Assessing Seadrill (SDRL) Valuation After West Saturn Contract Extension Boosts Backlog

Seadrill Limited SDRL | 45.97 45.97 | -0.09% 0.00% Pre |

Seadrill (SDRL) is back in focus after Equinor Brasil Energia Ltda exercised a one year priced option on the ultra deepwater drillship West Saturn, adding US$114 million to Seadrill's contract backlog.

The latest Equinor contract option comes on the back of a strong run in Seadrill's share price, with a 20.92% 1 month share price return, 41.87% 3 month share price return and 22.06% year to date share price return, alongside a 36.99% 1 year total shareholder return. This hints at improving sentiment toward its backlog and earnings visibility.

If this kind of contract driven story has your attention, it may be a good moment to look at our screener of 21 elite gold producer stocks as another way to find resource related opportunities.

With Seadrill trading at US$42.66 against an average analyst price target of US$45.50 and an intrinsic value estimate that is lower than today’s price, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 1.9% Undervalued

Seadrill’s most followed narrative sees fair value at $43.50, sitting just above the recent $42.66 close, which puts every assumption under the microscope.

Supply of competitive ultra-deepwater rigs remains tight due to minimal newbuilds and uneconomical reactivations, positioning Seadrill's high-spec fleet for greater pricing power and margin improvement as the market rebalances, ultimately benefiting net margins and profitability.

Want to see what sits behind that pricing power argument? The narrative leans on a specific mix of revenue growth, margin expansion and a lower future earnings multiple. The exact mix may surprise you.

Using an 8.13% discount rate, the narrative pulls together expected top line growth, margin expansion and future earnings to land at a fair value of $43.50. That sits only slightly above the current share price, so even small changes in assumptions on revenue, earnings or required return can shift the implied upside quickly.

Result: Fair Value of $43.50 (ABOUT RIGHT)

However, softer utilization, rising competition, and the risk of aging rigs needing heavy investment could all pressure margins and challenge the optimistic earnings path.

Another Angle on Seadrill’s Valuation

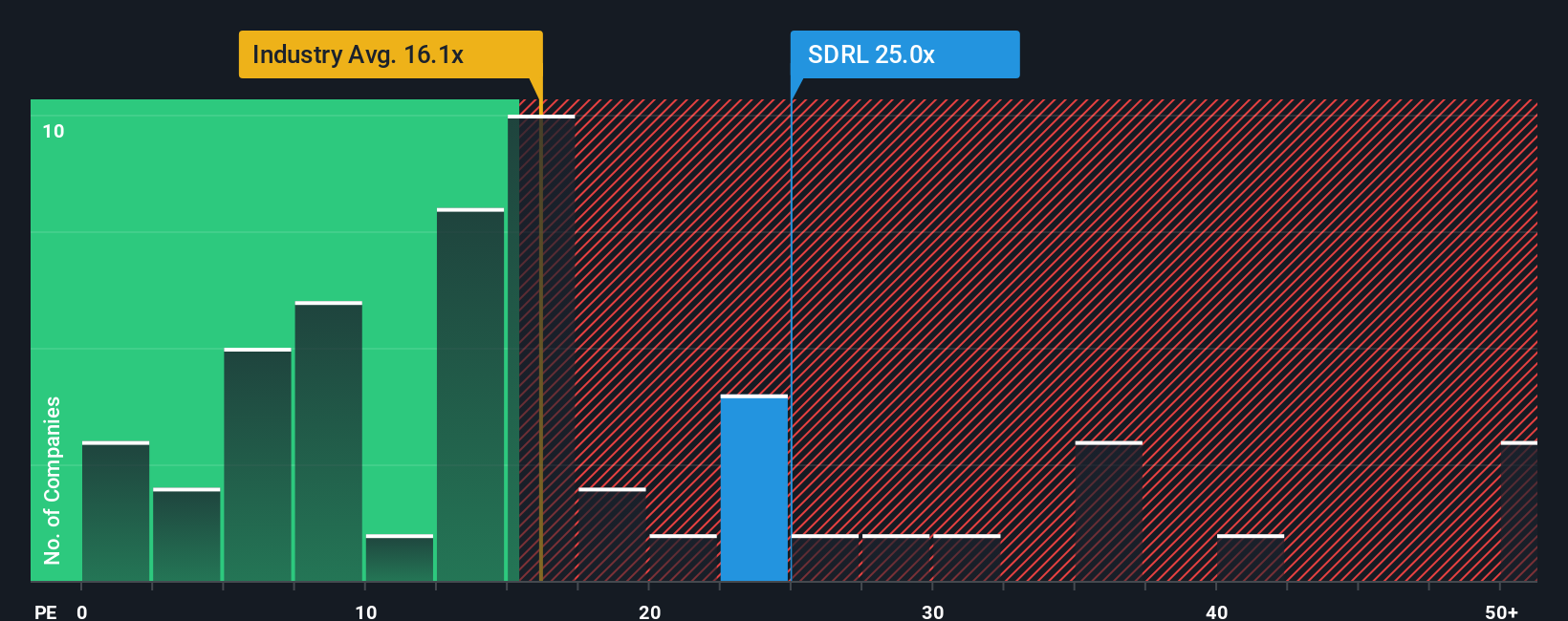

Here is where things get interesting. On a P/E of 75.5x, Seadrill trades well above the US Energy Services industry at 25x, its peer average of 18.4x, and even our fair ratio of 51.1x. That gap points to valuation risk if expectations cool.

Build Your Own Seadrill Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a custom Seadrill view in a few minutes: Do it your way.

A great starting point for your Seadrill research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready to Find Your Next Idea?

If Seadrill has you thinking more broadly about where to put fresh capital, do not stop here. Widen your opportunity set and see what else stands out.

- Spot potential mispricings early by scanning our list of 55 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect them yet.

- Strengthen your income stream by reviewing 16 dividend fortresses that combine higher yields with a focus on staying power.

- Sleep easier at night by checking 85 resilient stocks with low risk scores filtered for resilience on both financial and risk measures.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.