Assessing Walmart (WMT) Valuation After Recent Pullback And Conflicting Fair Value Estimates

Walmart Inc. WMT | 0.00 |

Recent Stock Performance Snapshot

Walmart (WMT) has drawn investor attention after a mixed stretch in its recent returns, with the stock up over the past year but down over the past month and over the past three months.

For context, Walmart’s recent pullback, with a 30 day share price return of down 8.61% and 90 day share price return of down 3.97%, contrasts with a stronger backdrop that includes a 1 year total shareholder return of 22.98% and a 3 year total shareholder return of about 14x. This suggests longer term momentum while short term sentiment has cooled.

If you are comparing Walmart’s profile with other opportunities, it could be timely to scan for companies riding similar themes using the 21 top founder-led companies

With Walmart trading at $118.88 and sitting at about a 16% discount to analyst price targets, investors have to decide: Is this a genuine value opportunity, or is the market already factoring in future growth?

Most Popular Narrative: 8.6% Undervalued

Markus values Walmart at $130 per share, which sits above the latest close at $118.88, setting up a story of modest undervaluation built on real world retail reach and digital growth.

Innovative company, targeting multiple consumer levels. Lots of stores throughout the country where customers can see and "feel" the goods. Try the clothes before buying them etc. This gives a great advantage over pure online shops. Apart from this, Walmart is also very active in the online business and invests in rolling out drone based fast delivery, eg for groceries. So, if you lack this one ingredient to your recipe, you may order it online and receive it right at your doorstep in no time. In this field, Walmart will however be subject to increasing competition from online retailers such as Amazon. As Walmart maintains a lot of physical stores, they can cover more particular situations than Amazon.

Curious what kind of revenue growth, margins and future earnings multiple sit behind that $130 fair value and 8.6% discount, according to markus. The key assumptions link Walmart's subscription flywheel, ecommerce push and traditional store footprint into one valuation story that is not obvious from the share price alone.

Result: Fair Value of $130 (UNDERVALUED)

However, subscription growth could slow, or online rivals could pull price sensitive shoppers away, which would challenge the optimism baked into this narrative.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

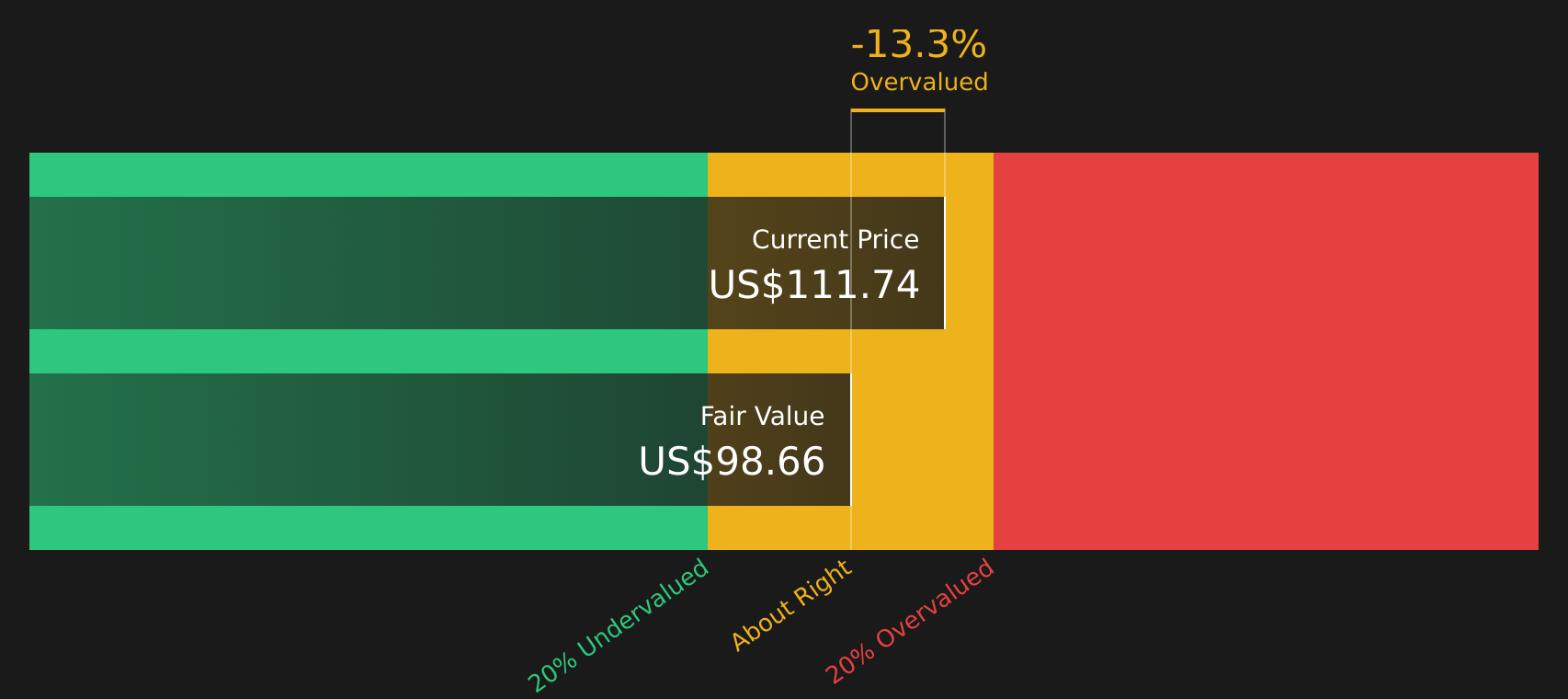

Another View: Cash Flows Paint a Different Picture

While markus sees Walmart as 8.6% undervalued at a fair value of $130 per share, the Simply Wall St DCF model points the other way. On that cash flow view, Walmart's current price of $118.88 sits above an estimated value of $92.86, which frames the stock as overvalued rather than cheap. For you as an investor, the key question is which story you trust more, earnings power or long term cash flows.

Before leaning on one method, it can help to understand how our DCF model treats growth, margins and reinvestment assumptions over time, and how sensitive the result is to small changes.Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Walmart for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment mixed across valuations and recent returns, this is the moment to look through the key data yourself and decide where you stand, starting with the 2 key rewards and 2 important warning signs.

Ready to find your next idea?

If Walmart is on your radar, do not stop there. Use curated screeners to quickly spot other stocks that match the kind of profile you care about most.

- Focus on resilience by scanning 64 resilient stocks with low risk scores that aim to keep portfolio swings in check while still offering meaningful exposure to equities.

- Target quality at a discount by reviewing the 49 high quality undervalued stocks that combine solid fundamentals with prices that sit below many investors' expectations.

- Spot earlier stage opportunities by checking the 24 elite penny stocks with strong financials where stronger balance sheets and healthier financials separate potential standouts from the crowd.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.