The US Labor Department is set to release the highly anticipated January nonfarm payrolls report and unemployment rate on Wednesday, February 11, 2026, at 04:30 PM, Riyadh Time.

This report is exceptionally significant as it will include the annual benchmark revision to the establishment survey data, which is expected to dramatically alter the landscape of US job growth throughout 2025.

Also will released are the following gauges:

Time (Riyadh)

Event

Previous

Consensus

Forecast

04:30 PM

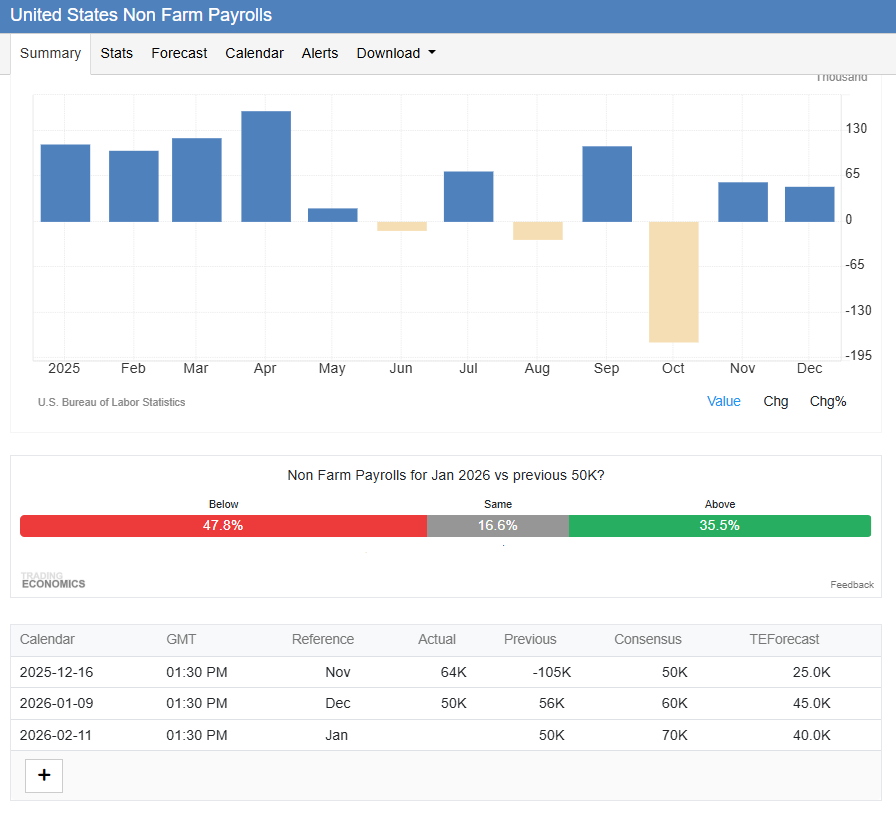

Non-Farm Payrolls JAN

50K

70K

40K

04:30 PM

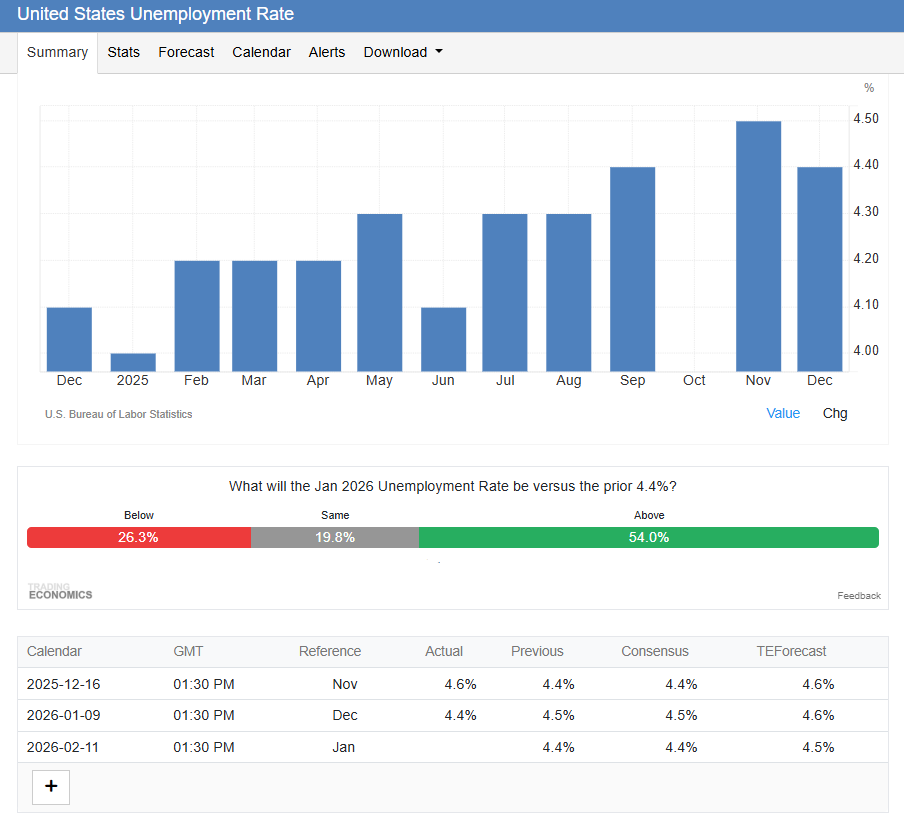

Unemployment Rate JAN

4.4%

4.4%

4.5%

04:30 PM

Average Hourly Earnings MoM JAN

0.3%

0.3%

0.3%

04:30 PM

Average Hourly Earnings YoY JAN

3.8%

3.6%

3.8%

04:30 PM

Participation Rate JAN

62.4%

62.3%

04:30 PM

Average Weekly Hours JAN

34.2

34.2

34.2

04:30 PM

Government Payrolls JAN

13K

8.0K

04:30 PM

Manufacturing Payrolls JAN

-8K

-5K

-10.0K

04:30 PM

Nonfarm Payrolls Private JAN

37K

70K

32.0K

04:30 PM

U-6 Unemployment Rate JAN

8.4%

8.5%

The broader narrative for 2025 has been one of a "low hiring, low firing" environment, with the year potentially recording the weakest job growth since 2020, excluding the pandemic period.

This slowdown occurs amidst a unique economic backdrop described by the White House and the Federal Reserve as a "challenging and quite unusual situation" where slowing labor force growth, partly due to restrictive immigration policies, coincides with rising productivity.

02

Expectations, Interpretation

