.6% Undervalued

Compared to NVIDIA’s last close of $215.33, the most followed narrative on Simply Wall St sees fair value at $339.90, which implies a sizeable valuation gap and puts long term AI demand assumptions front and center.

Nvidia will hit $400b annual revenue in 5 years time. ~90% of revenue will come from data centre customers. This equates to $90b / quarter, or equivalent to 30,000 Blackwell racks (at ~$3m per rack).

According to KiwiInvest, this fair value rests on bold revenue concentration in data centers, aggressive rack deployments and sustained AI hardware refresh cycles. It also raises the question of what growth path and margin structure are incorporated into that view.

Result: Fair Value of $339.90 (UNDERVALUED)

However, this depends on NVIDIA maintaining its lead in AI software and avoiding major regulatory or power supply constraints that could slow data center demand and spending.

Another View Using Our DCF Model

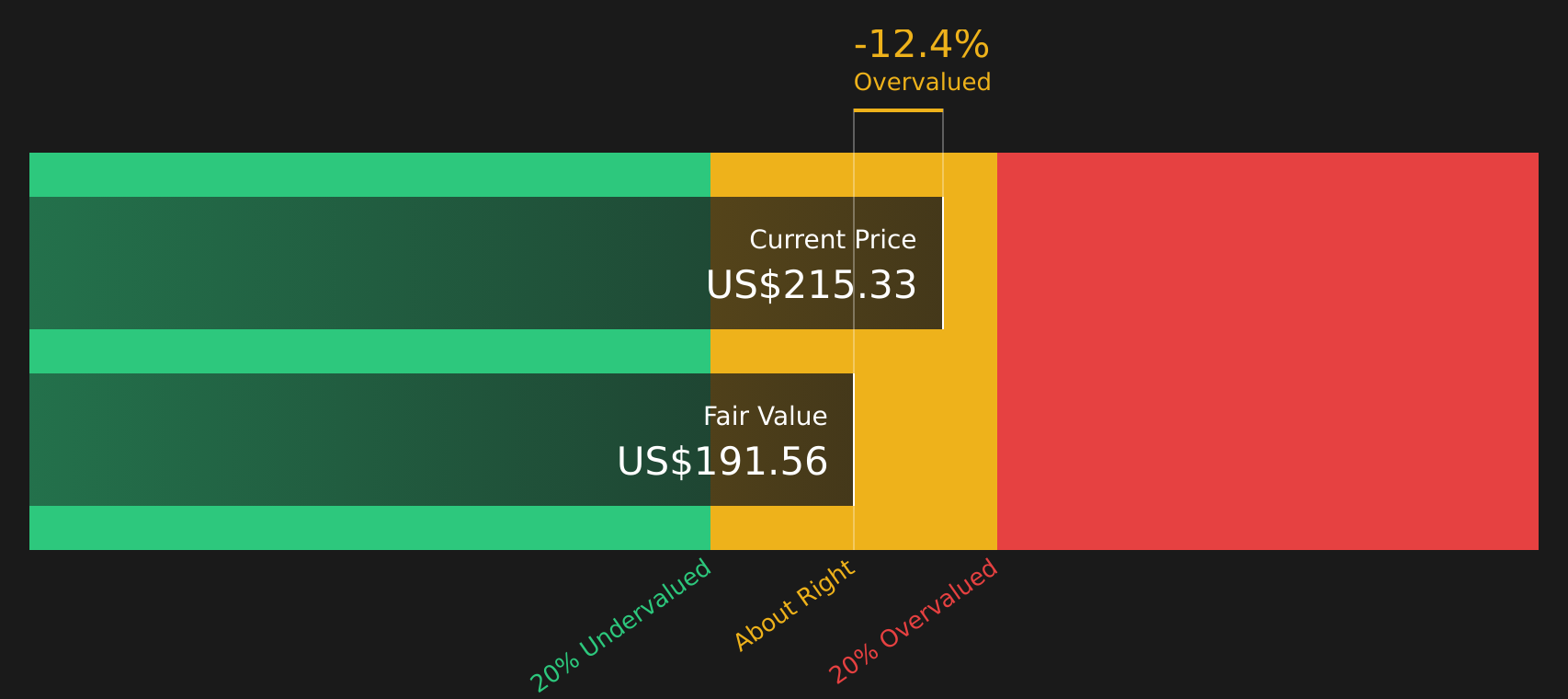

The user narrative points to a fair value of $339.90 and frames NVIDIA as undervalued, but our DCF model tells a different story. On that basis, the stock at $215.33 is above an estimated fair value of $191.56, which indicates possible downside if cash flows do not scale as quickly as hoped.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NVIDIA for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals on value, risk and reward, it helps to review the details yourself and quickly decide where you stand on NVIDIA’s story using 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If NVIDIA feels fully priced, do not stop there. Use focused stock lists to quickly spot other opportunities that might fit your approach.

- Target potential mispricing by scanning companies flagged as 49 high quality undervalued stocks to see which stocks the data suggests may not match their current share prices.

- Strengthen your income stream by reviewing stocks in the 10 dividend fortresses and see which yields stand out alongside those payouts.

- Prioritise resilience by checking companies in the 67 resilient stocks with low risk scores so you are not the last to notice which stocks score well on risk controls.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.