Assessing Western Midstream Partners (WES) Valuation As Long Term Returns Contrast With Recent Pullback

Western Midstream WES | 0.00 |

Why Western Midstream Partners (WES) is on investors’ radar today

Western Midstream Partners (WES) has drawn attention after recent trading, with the unit price around $43.62 and a market value near $17.0b prompting investors to reassess how its current metrics line up.

The partnership reports revenue of about $4.05b and net income of roughly $1.20b from its U.S. midstream operations across Texas, New Mexico, and the Rocky Mountains, placing all its business exposure in domestic energy infrastructure.

At around $43.62, Western Midstream Partners’ recent 1-day share price return of 0.88% comes after a 7-day decline of 3.92%. Its year-to-date share price return of 9.82% and 1-year total shareholder return of 25.48% point to momentum that has cooled in the near term but remains strong over longer horizons, supported by very large 3-year and 5-year total shareholder returns.

If you are comparing WES with other income and infrastructure ideas, it can also be helpful to see what is happening across listed grids and transmission, including 33 power grid technology and infrastructure stocks

With Western Midstream Partners trading close to a recent analyst price target and showing a wide gap to one intrinsic value estimate, the key question is whether units are still on sale or if the market already reflects expected future growth.

Price-to-Earnings of 14.4x: Is it justified?

Western Midstream Partners trades on a P/E of 14.4x, which screens as good value against its peer group but slightly expensive compared with the broader US oil and gas industry.

The P/E ratio links the current unit price to earnings per unit and is a quick way to see how much investors are paying for current profit. For a mature midstream business with established assets, this metric often reflects what the market is willing to pay for steady cash generation and distributions.

Here, the stock sits below the peer average P/E of 22.4x, suggesting investors are paying less for each dollar of earnings than for similar companies. At the same time, the ratio is above the wider US oil and gas industry average of 13.1x, which indicates the market is placing a premium on Western Midstream Partners compared to more general sector exposure. Against an estimated fair P/E of 21.6x, the current 14.4x level is materially lower. Some investors may see this gap as room for sentiment to shift closer to that fair ratio over time if forecasts play out as expected.

Result: Price-to-Earnings of 14.4x (UNDERVALUED)

However, investors still need to watch for weaker energy pricing or lower throughput volumes, which could pressure earnings and challenge the current P/E discount argument.

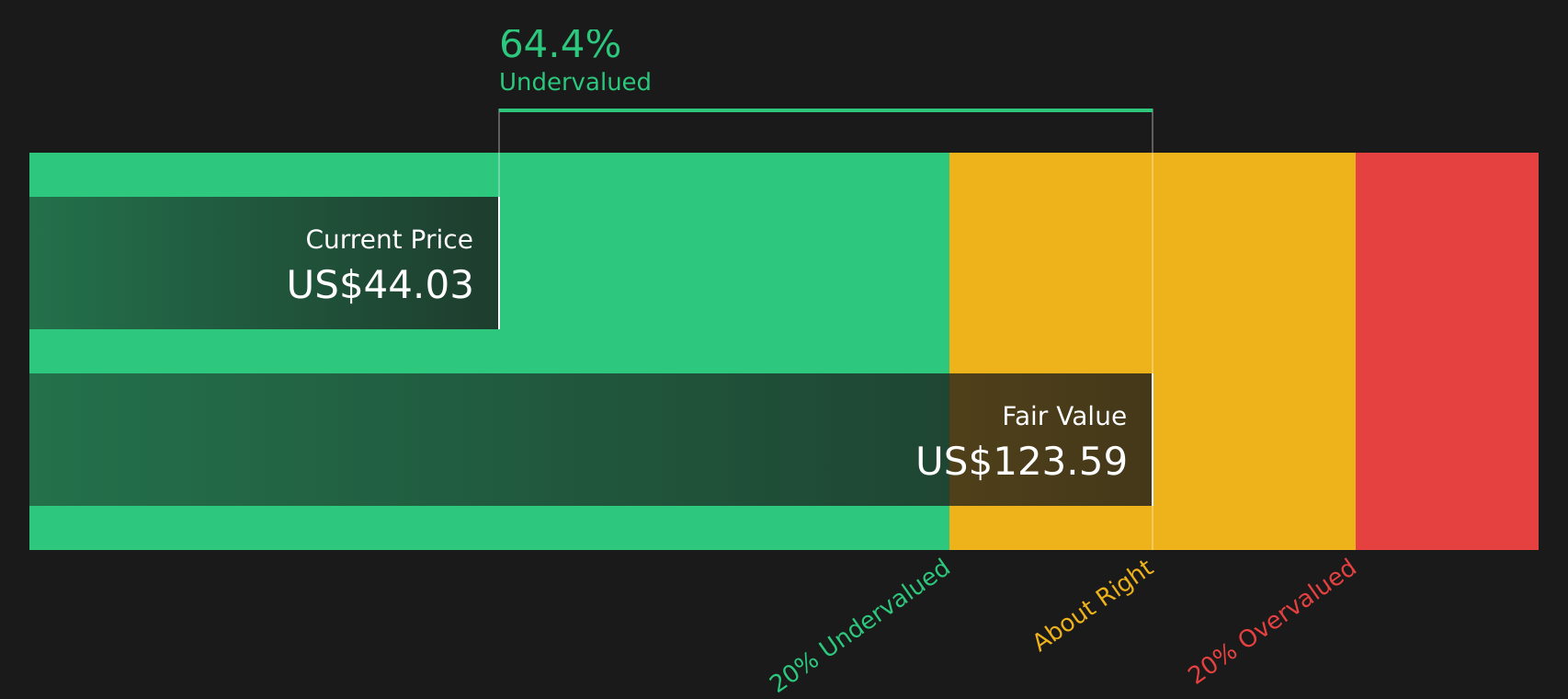

Another view on value

While the P/E discussion points to Western Midstream Partners looking inexpensive against peers, the SWS DCF model presents an even starker picture. It shows an estimated future cash flow value of $123.70 versus the recent $43.62 price, suggesting the units appear heavily undervalued using this method.

That is a sizable difference for any investor to consider, so the key question is whether the cash flow assumptions behind that figure seem realistic enough for you to rely on, or whether the simpler earnings multiple provides a more reliable indication.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Western Midstream Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment in this review pulling in both positive and cautious directions, it makes sense to look at the details yourself and decide how compelling the balance of risks and rewards really feels for your portfolio, starting with the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop at just one stock, you risk missing other opportunities that might fit your goals even better, so broaden your search with a few targeted screens.

- Spot potential value opportunities early by scanning 47 high quality undervalued stocks that pair attractive pricing with solid fundamentals.

- Strengthen the quality tilt in your portfolio by focusing on companies from the solid balance sheet and fundamentals stocks screener (47 results).

- Get ahead of the crowd by reviewing the screener containing 22 high quality undiscovered gems before they are widely talked about.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.