Assessing Swarmer (SWMR) Valuation After Meta Bureau Contract And Global Expansion Moves

Swarmer, Inc. SWMR | 0.00 |

Swarmer (SWMR) has quickly moved into focus after securing a software license contract with Meta Bureau LLC for more than 16,000 SkyKnight and other UAVs, potentially worth up to US$13.2 million.

The Meta Bureau contract, Japan expansion and new interceptor partnerships have arrived after a volatile few weeks. The 7 day share price return is 9.21%, following a 30 day share price decline of 27.64%, leaving the year to date share price return down 4.39% at US$29.64. Recent momentum has therefore picked up from a weaker short term patch.

If this contract has you thinking more broadly about defense and autonomy, it can be useful to see what else is moving in related areas through 30 robotics and automation stocks

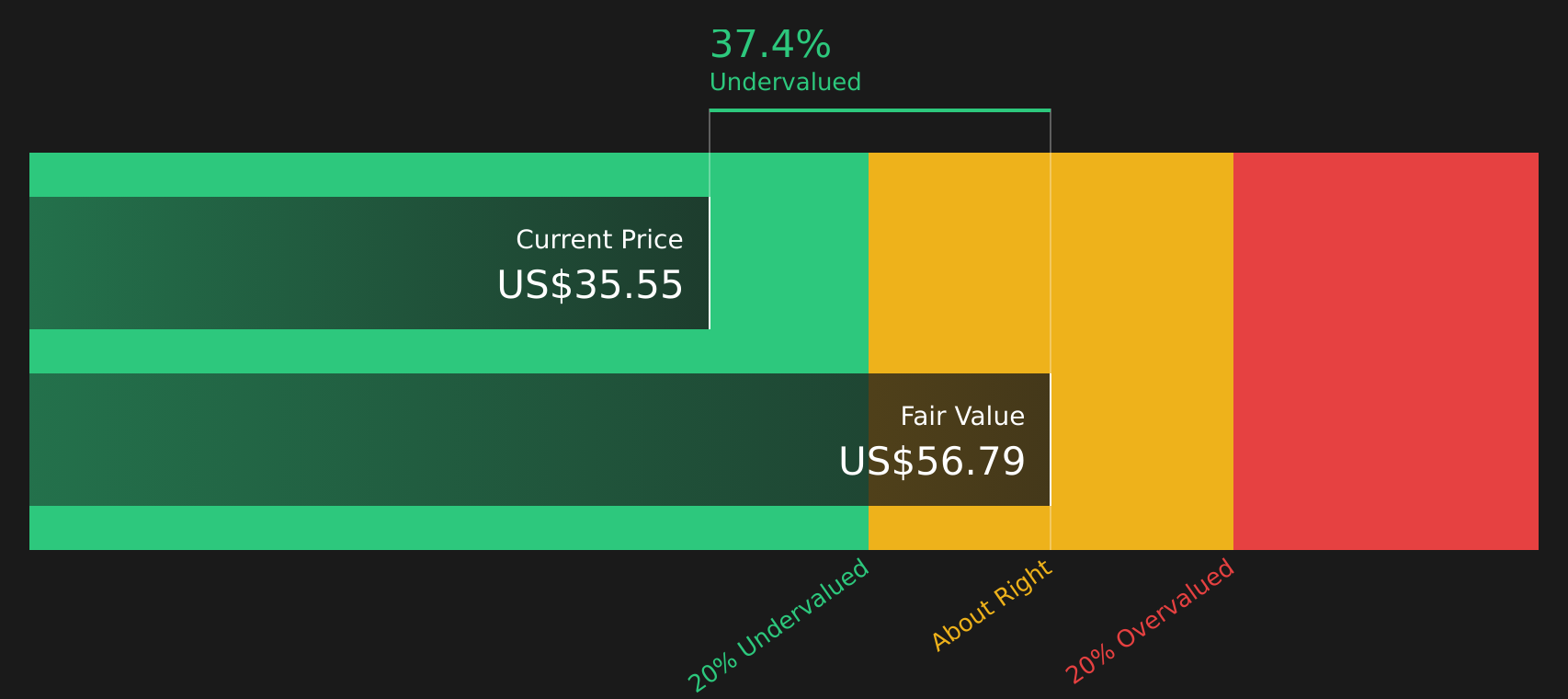

With Swarmer trading at US$29.64, alongside an intrinsic discount flag of about 48% and a price target of US$60.00, the key question is whether recent contracts and expansion are already reflected in the stock or if the market is still underestimating future growth.

Preferred Price-to-Book of 13.9x: Is it justified?

Swarmer is trading at $29.64 and flagged as 47.9% below the SWS DCF estimate of fair value, yet its P/B ratio of 13.9x screens as expensive against peers.

The P/B ratio compares the market value of the company to its book value, which can help you see how much investors are paying relative to net assets. For Swarmer, the statements flag the stock as expensive on this metric compared to both a peer set average of 12.5x and the wider US Aerospace & Defense industry at 3.9x, even though the SWS DCF model suggests the price is below an estimate of future cash flow value of $56.85.

That contrast, a premium P/B multiple alongside a large DCF discount and an unprofitable profile with a reported loss of $12.29m on $220K of revenue, points to a market that is already pricing in a lot of balance sheet light, software style potential. Earnings and revenue are forecast to grow quickly, and the company is expected to move into profitability within three years, yet the limited financial history and high volatility flagged in the statements mean investors are working with a short track record.

Compared with peers, a P/B of 13.9x stands above the peer group average of 12.5x and well above the US Aerospace & Defense industry average of 3.9x, which is strong relative pricing for a business that is still very early in its public life. For investors, the tension between a premium P/B multiple and a discounted DCF fair value puts the focus on how quickly the company can scale its software, convert contracts into meaningful revenue and reach the profitability that the forecasts are pointing to.

Result: Price-to-book of 13.9x (OVERVALUED)

However, the company’s short operating history, ongoing losses of US$12.29m, and a rich 13.9x P/B mean that contract execution risk could quickly challenge the current narrative.

Another View: DCF Versus Rich P/B

The P/B of 13.9x makes Swarmer look expensive against peers, yet the SWS DCF model points the other way, flagging the stock at $29.64 as 47.9% below an estimate of future cash flow value of $56.85. Which signal should carry more weight for you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Swarmer for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between opportunity and risk, it makes sense to move quickly, test the numbers yourself, and decide where you stand using the 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Swarmer has sharpened your thinking, do not stop here. Broadening your watchlist with fresh ideas can help you spot opportunities others overlook.

- Target potential mispricings by checking out 49 high quality undervalued stocks that combine quality fundamentals with appealing valuations.

- Strengthen your income focus by reviewing 12 dividend fortresses that aim to pair higher yields with resilient business models.

- Prioritise resilience by scanning 66 resilient stocks with low risk scores that score well on financial stability and risk checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.