Assessing Super Micro Computer (SMCI) Valuation After Strong Q3 AI Momentum And Ongoing Legal Risks

Super Micro Computer, Inc. SMCI | 0.00 |

Super Micro Computer (SMCI) is back in focus after its fiscal third quarter, where stronger gross margins, confident revenue guidance, and fresh AI data center partnerships, including nuclear-powered concepts, pulled attention away from ongoing legal questions.

The recent AI partnerships and earnings surprise have helped the stock regain momentum, with a 30 day share price return of 48.3% and year to date share price return of 8.59%. Over the past 5 years, the total shareholder return is very large at about 9x.

If this AI infrastructure story has your attention, it can be useful to see what else is moving in the space by scanning 40 AI infrastructure stocks

With the stock still below prior highs, trading close to analyst targets and carrying both strong AI momentum and serious legal overhangs, the key question is simple: is SMCI undervalued, or is the market already pricing in the next leg of growth?

Most Popular Narrative: 54.9% Undervalued

The narrative fair value of $74.53 sits well above the last close at $33.62, which immediately raises a question about what is driving such a wide gap.

Using management guidance of $23bn for 2025 and $40bn for 2026, I decided to use a revenue growth rate of 50% to reach an estimated revenue of $50bn for 2028 (conservative in my view). Using their TTM net profit margin of 6.64% and a conservative forward PE of 20x. With the aforementioned assumptions my fair value estimate for SMCI stock is at least $74.7 using a 3y exit, and $126.52 using a 5y exit.

According to DavidWSC, this valuation leans heavily on rapid revenue expansion, stable margins and a future earnings multiple that implies continued AI demand strength. This raises the question of which assumptions matter most and how they interact over time.

Result: Fair Value of $74.53 (UNDERVALUED)

However, this hinges on management hitting aggressive revenue targets, while legal and accounting reviews, including the Hindenburg allegations and restated filings, could still reshape investor confidence.

Another View: Cash Flows Paint A Tighter Picture

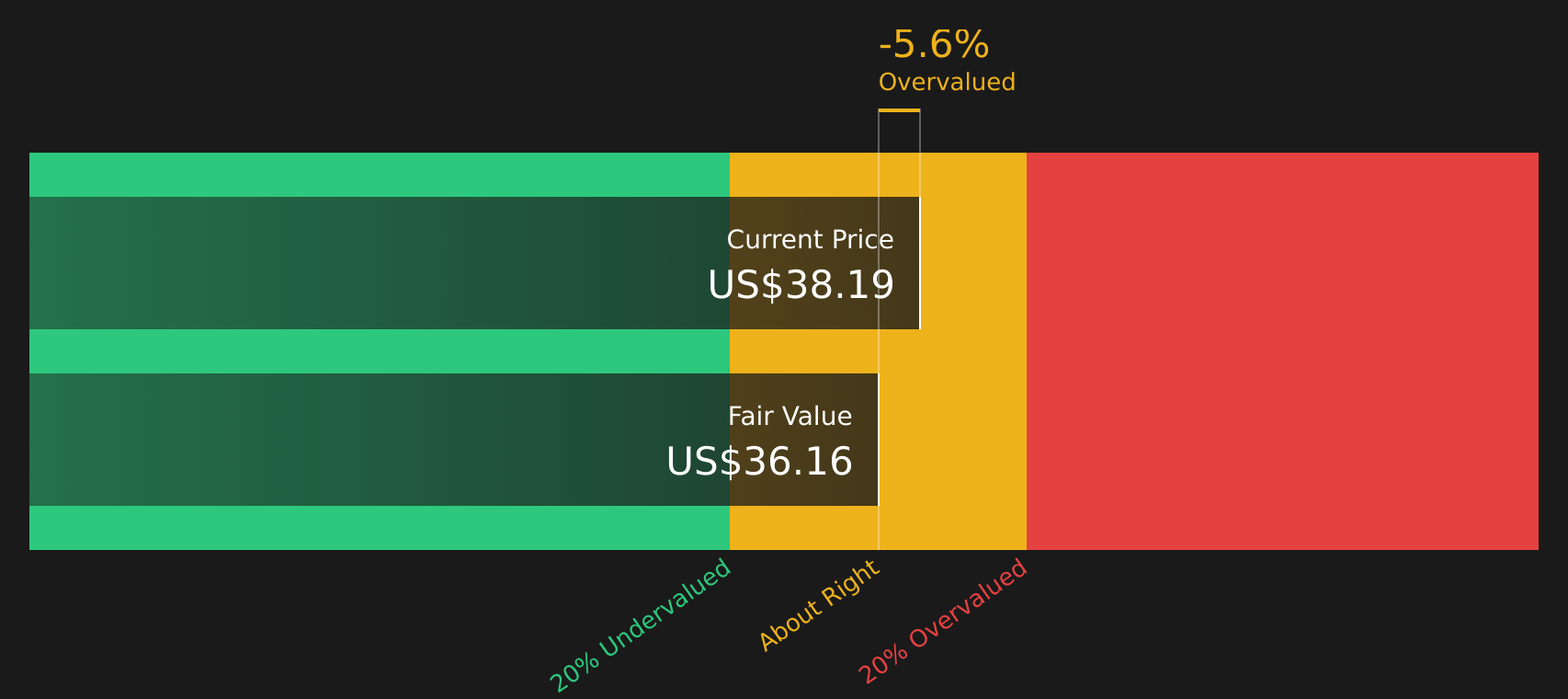

While the community narrative points to a fair value of $74.53 and labels SMCI as undervalued, the SWS DCF model is more cautious, with a future cash flow value of $26.34 against the current $33.62 share price. That implies the stock is overvalued from this perspective, so which story matters more to you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Super Micro Computer for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals on value and future potential, it makes sense to look at the underlying data yourself and move quickly to shape your own view. To weigh the upside against the concerns in a structured way, start by checking the 4 key rewards and 4 important warning signs.

Looking for more investment ideas?

If SMCI has sharpened your thinking, do not stop here. Use the screener to hunt for fresh opportunities that could better fit your risk and return goals.

- Target resilient income by reviewing 12 dividend fortresses that aim to combine substantial yields with staying power through different market conditions.

- Track potential upside by scanning screener containing 23 high quality undiscovered gems that the broader market may not be focused on yet.

- Reduce portfolio stress by filtering for 71 resilient stocks with low risk scores that score well on stability and downside protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.