Celsius (CELH) Stock Looks Cheap On Returns But Expensive On Earnings

Celsius Holdings, Inc. CELH | 0.00 |

Celsius Holdings stock is in a tricky spot for valuation right now, with the share price weak over recent years while broader checks still suggest the stock is not a clear bargain. Recent legal and regulatory scrutiny around its Alani Nu energy drinks has added another layer of uncertainty on top of already cautious market sentiment.

- Over the past 3 years, Celsius Holdings has delivered a total return that is down about 41%, which shows how much optimism has already come out of the share price.

- On the one hand, investors see growth potential in the broader portfolio, including Alani Nu. On the other hand, ongoing investigations into marketing practices and product safety may weigh on how much value the market is willing to assign to those prospects.

- With a value score of 2 out of 6, Celsius Holdings currently screens as leaning expensive rather than a clear bargain on the wider set of valuation checks.

The issue now is whether the current price for Celsius Holdings already reflects these legal, operational, and growth risks, or if the stock still embeds expectations that are too optimistic for the fundamentals on offer.

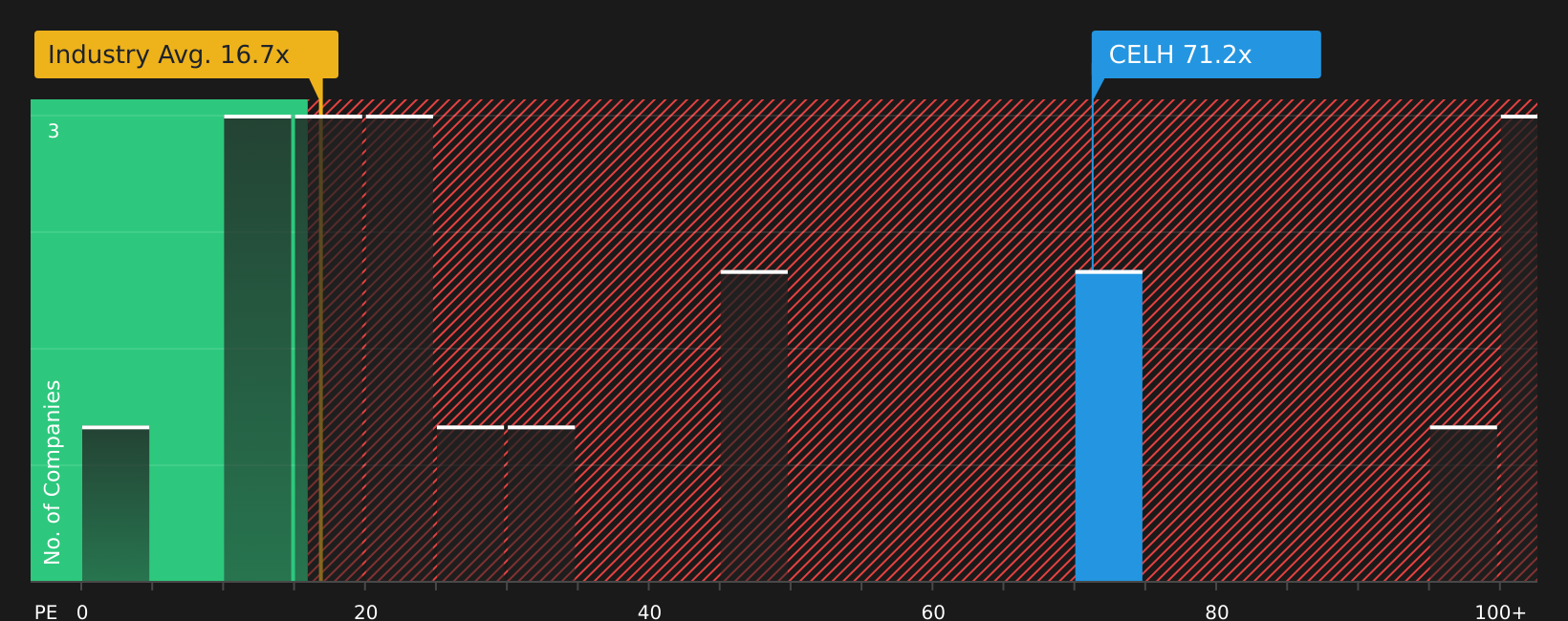

Has Celsius Holdings Run Too Far on Earnings?

The P/E ratio is a useful lens for Celsius Holdings because the stock is already priced primarily on its earnings power rather than dividends. Celsius Holdings currently trades at about 65.4x earnings, compared with an average of 16.8x for the broader Beverage industry and roughly 51.1x for peers, so you are paying a clear premium for each dollar of current profit.

On a more tailored basis, the fair P/E ratio implied by the company’s growth profile, margins, size, and risk is estimated at 28.5x. This is less than half of where Celsius Holdings is currently priced. Despite the recent legal scrutiny around Alani Nu and the share price weakness, the multiple has not fallen to a level that lines up with this fair ratio yardstick.

On this P/E yardstick, Celsius Holdings stock appears overvalued, with the current multiple sitting well above both industry norms and the modelled fair level.

The Celsius Holdings Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Celsius Holdings valuation puzzle leaves off by spelling out which paths for growth, margins, and earnings would need to play out for the stock to be worth materially more or less than today's price on the market. Rather than a single P/E shortcut or one model output, each Narrative lays out its own set of fair value assumptions so you can compare those inputs with Celsius Holdings' actual results as they arrive.

One of the top community narratives on Celsius Holdings: 47% undervalued

"This narrative is about understanding which of those two situations you are looking at right now, as the company enters an entirely new chapter…"

Do you think there's more to the story for Celsius Holdings? Head over to our Community to see what others are saying!

The Bottom Line

For now, Celsius Holdings trades on a premium P/E that points to an overvalued stock on market multiples, even after a weak 3 year return. That gap only really closes if earnings growth, margins, or both ultimately support paying far more for each dollar of profit than the wider beverage peer group. With broader valuation checks already on the soft side, the key question from here is whether Celsius Holdings can deliver the profitability and risk profile that keeps investors comfortable with this premium in the face of ongoing legal and regulatory scrutiny.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.