Boeing (BA) Stock May Be Below Fair Value On MAX 7 Certification

Boeing Company BA | 0.00 |

Boeing stock has slipped about 7.2% over the past year, yet the valuation signals are split, with a Discounted Cash Flow (DCF) estimate pointing to meaningful upside while market multiples suggest the shares are not cheap.

- Boeing's share price is down 7.2% over the past year, which puts more focus on whether the current level already reflects its operational and regulatory challenges.

- Progress on 737 MAX certifications and production ramp ups can support future cash flow expectations, while ongoing manufacturing issues and IT disruptions highlight execution risk that may weigh on how much investors are willing to pay.

- Boeing scores 3 out of 6 on valuation checks, a mixed picture rather than a clear bargain or clear overvaluation.

The issue now is whether Boeing's current price more closely reflects the upside suggested by the intrinsic value estimate or the caution implied by richer earnings based multiples.

Is Boeing Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) method values Boeing by projecting future cash the company might generate for shareholders and discounting it back to today.

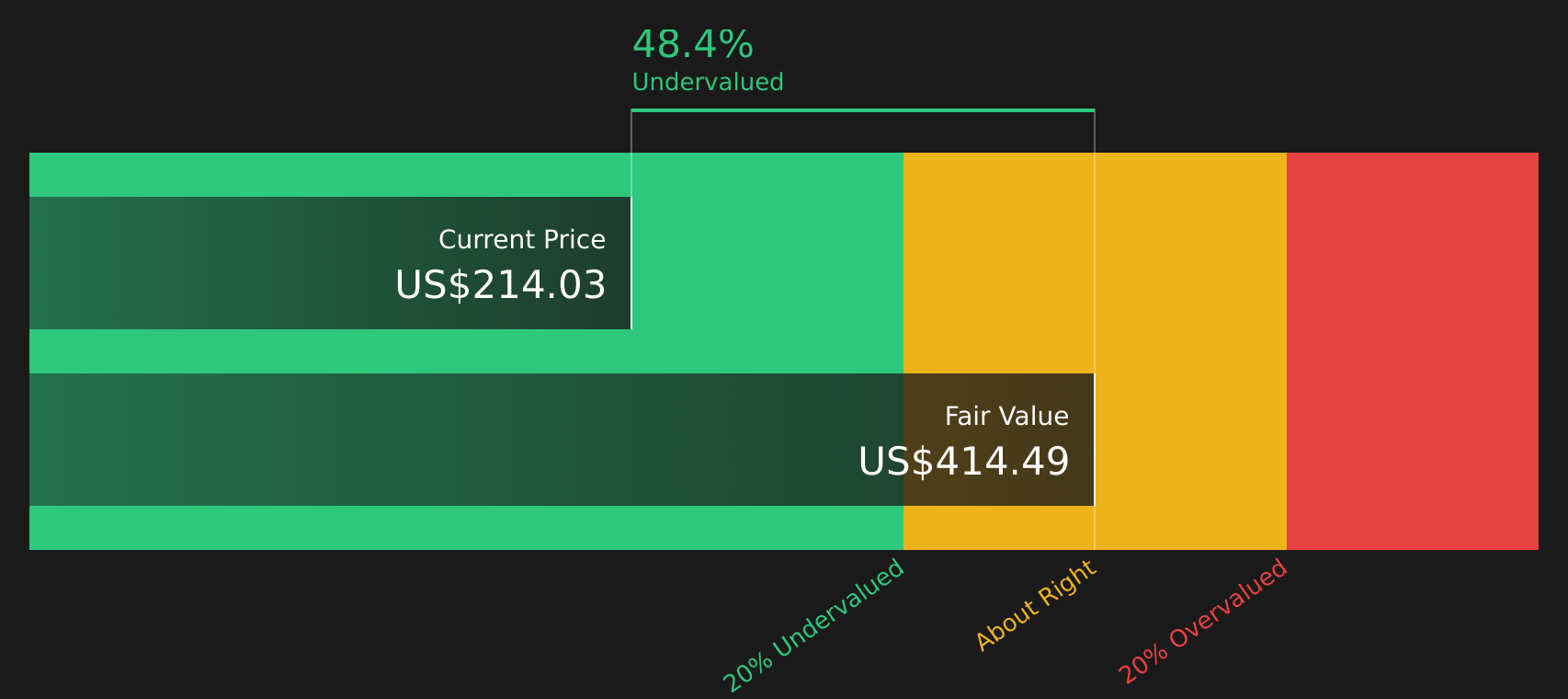

On this model, Boeing is currently coming off a period of pressure, with latest twelve month free cash flow showing a loss of about $0.48b. The DCF assumes those cash flows recover over time rather than stay at that level, which leads to an estimated intrinsic value of about $411.84 per share. Compared with the current share price, that implies the stock trades at roughly a 48.0% discount to this intrinsic value estimate.

The planned ramp up in 737 MAX production and progress on certifications helps explain why the cash flow projections in the DCF look healthier than the recent numbers, even though operational setbacks and IT outages remain in focus. Despite these cross currents, the model suggests the market price is still below the level implied by the projected cash flows.

On this Discounted Cash Flow view, Boeing stock currently appears undervalued.

Our Discounted Cash Flow (DCF) analysis suggests Boeing is undervalued by 48.0%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Does Boeing Look Pricey on Earnings?

The P/E ratio is a common way to see how much you are paying for each dollar of Boeing's earnings. Right now, Boeing trades on a P/E of about 87.9x, which is well above the Aerospace & Defense industry average of roughly 37.9x and above a peer group average of about 36.5x.

A tailored fair P/E for Boeing, which accounts for its size, margins and risk profile, sits closer to 67.0x. The current multiple is therefore higher than both this fair ratio and the sector benchmarks, indicating that investors are already paying a premium price for the stock relative to its earnings base.

On this P/E multiple, Boeing stock appears expensive compared with both its industry and what the fair ratio implies.

The Boeing Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Boeing pick up where this valuation split leaves off and spell out which paths for Boeing's growth, margins and earnings would need to play out for the stock to be worth materially more or less than today. They are available on the company’s Community page. Each one treats its fair value as a thesis about Boeing's business that can be revisited over time, rather than a one off snapshot.

One of the top community narratives on Boeing: 29% undervalued

"Boeing's vast $522 billion commercial backlog, with 5,900 aircraft sold firm into the next decade, positions the company to disproportionately benefit from the expected doubling of global air travel demand by 2040…"

Do you think there's more to the story for Boeing? Head over to our Community to see what others are saying!

The Bottom Line

For Boeing, the Discounted Cash Flow (DCF) intrinsic value points to a large upside gap, while the earnings multiple signals the stock is already priced at a premium. That split mainly reflects a tension between what long term cash flows could look like once production and deliveries stabilise, and what investors are currently willing to pay based on reported earnings and sector comparisons. Broader valuation checks sit in the middle, so neither side of the argument is overwhelming. The key question from here is whether Boeing can convert its order book and efficiency plans into sustained cash generation without further execution setbacks that keep the multiple elevated and trust subdued.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.