Datadog (DDOG) Valuation Reassessed As AI Agent Fears Pressure Software Stocks

Datadog DDOG | 124.61 | +2.93% |

AI agent fears hit Datadog as markets reassess software stocks

The latest AI model releases from Anthropic and OpenAI have sharpened worries that autonomous agents could replace traditional software. As a result, Datadog (DDOG) and its recurring revenue model are under closer investor scrutiny.

Datadog’s share price has been under pressure despite the latest AI headlines, with a 7 day share price return decline of 13.63% and a 90 day share price return decline of 44.08%, while the 3 year total shareholder return of 38.71% still reflects a stronger longer term outcome than the 1 year total shareholder return decline of 21.7%. This suggests momentum has been fading as investors reassess growth and risk around AI agents and software spend.

If you are weighing how AI agents might reshape the software space, it could be a moment to scan 56 profitable AI stocks that aren't just burning cash and see which names pair AI exposure with current earnings power.

With Datadog trading at a discount to analyst targets and screens suggesting intrinsic value above the current US$111.69 share price, the key question is whether this weakness has opened an opportunity or if the market already sees future growth clearly.

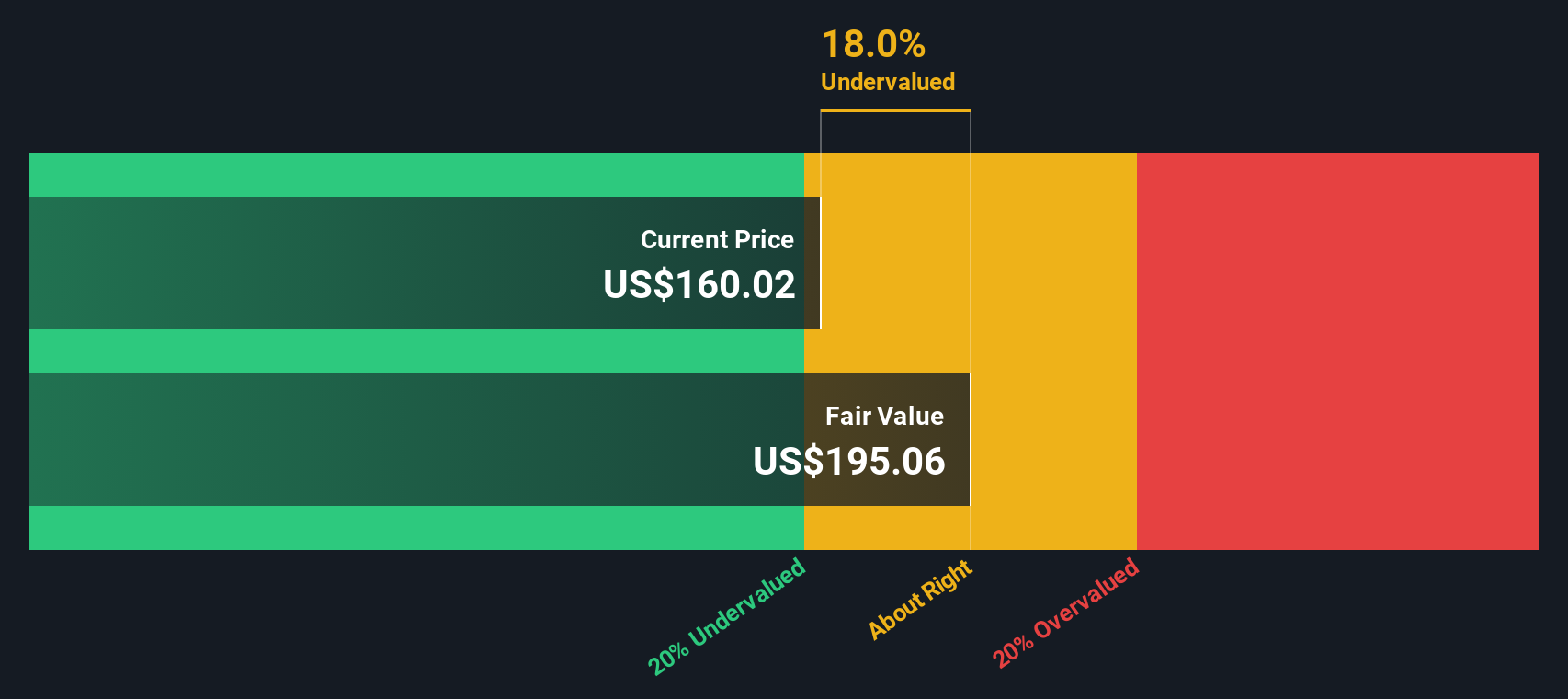

Most Popular Narrative: 46.4% Undervalued

Datadog’s most followed narrative pins fair value at about $208.49 per share versus the latest $111.69 close, setting up a sharp gap between model and market.

Analysts have trimmed their Datadog fair value estimate to about US$208 from roughly US$212, reflecting lower price targets that factor in competitive pricing pressure after Palo Alto Networks' Chronosphere deal and a reset in multiples, even as recent research still highlights strong Q3 execution, renewed OpenAI commitments, and ongoing AI related demand as key supports for the story.

Curious what justifies that gap between price and fair value? The narrative leans on double digit growth, rising margins, and a punchy future earnings multiple to get there.

Result: Fair Value of $208.49 (UNDERVALUED)

However, that upside view sits alongside real pressure points, including rising competition on pricing and the risk that a few large AI customers cut back spending.

Another Angle on Valuation

While the popular narrative references a fair value of about US$208.49 per share, our DCF model indicates an estimate of US$218.82. This compares with the current US$111.69 price and also screens as undervalued. When both views align in this way, the key question is which set of cash flow assumptions you are most comfortable with.

Build Your Own Datadog Narrative

If the current fair value views do not fully line up with how you see Datadog, you can put the data to work yourself and build a custom story in just a few minutes, then Do it your way.

A great starting point for your Datadog research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Datadog has you thinking harder about where you put your money, do not stop here. Broaden your watchlist now so you do not miss potential standouts.

- Spot potential value opportunities early by checking out 53 high quality undervalued stocks that pair solid fundamentals with pricing that still looks reasonable on the numbers.

- Prioritise staying power by reviewing solid balance sheet and fundamentals stocks screener (45 results) where financial strength and resilience are front and center.

- Hunt for off the radar potential by scanning our screener containing 24 high quality undiscovered gems before they land on every other investor's screen.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.