Citigroup (C) Valuation Check As Capital Reshuffle Adds New Preferred Stock And Retires Series X Shares

Citigroup Inc. C | 131.69 | +1.63% |

Citigroup (C) has moved aggressively on its capital stack, redeeming all $2.3b of Series X preferred depositary shares while introducing new 6.250% Series II preferred stock and issuing fresh senior notes across fixed, floating and zero coupon structures.

These capital moves come as Citigroup’s 90 day share price return of 14.83% contrasts with a 30 day share price decline of 5.52%, while the 1 year total shareholder return of 44.24% points to stronger momentum over a longer horizon.

If Citigroup’s capital reshuffle has you thinking about banks and beyond, it could be a good moment to broaden your search with our list of 22 top founder-led companies.

With Citigroup trading at $115.74 and third party estimates pointing to both an intrinsic value gap and a discount to analyst targets, the key question is whether this is genuine mispricing or if the market is already taking future growth into account.

Most Popular Narrative: 20% Undervalued

Citigroup’s fair value narrative of $116 sits almost on top of the current $115.74 share price, yet it still frames the stock as meaningfully discounted to its future cash flow potential.

Investment and momentum in wealth management, especially in high-growth regions and with affluent clients, is expanding the fee-based revenue stream and improving return on equity, as evidenced by double-digit growth in revenues, net new assets, and margins in recent quarters.

Curious how a business reshuffle, higher fee income and a richer profit profile can still point to a discount here? The key is how revenue, margins and future earnings are stitched together into that single $116 figure, and what kind of future valuation multiple is baked into the story.

Result: Fair Value of $116 (UNDERVALUED)

However, that fair value story still depends on Citi keeping digital rivals at bay, and on managing ongoing regulatory and restructuring costs that could pressure earnings and capital returns.

Another View: Earnings Multiple Flags Caution

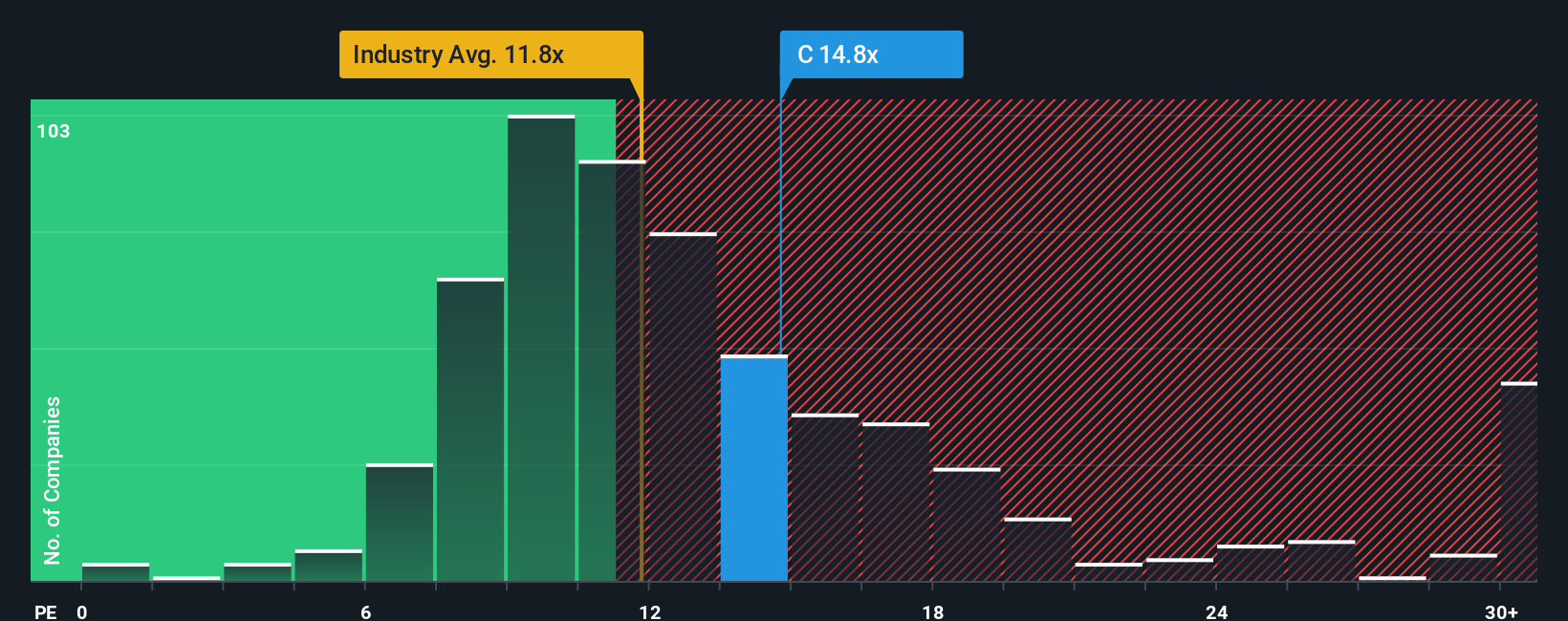

Our DCF work sees Citigroup as undervalued, yet its 15.5x P/E sits above both the US Banks industry at 12x and peers at 13.6x, and only slightly below a 17.2x fair ratio. If growth does not keep pace, is this multiple giving you much margin for error?

Build Your Own Citigroup Narrative

If parts of this story do not quite fit how you see Citigroup, you can stress test the numbers yourself and build a version that reflects your own assumptions, then Do it your way and put your view on the record in just a few minutes.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Citigroup.

Looking for more investment ideas?

If Citigroup has sharpened your thinking, do not stop here. Broaden your watchlist with a few focused ideas that other investors may be overlooking.

- Target resilience by scanning companies that show up in our 81 resilient stocks with low risk scores, where lower risk scores can help you sleep better at night.

- Hunt for mispriced quality with the 55 high quality undervalued stocks, a curated set of stocks our filters flag as having strong fundamentals at undemanding prices.

- Spot early opportunities with the screener containing 25 high quality undiscovered gems, which highlights lesser known businesses that still clear solid financial quality checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.