Duolingo (DUOL) Falls Ahead Of Earnings As Valuation Debate Heats Up

Duolingo, Inc. DUOL | 0.00 |

Why Duolingo Stock Is Back in Focus Ahead of Earnings

Duolingo (DUOL) is drawing attention after the stock fell 9.24% in the latest session, as investors react to forecasts of lower year-over-year earnings per share in spite of expectations for higher revenue.

The recent 9.24% one day share price drop has come after a strong 90 day share price return of 29.08%, while the year to date share price return is down 31.16% and the 1 year total shareholder return has fallen 70.46%. This suggests momentum has recently cooled as investors reassess Duolingo’s earnings outlook against its revenue trajectory.

If Duolingo’s recent swing has you rethinking where growth might come from next, it could be a good time to scan for other opportunities in education focused and consumer technology, starting with 20 top founder-led companies

With Duolingo now trading around $121.49, carrying an intrinsic discount of about 57% yet sitting below the average analyst price target, you have to ask: is this a genuine undervaluation, or is the market already pricing in future growth?

Most Popular Narrative: 6.1% Overvalued

According to the most followed Duolingo narrative, the fair value sits at $114.49, slightly below the last close at $121.49, which raises questions about how much of the story is already reflected in the price.

Running it through the numbers, the quick ratio sits at ~2.0x with $1.1 billion cash on hand and minimal debt, this company is not going anywhere. The long-term PEG ratio normalises to around 1.1x by 2027/28 estimates, well below the 2.0 threshold that signals reasonable growth-adjusted value.

The fair value in this narrative hinges on how Duolingo converts that cash rich balance sheet and current profitability into future earnings power. Want to see which growth, margin and valuation assumptions sit underneath that $114.49 figure and why they still point to an overvaluation at today’s price, even after the recent share price slide?

Result: Fair Value of $114.49 (OVERVALUED)

However, Duolingo’s Vision 2026 spending plans and rising AI competition could pressure margins or slow user monetisation, which would quickly challenge this narrative of overvaluation.

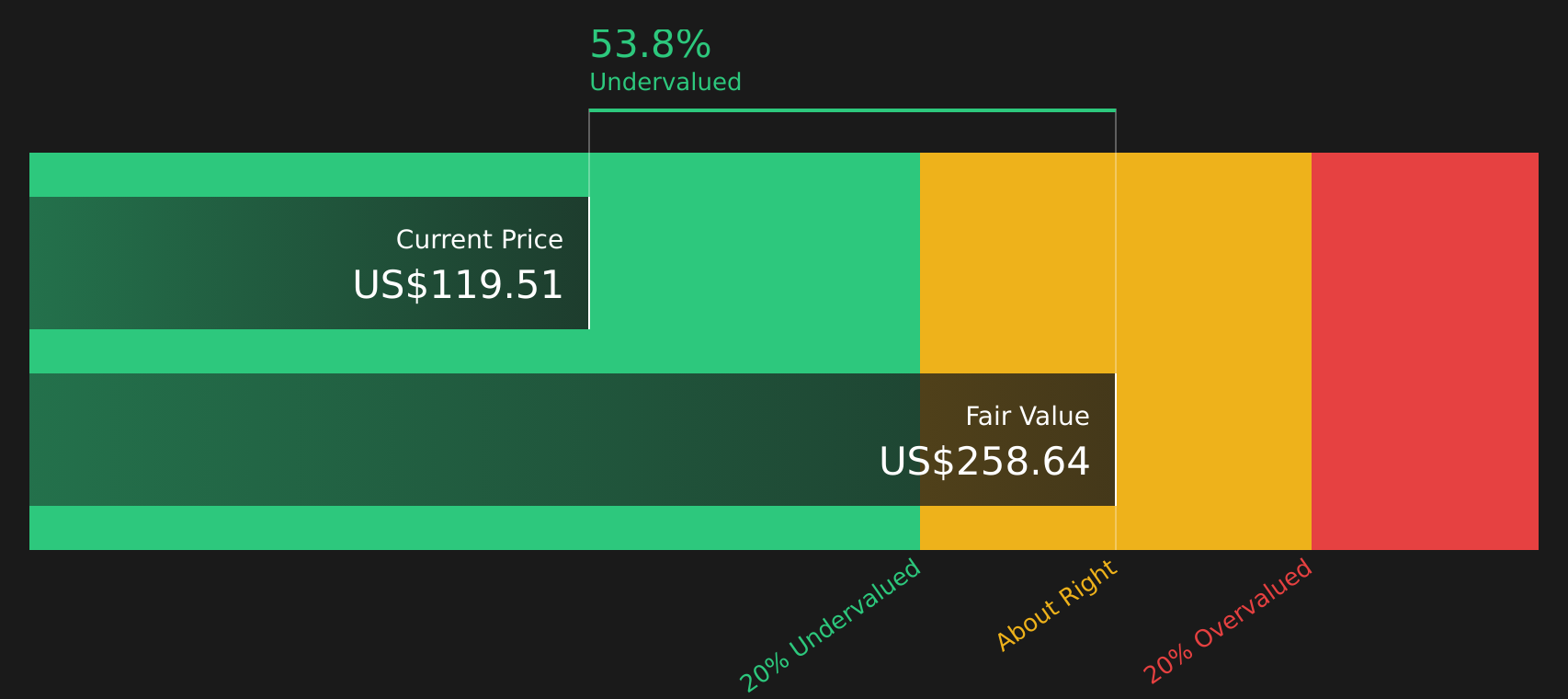

Another View: SWS DCF Signals Deep Undervaluation

The user narrative has Duolingo trading around 6.1% above a fair value estimate of $114.49, yet our DCF model presents a very different picture. With Duolingo at $121.49 and the SWS DCF fair value at $282.50, the stock appears heavily undervalued. This raises a clear question for you to weigh: are earnings fears too dominant in the current price?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Duolingo for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If you are unsure whether the Duolingo story leans more toward concern or opportunity right now, consider acting while sentiment is mixed by evaluating both sides through 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Duolingo?

If Duolingo has sharpened your appetite for opportunities, do not stop here. Use targeted stock lists to quickly spot ideas that better match your risk and income goals.

- Target potential mispricings by scanning companies that combine quality and value through the 44 high quality undervalued stocks.

- Build a steadier income stream by focusing on companies offering robust payouts with the 8 dividend fortresses.

- Sleep easier at night by concentrating on resilient companies screened using the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.