e.l.f. Beauty (ELF) Stock Looks Above Fair Value While Sales Stay Strong

e.l.f. Beauty, Inc. ELF | 0.00 |

After a strong five year run that has left e.l.f. Beauty stock up more than threefold, the current valuation looks stretched based on the company’s low value score and an overvalued read from market multiples. Recent short term gains have come against a backdrop of mixed sentiment around earnings expectations and governance, which keeps the pricing of e.l.f. Beauty in sharp focus for investors.

- Over the past 5 years, e.l.f. Beauty has returned about 201%, which puts extra attention on whether today’s share price still offers a comfortable margin for error.

- On the upside, ongoing revenue growth and an expanding multi brand portfolio may support higher expectations. However, an investigation into potential fiduciary duty breaches by certain officers introduces governance risk that can weigh on how much investors are willing to pay.

- With a value score of 0 out of 6 checks, the stock currently screens as expensive rather than a clear bargain on the broader valuation tests.

The issue now is whether e.l.f. Beauty’s recent share price recovery is already pricing in the growth story, or if there is still room for upside before valuation becomes a binding constraint.

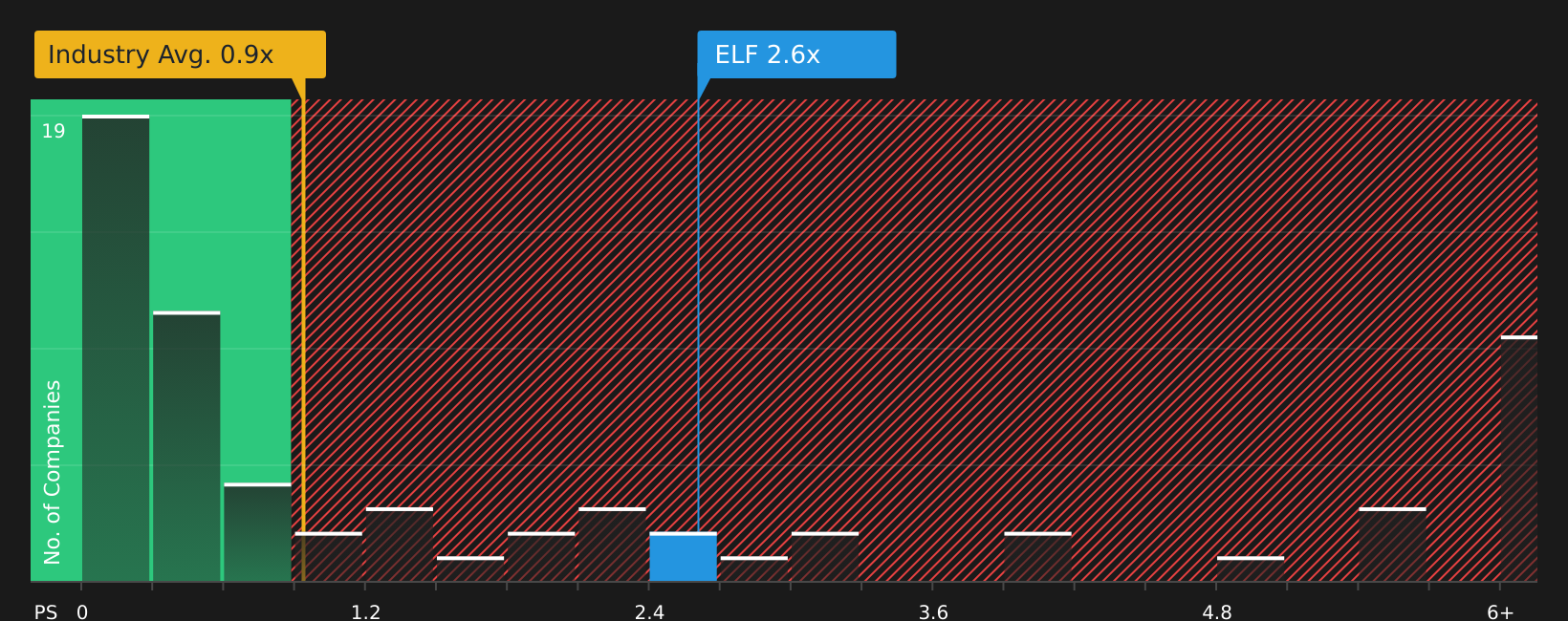

Does e.l.f. Beauty Look Pricey on Sales?

P/S is a useful yardstick for e.l.f. Beauty because the company’s story is closely tied to revenue scale and brand reach rather than current earnings alone.

Right now, e.l.f. Beauty trades on a P/S of 2.7x, compared with an industry average of about 0.9x for Personal Products and a peer group average of roughly 2.2x. That already places the stock at a clear premium to both the broader sector and closer listed peers on a simple sales basis.

The fair P/S ratio implied by the model is 1.7x. This reflects what investors might typically pay for e.l.f. Beauty given its margins, growth profile, size, and risk factors. With the current P/S sitting well above that level, the shares screen as overvalued on this measure, even though recent news highlights ongoing revenue growth and product expansion.

On the P/S multiple, e.l.f. Beauty stock currently looks overvalued relative to both its fair ratio and sector yardsticks.

The e.l.f. Beauty Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for e.l.f. Beauty pick up where the valuation question leaves off. They spell out which combinations of future growth, margins and earnings would need to hold for e.l.f. Beauty's stock to be worth meaningfully more or less than it is today, and they sit on the company’s Community page. Each narrative links a specific set of potential catalysts and risks to one clear fair value view, so you can see over time which storyline is tracking closer to reality.

The community is sharply split on e.l.f. Beauty, with one camp seeing meaningful upside potential and another arguing expectations already look full.

Bull case: 51% undervalued

"Especially with their acquisition of Rhode, not necessarily because of the revenue it will generate, but more so because of the brand and reputation they have acquired, especially with how Hailey Bieber will now work to help promote ELF…"

Bear case: roughly fairly valued

"Heavy reliance on Chinese manufacturing, tariff risks, and competitive pressures threaten margins, revenue growth, and market share if mitigation and expansion strategies fall short…"

Do you think there's more to the story for e.l.f. Beauty? Head over to our Community to see what others are saying!

The Bottom Line

For now, e.l.f. Beauty screens as overvalued on simple sales multiples, with the current P/S sitting well above the model’s fair ratio and sector averages. That does not rule out further gains; however, it does mean the valuation case rests more on confidence in the growth story than on a margin of safety. The key debate from here is whether e.l.f. Beauty can keep delivering the brand reach and revenue scale that bulls expect, while addressing governance concerns so that today’s premium does not turn into a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.