DexCom (DXCM) Could Be 10% Overvalued As Recall Adds Fresh Questions

DexCom, Inc. DXCM | 0.00 |

DexCom (DXCM) has drawn fresh attention after voluntarily initiating a Class II recall of certain Dexcom G7 sensor lots that were stolen during the destruction process and later entered unauthorized distribution channels.

Beyond the recall, DexCom’s share price has stayed resilient, with a 17.09% 90 day share price return and a 12.65% year to date share price return, even as the 1 year total shareholder return is down 10.09%. This points to momentum rebuilding after a weaker multi year stretch.

If this kind of healthcare story has your attention, it could be a good time to see what else is emerging in the sector through the 41 healthcare AI stocks.

After a sharp rerating and a recall that puts execution under the spotlight, the real test for DexCom now sits in the price tag. Does the current valuation still leave enough upside to justify fresh risk?

Most Popular Narrative: 10.3% Overvalued

At a last close of $74.96 versus a narrative fair value of $67.93, DexCom is framed as carrying a premium that rests heavily on execution in continuous glucose monitoring for wider patient groups.

Although broader commercial coverage for type 2 diabetes patients not using insulin, including more than 6 million covered lives across large PBMs and an expected expansion to over 7 million with Prime Therapeutics, supports a larger addressable base, future revenue growth still depends on converting the roughly two thirds of covered patients who are not yet using CGM. This may cap near term growth if adoption remains slow relative to coverage additions, with a knock on effect for earnings.

The heart of this DexCom narrative is simple: higher coverage, cautious margins, and a premium future earnings multiple. Curious which growth and profitability assumptions actually justify that stance? The full story spells out how revenue, earnings and valuation are expected to line up.

Result: Fair Value of $67.93 (OVERVALUED)

However, DexCom’s story could look different if broader Type 2 coverage leads to faster CGM adoption or if CMS reimbursement arrives with fewer constraints than cautious analysts assume.

Another View: DexCom Through a Cash Flow Lens

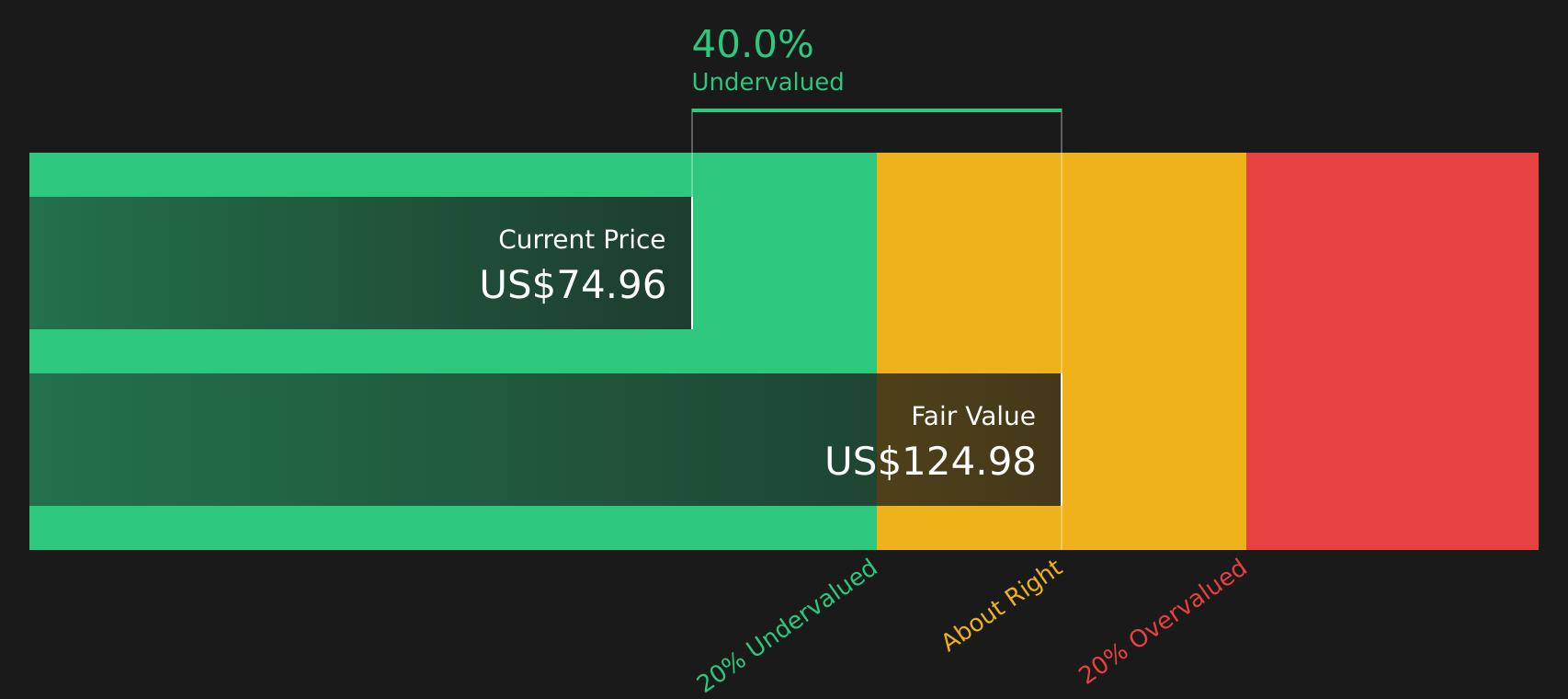

The bearish narrative pegs DexCom as 10.3% overvalued at $74.96 versus a $67.93 fair value, but the SWS DCF model points in the opposite direction. On that approach, DexCom is trading at $74.96 compared with an estimated future cash flow value of $124.79, which frames the stock as 39.9% below that fair value. When two models disagree this sharply, which set of assumptions do you trust more?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out DexCom for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of caution and opportunity around DexCom leaves you undecided, quickly review the numbers that matter most for you and see the 3 key rewards

Looking for more investment ideas beyond DexCom?

Once you have a view on DexCom, consider exploring additional opportunities. Use powerful stock filters to find other investments that match your risk tolerance and return objectives.

- Seek potential upside by scanning for companies that appear priced below what their quality and fundamentals suggest using the 44 high quality undervalued stocks.

- Emphasize stability by searching for companies with strong finances and durable operations through the 76 resilient stocks with low risk scores.

- Look for lesser known stocks with solid financial profiles via the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.