Assessing Paysign (PAYS) Valuation After Record Q1 Results And Patient Affordability Shift

Paysign, Inc. PAYS | 0.00 |

Paysign (PAYS) is back in focus after reporting record first quarter 2026 results, with revenue of US$28.04 million and net income of US$5.44 million, while its patient affordability business became the largest contributor.

The share price has been volatile around these earnings, slipping 2.94% on the day and 9.65% over the past week. However, the 90 day share price return of 65.78% and 1 year total shareholder return of 55.89% still point to strong recent momentum off a lower base.

If Paysign’s move has you thinking about where else growth and risk might be repriced, it can help to scan a broader set of ideas through 19 top founder-led companies

With the stock up 65.78% over 90 days yet still trading at a steep discount to the average analyst price target of US$9.95, you have to ask: is Paysign undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 53.2% Undervalued

With Paysign last closing at $5.62 against a widely followed fair value of $12.00, the most popular narrative frames the stock as heavily discounted while hinging on a major shift in where future profit comes from.

While analyst consensus expects pharma patient affordability revenue to more than double in 2025, the extraordinary pace of new program wins and deep customer value creation, already surpassing last year's savings for clients just four months into the year, signals the potential for hyper growth at well beyond projected rates, with this segment rapidly overtaking plasma as the main driver of total revenue and margin expansion.

Want to see what sits behind that patient affordability story? The narrative leans on steep revenue compounding, rising margins and a richer earnings base driving that $12.00 fair value.

Result: Fair Value of $12.00 (UNDERVALUED)

However, that upside story can crack if plasma related revenue continues to fall or if tighter regulation squeezes interchange fees and pushes margins lower than analysts expect.

Another Way To Look At Paysign’s Valuation

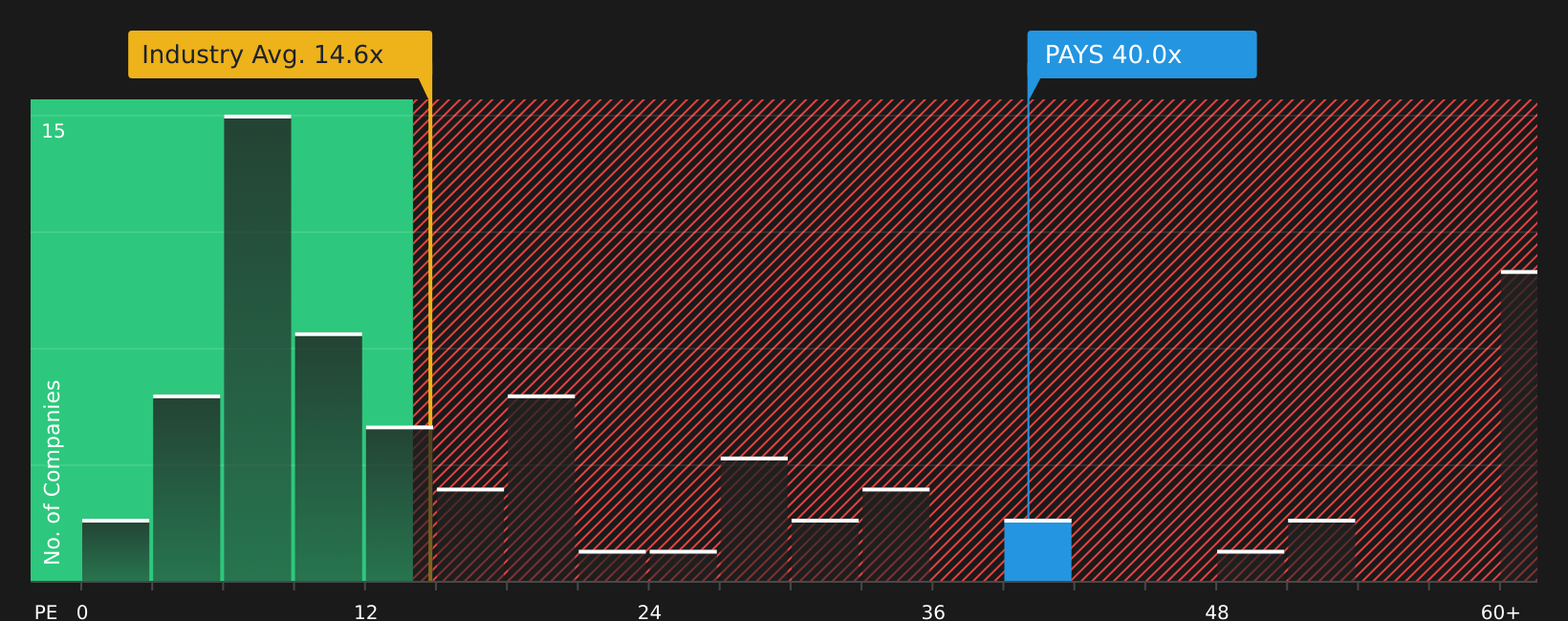

The narrative pegs fair value at $12.00, yet Paysign currently trades on a P/E of 30.2x versus a fair ratio of 20.6x and a peer average closer to 17x. That richer multiple can point to valuation risk if growth or margins fall short, so which story do you think the market is really paying for?

To see how that richer P/E compares with what the numbers suggest the ratio could move toward, take a closer look at our breakdown of Paysign’s valuation drivers through See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With the bullish and cautious takes laid out, the real question is where you land. Review the numbers, weigh the trade offs, and then check the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Paysign has sharpened your focus, do not stop here. The next move could come from finding a stock that fits your goals even better.

- Target income potential by checking out 12 dividend fortresses that might suit a portfolio built around regular cash returns.

- Hunt for quality at a discount by scanning screener containing 22 high quality undiscovered gems before the crowd starts paying attention.

- Dial up resilience in your portfolio by assessing 66 resilient stocks with low risk scores that aim to keep volatility in check.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.