Boeing (BA) Stock Looks Below Fair Value Despite Cash Flow Risks

Boeing Company BA | 0.00 |

Boeing stock sits in an unusual valuation spot right now, with the Discounted Cash Flow (DCF) estimate pointing to sizeable upside relative to the current price, while market multiples lean the other way and recent five year returns have been slightly negative.

- Over the past 5 years, Boeing has declined about 5.7%, which suggests the share price has not kept pace with the company’s shifting business mix and investor expectations.

- New long term defense and space work, such as the MUOS satellite contract, can support future cash flow, but ongoing concerns around cash burn and capital needs may still weigh on how much investors are prepared to pay today.

- On Simply Wall St's broader checks, Boeing scores 3 out of 6 for value, which points to a mixed picture rather than a clear bargain or clear overvaluation.

For investors, the key question is whether Boeing’s current price already reflects the risks in its cash flows, or whether the intrinsic value implied by the DCF still leaves a meaningful margin of safety.

Does Boeing Look Undervalued on Cash Flow?

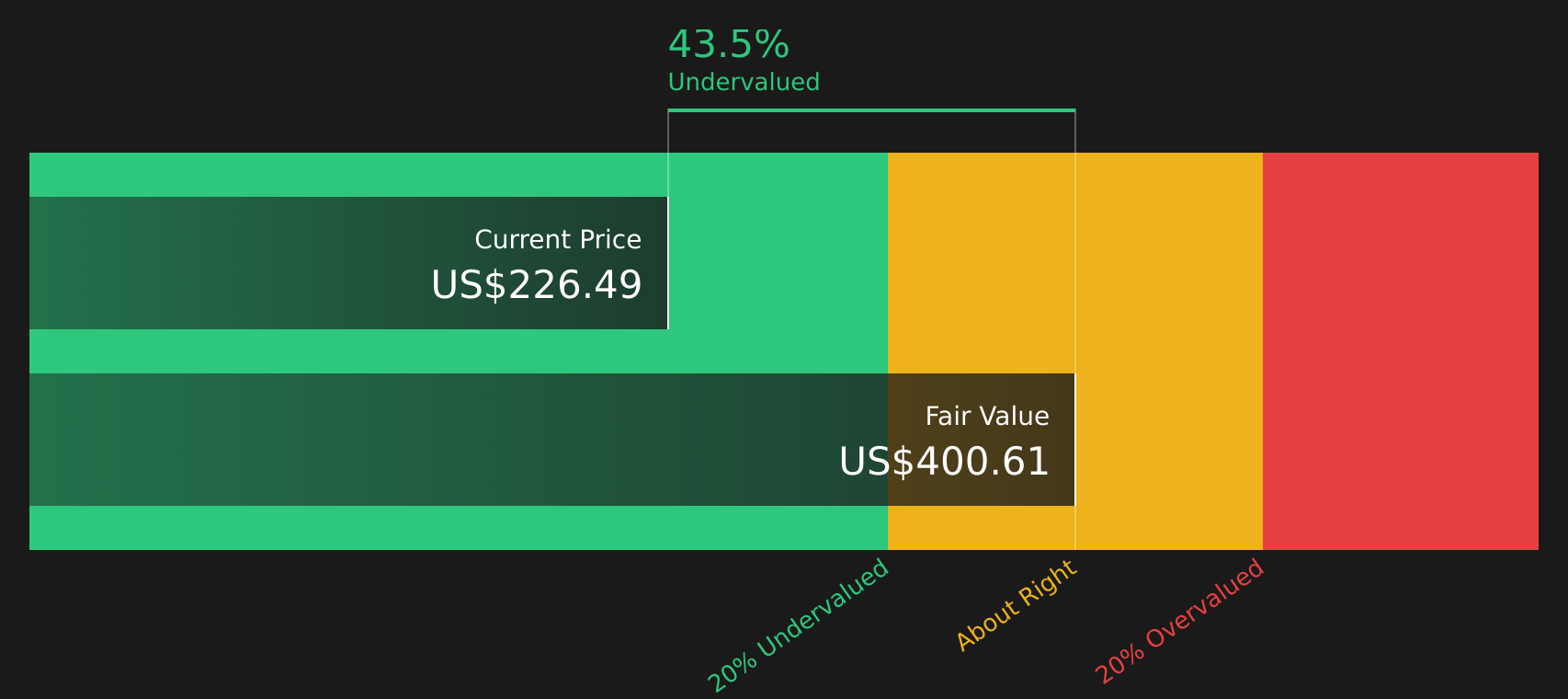

The Discounted Cash Flow (DCF) model estimates what Boeing’s future cash generation could be worth today. On the latest twelve month numbers, Boeing is still reporting free cash flow outflows of about $477m, so the model leans heavily on an assumption that cash flow recovers rather than staying at current levels.

On that basis, the DCF points to an intrinsic value around $399 per share, which implies the stock trades at roughly a 45.3% discount to this estimate. The discount sits alongside a high current P/E of 89.6, which indicates that earnings are still thin relative to the share price even if cash flow eventually improves.

The recent $2b MUOS satellite contract adds further long dated defense cash flow potential, and the market’s caution around Boeing’s cash burn helps explain why the price remains well below the DCF estimate.

Overall, the DCF workup suggests Boeing stock currently screens as undervalued relative to its projected cash flows.

Our Discounted Cash Flow (DCF) analysis suggests Boeing is undervalued by 45.3%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Has Boeing Run Too Far on Earnings?

The P/E multiple is a useful cross check for Boeing because it links the share price directly to the earnings that ultimately need to support it. Boeing currently trades on a P/E of about 89.6x, which is more than double the Aerospace & Defense industry average of 39.3x and well above the broader peer average of 36.2x.

On Simply Wall St's fair ratio framework, which adjusts for Boeing's size, risk and profitability profile, a P/E closer to 67.2x would be more in line with its fundamentals. The current 89.6x therefore represents a sizeable premium to that tailored benchmark, which indicates that investors are paying a high price for each dollar of earnings even after allowing for sector specific factors.

Taken together, Boeing stock currently appears overvalued based on its P/E multiple.

The Boeing Narrative: What Would Justify Today's Price?

For Boeing, Simply Wall St Narratives are the link between this mixed valuation picture and the specific expectations that would need to play out for the stock to be worth materially more or less than today's price, and they sit on Simply Wall St's Community page. Rather than focusing on a single multiple or model output, each narrative lays out the assumptions behind its view of fair value so you can compare them with Boeing's actual results as they are reported.

One of the top community narratives on Boeing: 27% undervalued

"Continued expansion of Boeing's high margin services and aftermarket platform, supported by new distribution centers and integrated digital offerings, is creating a durable stream of recurring, profitable revenue…"

Do you think there's more to the story for Boeing? Head over to our Community to see what others are saying!

The Bottom Line

For Boeing, the Discounted Cash Flow (DCF) work suggests meaningful upside to intrinsic value, while the P/E view flags the stock as overvalued on current earnings. That split mainly comes down to timing and reliability of future cash flows versus today’s profitability and sentiment toward the sector. Broader valuation checks sit in the middle. The real swing factor is whether Boeing can turn its cash burn and capital needs into stable, growing free cash flow. The key question for you is whether the current discount to intrinsic value compensates sufficiently for those execution and funding risks or whether it reflects them appropriately.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.