Charter Communications (CHTR) Stock Looks Cheap On Earnings While Its 5 Year Return Stays Weak

Charter Communications, Inc. Class A CHTR | 0.00 |

Charter Communications stock has been heavily sold off over the past few years, yet the current valuation checks suggest the shares still screen cheap on earnings based metrics. This sets up a clear tension between a weak share price history and a more forgiving market multiple picture.

- Over the past 5 years, Charter Communications has declined about 81%, which leaves the stock trading at levels where valuation is front and center for investors.

- The planned Cox Communications acquisition and heavy network investment can support the long term earnings story, but ongoing broadband subscriber losses and execution risk around large capital spending remain key threats to how the market prices the stock.

- On Simply Wall St's broader checks, Charter Communications looks undervalued in 5 of 6 tests. This indicates that the overall valuation framework leans cheap rather than expensive for the current fundamentals.

For investors, the debate is whether the deeply weak five year share performance already reflects the growth and execution risks, or if the current valuation of Charter Communications still leaves room for further downside repricing.

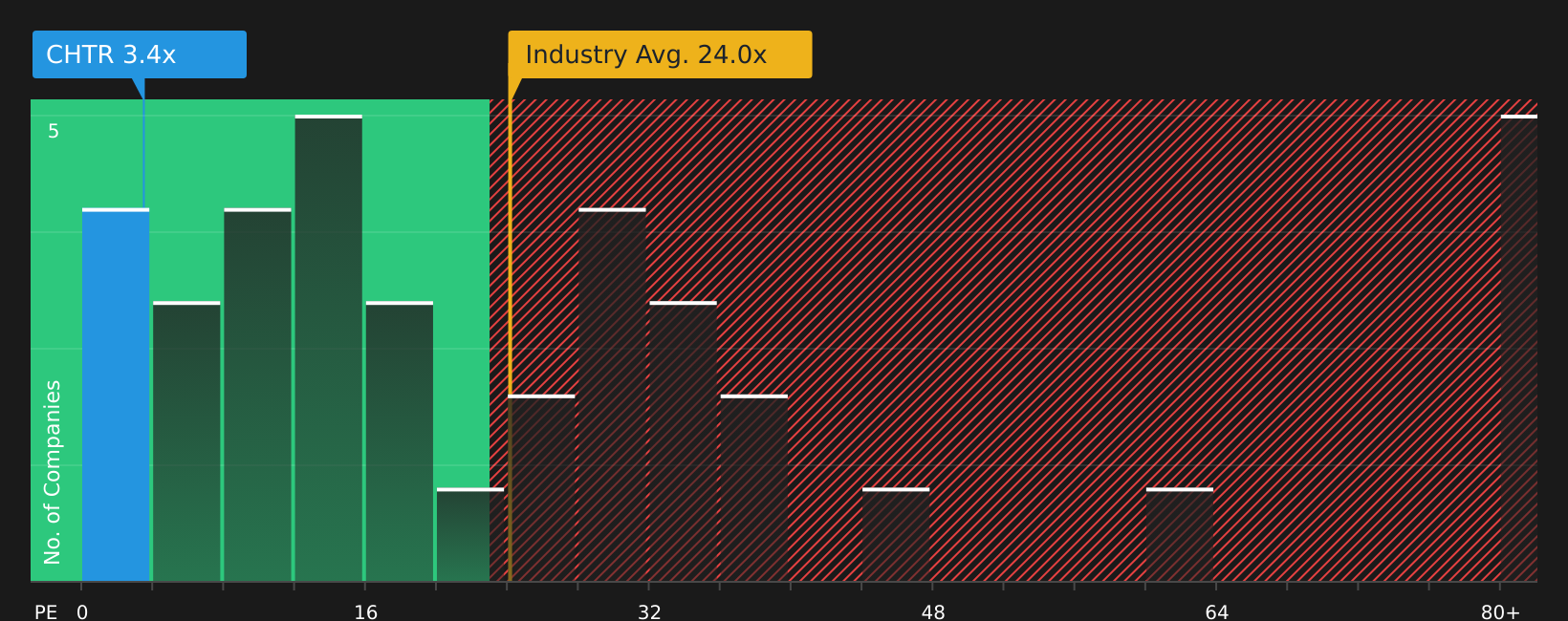

Is Charter Communications Still Cheap on Earnings?

P/E is a useful lens for Charter Communications because earnings remain a core focus for how investors value large, mature telecom and media companies. Charter Communications currently trades on a P/E of about 3.4x, compared with a Media industry average of 24.0x and a broader peer average of 29.2x. On Simply Wall St's fair ratio framework, which adjusts for factors such as growth profile, margins, size and risk, the stock might be expected to trade closer to 18.2x.

Even after recent headlines about broadband subscriber pressure and the planned Cox Communications acquisition, this very large gap between the current 3.4x P/E and both the industry and fair ratio benchmarks points to a market that is pricing in considerable execution and growth risk. If you think Charter Communications can stabilise earnings around current levels while integrating Cox and funding network upgrades, the present earnings multiple suggests the stock appears undervalued on this metric.

On the P/E multiple alone, Charter Communications appears markedly undervalued compared with both its industry and a tailored fair ratio estimate.

The Charter Communications Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Charter Communications valuation puzzle leaves off by spelling out which combinations of future growth, margins and earnings would need to play out for the stock to be worth materially more, or materially less, than today's price. Rather than relying on a single valuation multiple or model, each Narrative sets out its underlying assumptions so you can compare those expectations with Charter Communications' actual results as they are reported on the Community page.

The community is split on Charter Communications, with one camp leaning into a discounted valuation and another focused on pressure from broadband competition and capital needs.

Bull case: 41% undervalued

"Charter's strategic focus on bundling, along with attractive pricing of its Internet, mobile, and video services, is helping to drive higher customer acquisition and retention rates, contributing to future revenue stabilization and growth…"

Bear case: 11% overvalued

"Charter Communications faces persistent broadband subscriber losses amid heightened competition from 5G and fixed wireless access providers, threatening the company's ability to return to meaningful broadband customer growth and putting long-term revenue expansion at risk…"

Do you think there's more to the story for Charter Communications? Head over to our Community to see what others are saying!

The Bottom Line

Charter Communications screens as undervalued on earnings against both industry peers and a tailored fair-ratio check, which is why it still catches the eye despite a very weak five year return profile. That discount reflects real concerns around broadband subscriber pressure, capital intensity and the execution risk tied to the Cox Communications deal and ongoing network investment. For you, the key question is whether Charter Communications can keep earnings resilient enough for that low P/E to look conservative rather than justified by structural pressure. The crux of the debate is whether the current discount signals a value opportunity or a value trap if broadband and capital spending worries persist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.