Baidu (BIDU) Wins Swiss Robotaxi Trial Approval, Is The AI Upside Already Priced In?

Baidu, Inc. Sponsored ADR Class A BIDU | 0.00 |

Baidu (BIDU) is back in focus after its Apollo Go unit and Swiss Post’s PostBus received approval for Level 4 autonomous driving trials in Switzerland, marking the company’s first self driving tests in Europe.

The autonomous driving approval lands at a time when Baidu’s share price has been under pressure, with a 30 day share price return of down 23% and a year to date share price return of down 31%, even as the 1 year total shareholder return is 21%. This highlights recent volatility against a stronger 12 month picture.

If Baidu’s move into European self driving trials has caught your attention, it could be worth scanning for other AI related opportunities through the 33 AI small caps

With Baidu trading at US$104.22, sitting on a 31% decline year to date but a 21% total return over 12 months and valuation models pointing to mixed signals, you have to ask: is this a reset buying opportunity, or is the market already pricing in its AI and autonomous driving ambitions?

Most Popular Narrative: 40.9% Undervalued

With Baidu’s fair value estimate at $176.41 against a last close of $104.22, the most followed narrative sees a wide gap the market has not closed yet.

The commercialization and global expansion of Apollo Go (autonomous driving) through capital-efficient, asset-light partnerships with Uber, Lyft, and major international markets introduces high-margin, recurring revenue streams, successful execution could diversify income, support higher net margins, and unlock significant long-term profit growth.

Curious how a company with compressed recent margins, ambitious AI bets and a premium future earnings multiple still lands on that fair value number? The underlying narrative leans heavily on faster earnings growth than revenue, a sharp margin reset and a richer valuation multiple than the broader industry. The tension between cautious near term profitability and those long term assumptions is where the real story sits.

Result: Fair Value of $176.41 (UNDERVALUED)

However, there are clear pressure points, including declines in Baidu’s core online marketing revenue and negative free cash flow, as AI and cloud investment weighs on margins.

Another View: SWS DCF Model Puts Baidu Closer to Fairly Priced

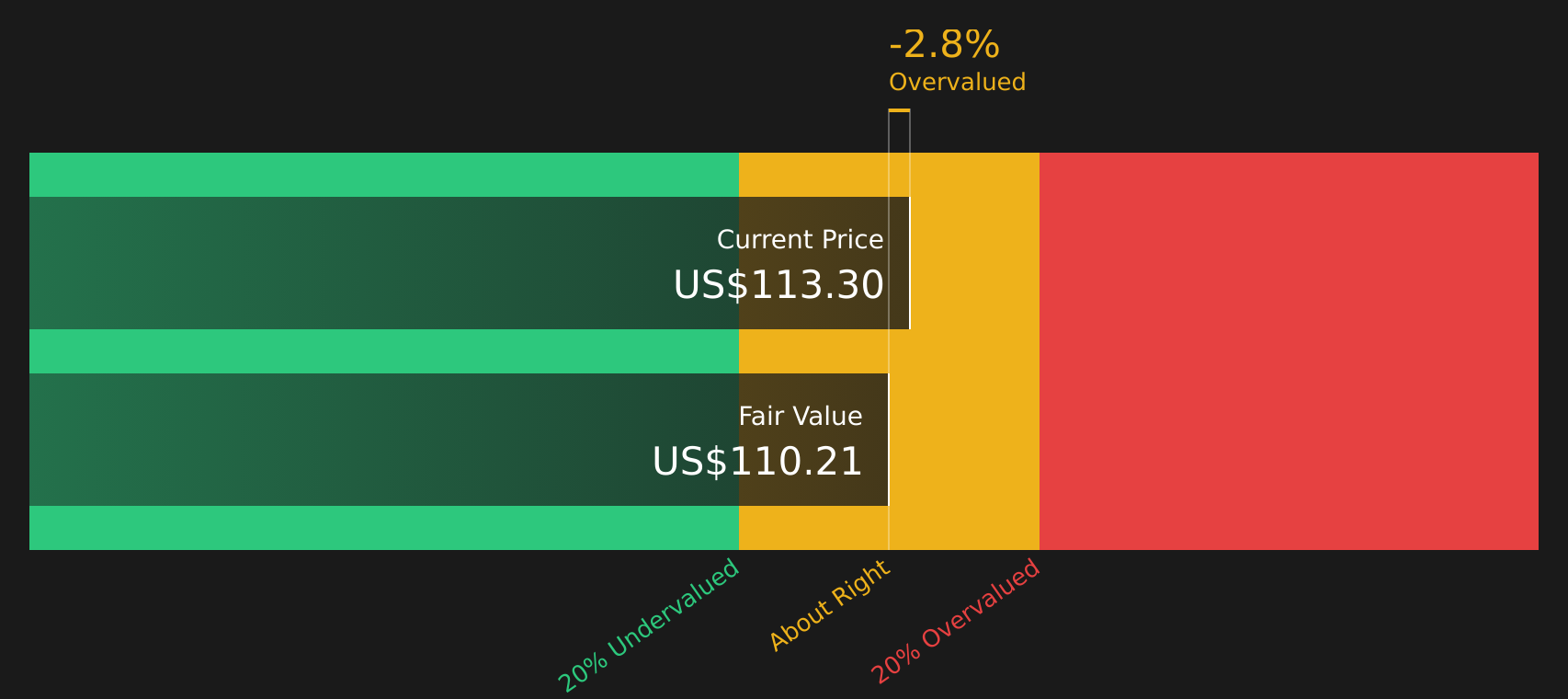

The analyst narrative leans on a fair value of $176.41 for Baidu, but the SWS DCF model tells a tighter story, with an estimate of $102.81 versus the current $104.22. That small premium suggests less obvious upside and raises a simple question: how much of the AI story is already in the price?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Baidu for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Baidu so divided, are you comfortable with the balance of risk and reward here, or do you want to stress test it yourself by checking the 1 key reward and 2 important warning signs?

Looking for more Baidu sized investment ideas?

If Baidu’s story has you thinking more broadly about where to put fresh capital, do not stop at one stock. Instead, widen your net with targeted screens.

- Zero in on potential mispriced opportunities by scanning the 44 high quality undervalued stocks that pair solid fundamentals with attractive entry points.

- Lock in the potential for income-focused returns by reviewing the 8 dividend fortresses that concentrate on higher yielding, sturdier payers.

- Protect your downside by reviewing the 71 resilient stocks with low risk scores designed to surface companies with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.