Assessing Whether Northrop Grumman (NOC) Is Fairly Valued After Strong Multi Year Shareholder Returns

Northrop Grumman Corp. NOC | 678.59 | -0.23% |

Why Northrop Grumman stock is on investors’ radar

Northrop Grumman (NOC) has drawn attention recently as investors weigh its current valuation against its track record of revenue and net income growth, along with strong multi year total returns.

At a share price of US$724.38, Northrop Grumman has recently seen a 1 day share price return of 1.9% and a 30 day share price return of 4.6%. Its 1 year total shareholder return of 55.5% and 5 year total shareholder return of 157.0% point to strong longer term momentum that investors are now weighing against its current valuation.

If this move in defense names has your attention, it could be a good moment to see what else is on the radar with our screener of 84 nuclear energy infrastructure stocks.

With revenue at US$41.95b, net income of US$4.18b and the share price sitting almost exactly in line with analyst targets, the real question is whether Northrop Grumman is undervalued today or already pricing in future growth.

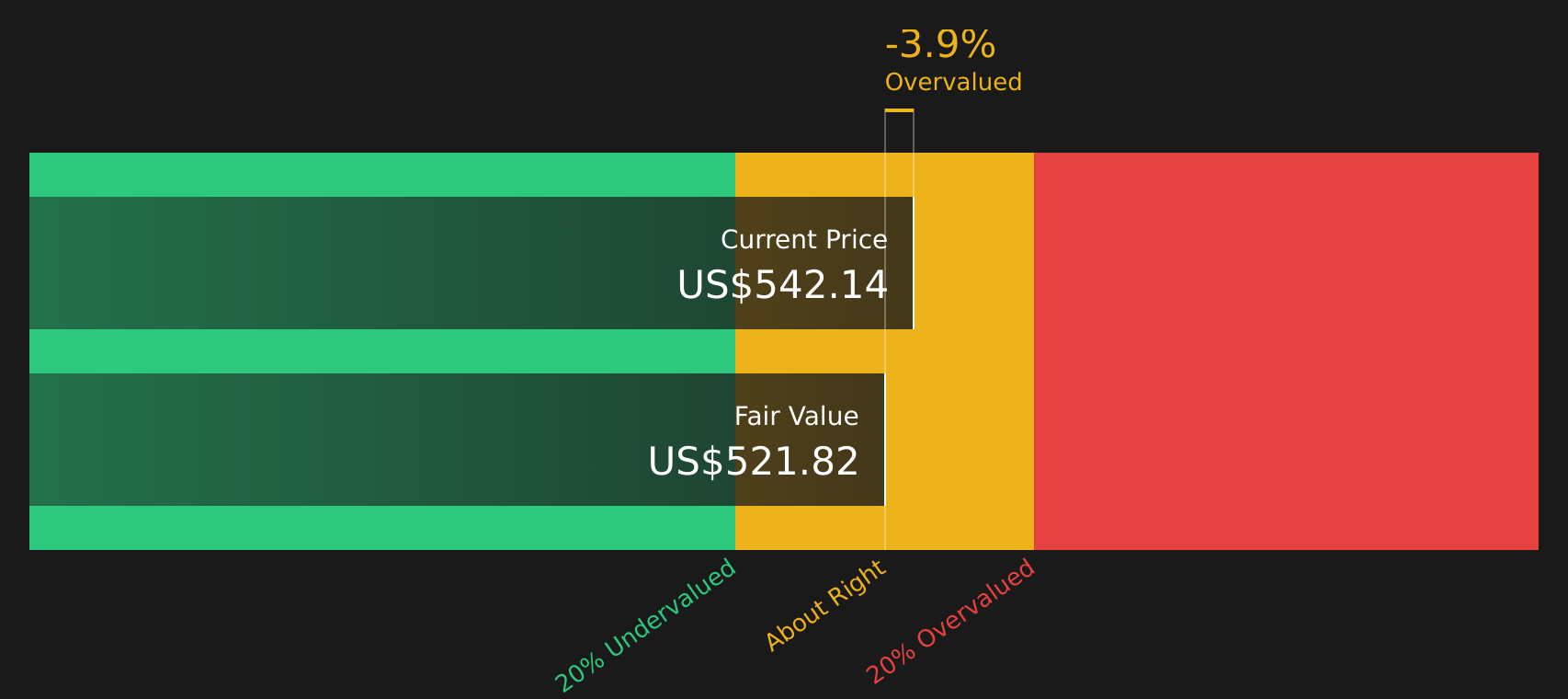

Most Popular Narrative: Fairly Valued

With Northrop Grumman trading at US$724.38 against a narrative fair value of US$724.39, the widely followed view is that the current price closely reflects its modeled cash flows using a 7.82% discount rate.

Supportive government actions to remove regulatory and contractual barriers are leading to faster program execution and improved incentives, which, coupled with targeted capital investments and a strong backlog, are expected to improve earnings stability, free cash flow, and long-term profitability.

Want to see what sits behind that fair value call? The narrative leans heavily on steady growth, firm margins, and a future earnings multiple that is anything but casual.

Result: Fair Value of $724.39 (ABOUT RIGHT)

However, that fair value story can change quickly if major U.S. defense programs face budget cuts or if sanctions and policy shifts begin to limit international opportunities.

Another View: Cash Flows Paint A Tougher Picture

There is a catch. While narrative fair value sits almost exactly at the current US$724.38 share price, our DCF model puts Northrop Grumman at US$529.15, which suggests the shares are pricing in richer cash flows than the model supports. So which story do you trust more: earnings or cash?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Northrop Grumman for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The split between the fair value view and the tougher cash flow take is clear, so it makes sense to look at the numbers yourself instead of waiting on the crowd. To frame your own stance quickly, it helps to see both sides of the story in one place with 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If this kind of valuation split has you thinking harder about where to put fresh capital, do not stop with just one defense stock on your watchlist.

- Target income first with a list of 13 dividend fortresses that could help you focus on companies prioritizing regular cash returns to shareholders.

- Hunt for potential mispricings using our 49 high quality undervalued stocks to quickly spot businesses that our filters flag as trading below their assessed worth.

- Prioritise durability by scanning 76 resilient stocks with low risk scores so you can focus on companies that score well on balance sheet strength and overall risk checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.