Countdown to Bank of Japan Rate Hike! Will US Stocks Face Another Crash Like in 2024?

S&P 500 index SPX | 0.00 | |

NASDAQ IXIC | 0.00 | |

ETF-S&P 500 SPY | 0.00 | |

PowerShares QQQ Trust,Series 1 QQQ | 0.00 | |

Microsoft Corporation MSFT | 0.00 |

The Bank of Japan (BOJ) is widely expected to raise its benchmark interest rate this Friday, marking the highest level in three decades. However, market participants remain cautious about the possibility of a repeat of the crush scenario from August 5, 2024, when the sudden strengthening of the yen triggered a sharp unwinding of carry trades, leading to a global sell-off in risk assets. On that day, the S&P 500 index(SPX.US) dropped 3%, while the NASDAQ(IXIC.US) fell 3.4%.

Fortunately, fears of such a panic have significantly subsided. The market has almost fully priced in a 25-basis-point rate hike, shifting the focus from "whether the BOJ will hike rates" to "what comes next." Investors are now keenly watching whether the BOJ will provide clarity on the endpoint of its policy normalization. More importantly, attention is turning to how this policy shift is reshaping investment strategies.

Rate Hike Green Light, but Uncertainty Over Policy Path Looms

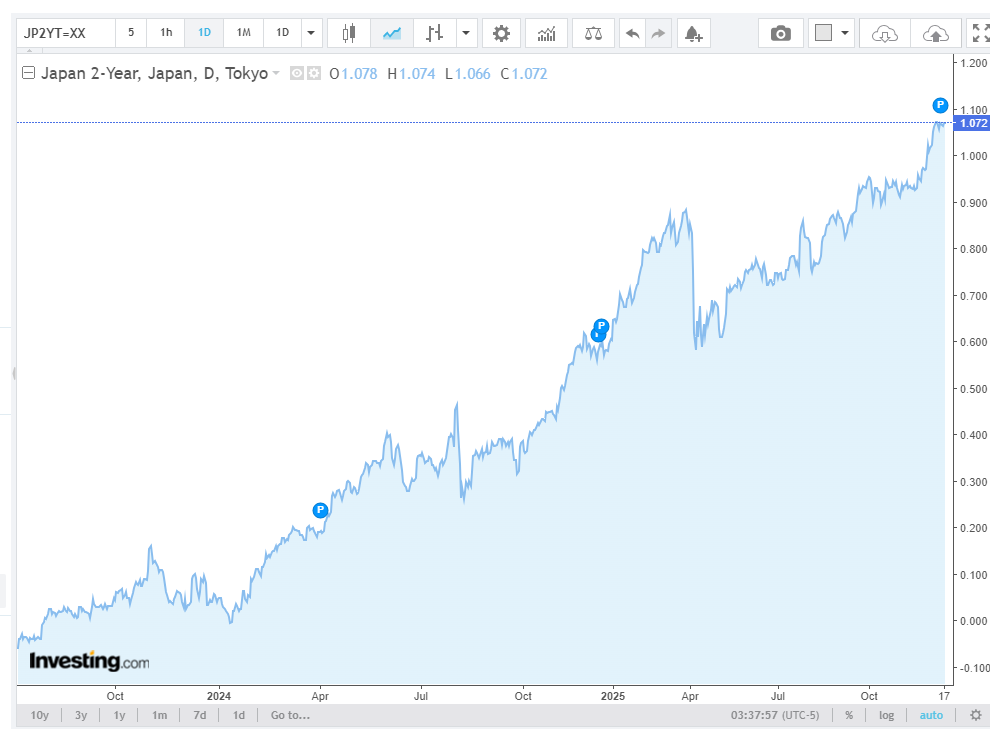

From a macroeconomic perspective, conditions for a rate hike are firmly in place. The BOJ's policy rate is expected to rise to 0.75%. While this figure may seem modest compared to global standards, for Japan, it represents a historic shift—the first in 30 years—and an unprecedented move for many market participants.

Supporting this decision are two key factors: a notable easing of economic downside risks and unprecedented optimism in corporate wage negotiations. Reports suggest that despite rising cost pressures, Japanese companies are steadily advancing discussions for wage increases during the 2026 fiscal year "Shunto" negotiations, reinforcing a virtuous cycle between wages and prices. This structural resilience enables the BOJ to proceed with monetary normalization with confidence, without jeopardizing the pace of economic recovery.

Limited Market Impact as Rate Hike Already Priced In

Despite the significance of the rate hike, its immediate impact on markets may be limited. Recent U.S. non-farm payroll data for November has alleviated recession fears but does not signal a full economic landing, keeping the Federal Reserve on track for further rate cuts. Against this backdrop, the BOJ's decision alone is unlikely to trigger major market moves, as anticipation of the hike has already been baked into asset prices.

For weeks leading up to Friday's meeting, BOJ officials have been signaling the likelihood of a rate hike. On December 1, BOJ Governor Kazuo Ueda mentioned that the central bank would make an "appropriate judgment" on whether to raise rates, while other policymakers have made comments widely interpreted as preparatory steps. Meanwhile, Japanese media outlets have reported extensively on the matter, with the Nikkei's online edition stating on December 16 that the market has priced in a 95% probability of a rate hike.

The real point of contention lies in viewing this as a milestone rather than the endpoint. The market currently prices the terminal rate for this rate hike cycle at around 1.5%.

