Assessing Sempra (SRE) Valuation After Earnings Beat And Ongoing Analyst Optimism

Sempra SRE | 95.39 | -0.08% |

Sempra (SRE) is back in focus after its latest earnings topped analyst expectations, with Q3 2025 revenue of US$3.2b and adjusted EPS of US$1.11, even as the stock trails its sector.

The share price, now at US$87.36, has slipped over the last quarter with a 6.79% 90 day share price return, even as the 1 year total shareholder return of 10.05% signals steadier long term momentum supported by dividends.

If this earnings beat has you looking at other parts of the energy value chain, our screener of 24 power grid technology and infrastructure stocks is a handy way to spot more grid focused opportunities.

So with earnings ahead of expectations, a 1 year total return of 10.05% and the share price sitting below analyst targets, is Sempra offering a reasonable entry point, or is the market already pricing in future growth?

Most Popular Narrative: 12.3% Undervalued

Compared with the current $87.36 share price, the most followed narrative pegs Sempra's fair value closer to $99.60, suggesting meaningful upside according to that framework.

The rollout and completion of major LNG export projects (ECA Phase 1 nearing completion, Port Arthur Phase 1 advancing, and strong commercial momentum for Phase 2) positions Sempra to benefit from sustained global demand for U.S. LNG as a transition fuel, significantly increasing future cash flows and long-term revenue generation.

Curious how a regulated utility gets to that higher fair value? The narrative leans heavily on steadier earnings growth, firmer margins, and a future earnings multiple that assumes investors keep paying up for that profile.

Result: Fair Value of $99.60 (UNDERVALUED)

However, there are still real swing factors here, including regulatory shifts in California or Texas and LNG project or policy setbacks that could undermine those fair value assumptions.

Another View: Market Multiple Sends a Different Signal

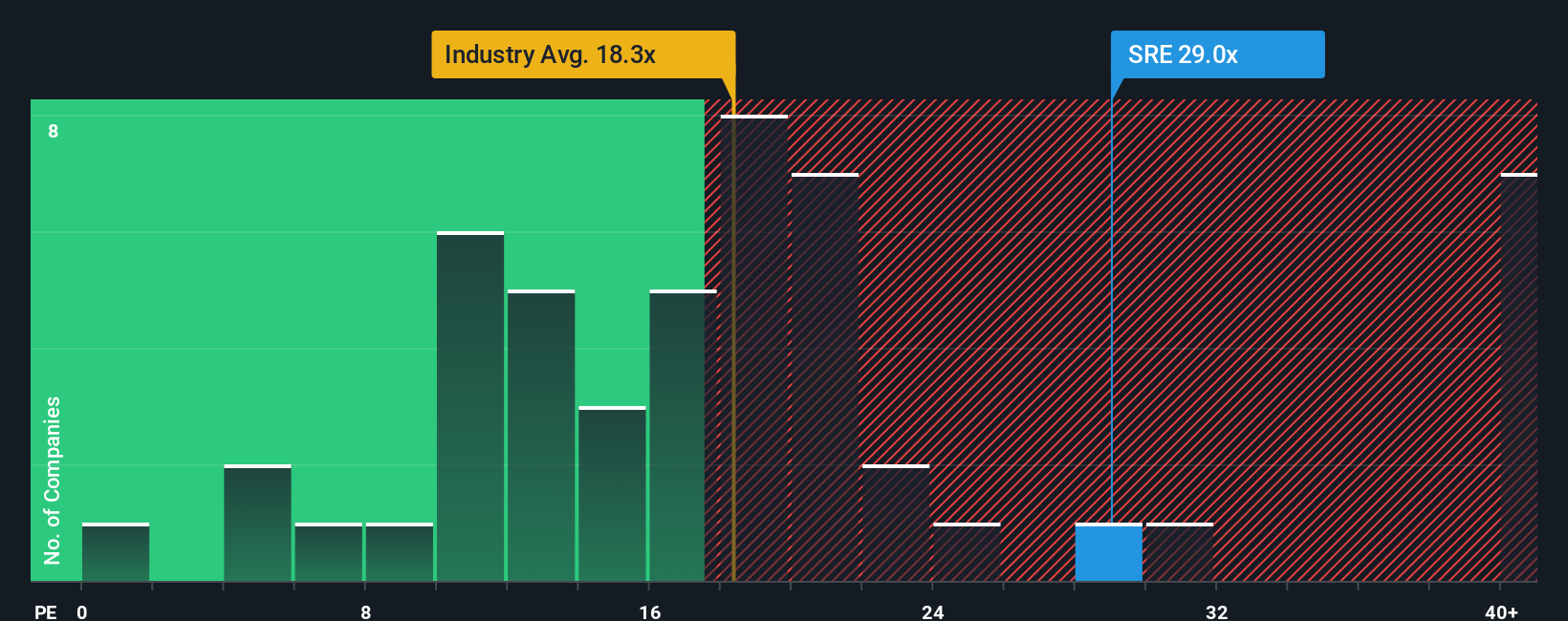

That 12.3% undervalued fair value of $99.60 sits awkwardly alongside the current P/E of 27x, which is higher than both the global Integrated Utilities industry at 19.2x and Sempra's own fair ratio of 28.8x. Is this a quality premium investors are comfortable paying, or a valuation risk?

Build Your Own Sempra Narrative

If you see the story differently or just want to test your own assumptions against the numbers, it is quick to build and refine a custom view with Do it your way

A great starting point for your Sempra research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop at Sempra, you could miss other opportunities that better match your goals, so put a few minutes into scanning the broader market with purpose.

- Spot potential value opportunities early by checking companies highlighted in our 53 high quality undervalued stocks, where price and fundamentals line up more tightly.

- Strengthen your focus on resilience by reviewing our 86 resilient stocks with low risk scores, built around businesses with more measured risk profiles.

- Get ahead of the crowd by browsing our screener containing 24 high quality undiscovered gems, a set of under the radar names with solid underlying numbers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.