Assessing RTX (RTX) Valuation After New Defense Wins And Secure Communications Progress

RAYTHEON TECHNOLOGIES CORPORATION RTX | 0.00 |

RTX (RTX) is back in focus after a series of defense wins, including fresh DARPA funding for composable rocket motors, new Javelin launcher deliveries to the U.S. Army, and progress on secure military communications systems.

RTX’s recent defense contract wins and technology milestones come as the stock trades at US$178.97, with short term share price momentum soft after a 90 day share price return that declined 8.68%. However, long term total shareholder returns of 35.50% over 1 year and 105.44% over 3 years suggest buyers have been rewarded over time.

If RTX’s contract pipeline has your attention, it can be useful to see what else is moving in related areas and find 35 power grid technology and infrastructure stocks

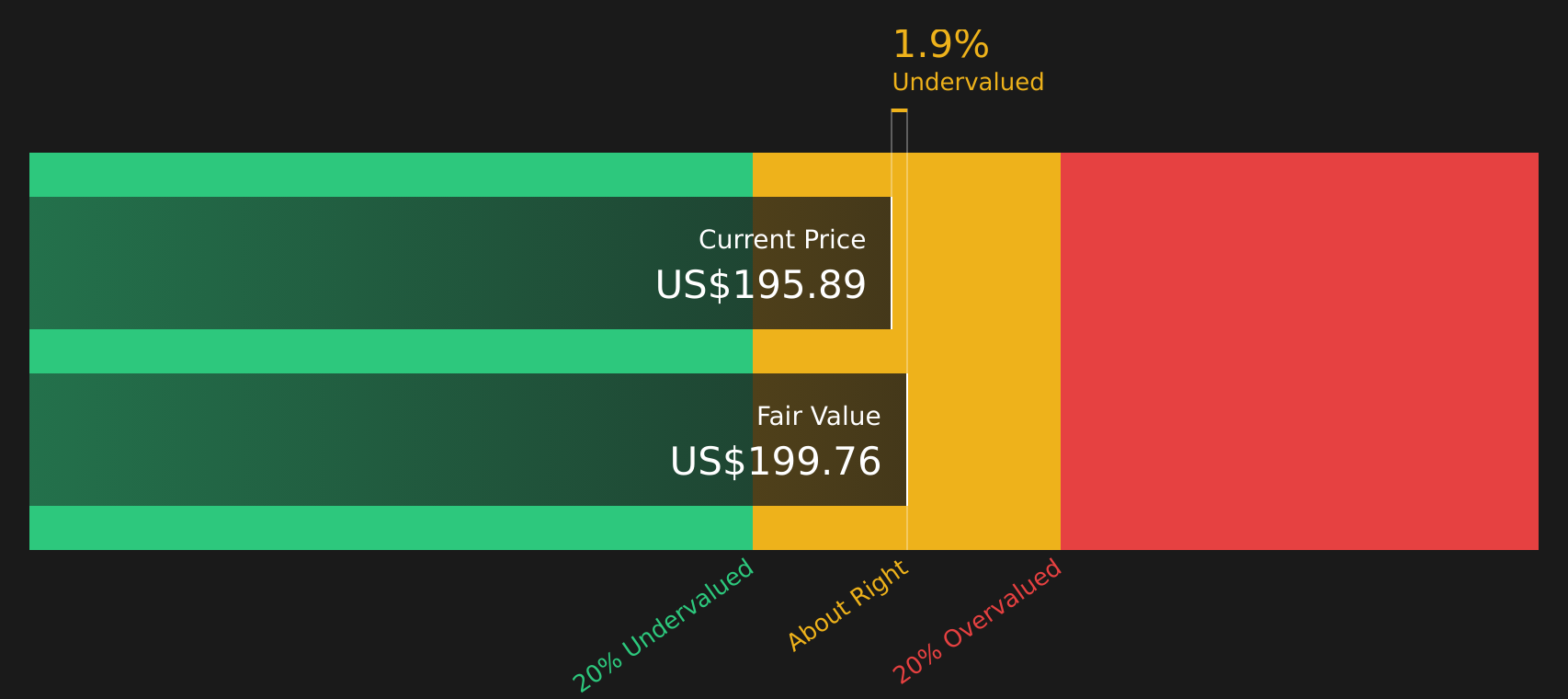

With RTX shares at US$178.97, trading below the average analyst price target but at a small premium to one intrinsic value estimate, you have to ask: is this defense heavyweight still mispriced, or is the market already baking in future growth?

Most Popular Narrative: 16.9% Undervalued

RTX’s most followed valuation narrative points to a fair value of $215.27 per share versus the last close at $178.97. This frames the current price as a discount that hinges on specific growth and margin assumptions.

Accelerated ramp in both commercial aerospace OE and aftermarket (mid-teens aftermarket growth and high single digit OE growth expected for the year), combined with persistent low aircraft retirement rates and expanding air travel in emerging markets, are driving higher recurring revenues and margin expansion in RTX's commercial segments supporting future earnings growth.

Want to see what sits behind that confidence in future earnings and margins? The narrative leans on steady revenue compounding, fatter profit margins, and a higher future earnings multiple that has to hold up over time.

Result: Fair Value of $215.27 (UNDERVALUED)

However, this upbeat story can quickly change if jet engine reliability issues at Pratt & Whitney resurface or if tariff and trade tensions squeeze RTX’s margins.

Another View: Cash Flows Paint a Different Picture

There is also a more cautious read on RTX using the SWS DCF model. On this view, RTX at US$178.97 is trading above an estimated future cash flow value of US$167.94. This points to the stock looking slightly overvalued rather than 16.9% undervalued. Which interpretation aligns more closely with your expectations?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out RTX for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on valuation and sentiment, this is a moment to look at the data yourself, weigh both sides, and move quickly to form a clear view using 5 key rewards and 2 important warning signs

Looking for more investment ideas?

If RTX has sharpened your focus, do not stop here. Use the Simply Wall St screener to uncover other opportunities that could fit your portfolio goals.

- Target potential mispricing by scanning 46 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their underlying economics.

- Build a steadier income stream by searching for 10 dividend fortresses that aim to pair higher yields with resilient cash generation.

- Prioritise capital preservation by focusing on 65 resilient stocks with low risk scores that score well on financial strength and volatility measures.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.