In this context, the key focus should be on the BOJ's willingness to continue raising rates. Questions arise about how long the hikes will continue and what the ultimate rate might be. If Governor Ueda's post-meeting remarks lean dovish, the market may interpret this hike as a "conclusion." Additionally, given the market's aggressive expectation of a 1.5% terminal rate, the BOJ may intentionally leave room for ambiguity. They might describe the neutral rate as a "rough reference range," emphasizing uncertainty to avoid prematurely committing to a path. A hasty commitment to a hawkish stance could unexpectedly tighten financial conditions, disrupting the recovery.

For U.S. equity investors, this "strategic ambiguity" could be beneficial. As long as the BOJ confirms economic strength while not rushing to 1.5%, it can prevent a sharp yen appreciation, avoiding another violent unwinding of carry trades.

Carry Trade Winds Down: Investment Strategies for 2026

Japan's long-standing low-interest-rate environment has served as a global "anchor" for financing costs. With the significant interest rate differential between the U.S. and Japan driving yen depreciation, hedge funds and other institutions have frequently engaged in "yen carry trades" by borrowing yen for overseas investments.

The mechanism is straightforward: Japan raises rates → Yen borrowing costs rise + Yen strengthens → Leveraged investors are forced to sell profitable positions to repay debt → Risk assets come under pressure. This scenario played out in July 2024 when an unexpectedly hawkish signal spiked the VIX, causing a pullback in the "Magnificent Seven" U.S. stocks and cryptocurrencies like Bitcoin.

The Path Ahead for the BOJ:

Scenario A: Gradual Rate Hikes Every Six Months (Safe Mode)

This is the current market expectation. If the next rate hike is delayed until June 2026, the market will have ample time to adjust. The slow unwinding of carry trades will keep volatility manageable, with limited pressure on high-beta assets.

According to a Bloomberg survey conducted from December 5 to 10, 64% of 50 economists expect rate hikes "approximately every six months" after 2026, while 21% anticipate "approximately once a year." The median forecast for the BOJ's "neutral rate" is around 1.5%.

Scenario B: Accelerated Tightening Due to Yen Weakness (Risky Mode)

If persistent yen weakness forces the BOJ to act sooner, such as another rate hike by April 2026, and the BOJ adopts a hawkish stance, the yen may appreciate. This could trigger the "worst-case scenario" for the market, similar to the "Ueda Shock" in August 2024, where high-leverage tech stocks and cryptocurrencies could face liquidity crunches.

Options Strategies for Investors:

For investors heavily positioned in high-volatility U.S. equities and concerned about potential market disruptions from BOJ rate hikes or CPI data, options can provide protection. This strategy is akin to buying insurance for your portfolio. By purchasing an out-of-the-money put option alongside your stock holdings, you can offset some losses if stock prices drop significantly. The put option allows you to sell the stock at a predetermined price, capping potential losses. If extreme scenarios don't occur, the only cost is the option premium.

For risk-tolerant investors, end-of-day options trading around key macro events can be advantageous. Exchanges offer daily expiration options for highly liquid ETFs like the ETF-S&P 500(SPY.US) and the PowerShares QQQ Trust,Series 1(QQQ.US). Investors can deploy strategic options based on market expectations. If the BOJ's actions suggest a softer approach, a market rebound is possible.

Top Picks for 2026: From "Storytelling" to "Earnings Reports"

The liquidity pullback initiated by Tokyo underscores the main investment theme for institutional players in 2026: shifting away from speculative growth fueled by cheap funding and toward "quality assets" with real cash flow and strong balance sheets.

Morgan Stanley Advocates a "Flight to Quality": In a rising rate environment, low-leverage giants like Microsoft Corporation(MSFT.US) and Apple Inc.(AAPL.US), along with financial institutions benefiting from a steeper yield curve like JPMorgan Chase & Co.(JPM.US) and Morgan Stanley(MS.US), will act as stabilizers. They even recommend overweighting software while underweighting hardware to reduce volatility.

JPMorgan & Wells Fargo Shift Focus in AI: Instead of solely focusing on chipmakers, they suggest pivoting toward the "utilities" of AI infrastructure—companies like BLOOM ENERGY CORP(BE.US) (data center power), Seagate Technology PLC(STX.US) (data storage), and Celestica Inc.(CLS.US) (servers). These firms are driven by tangible demand rather than liquidity-driven bubbles.

Bank of America Stays Loyal to Core AI Factories: NVIDIA Corporation(NVDA.US), Broadcom Limited(AVGO.US), Lam Research Corporation(LRCX.US), and KLA-Tencor Corporation(KLAC.US) remain irreplaceable winners in capital expenditures. Despite their high valuations, their order visibility is strong.

Goldman Sachs Bets on "Middle-Class Consumption Recovery": They predict that real wages will finally outpace inflation in 2026, favoring companies like TJX Companies, Inc.(TJX.US), Ross Stores, Inc.(ROST.US), NIKE, Inc. Class B(NKE.US), Starbucks Corporation(SBUX.US), and Royal Caribbean Cruises Ltd.(RCL.US), which cater to experience-based spending.

The BOJ's rate pivot may signal that the global liquidity cycle's final line of defense is shrinking. Beyond the expected rate hike, the market's greater fear lies in unclear paths and unexpected hawkishness. As the cheapest funding currency begins to "charge," leveraged "castles in the air" may be the first to shake. Investors will need to make more cautious and deliberate decisions.