Market consensus, as gathered by Bloomberg, expects January payrolls to increase by 65,000, which would be the largest gain in four months.

Other surveys point to a median forecast around 70,000.

The unemployment rate is expected to remain stable at 4.4%.

However, forecasts vary widely, from Citi's optimistic 135,000 to Goldman Sachs' more conservative projection of just 45,000 new jobs. Goldman Sachs cites potential drags from updates to the "birth-death" model and weak signals from alternative employment indicators.

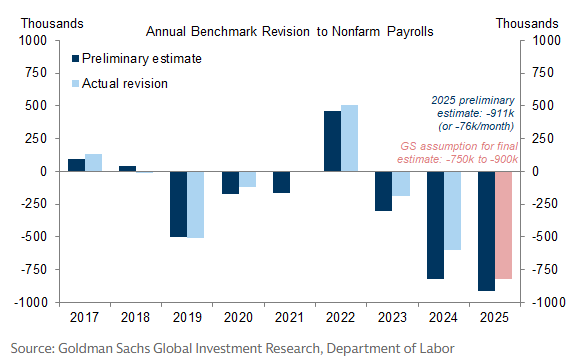

The true spotlight, however, is on the annual benchmark revision.

Preliminary estimates from last September suggested a record downward revision of approximately 911,000 jobs for the period through March 2025.

The final adjustment, to be released tonight, is anticipated to confirm a significant downgrade, with economists forecasting a reduction in the range of 750,000 to 900,000 jobs for that period.

Furthermore, subsequent revisions for the months from April through December 2025 could erase an additional 100,000 jobs, leading to a scenario where the previously reported meager job growth for 2025 is entirely wiped out. This has led to warnings, echoed by Fed Governor Waller, that the data may show job growth was nearly zero last year.

The key to interpreting the report will be distinguishing between supply and demand factors.

As emphasized by White House National Economic Council Director Kevin Hassett, weak job growth could stem from a shrinking labor supply rather than weak economic demand, a distinction that carries vastly different implications for Fed policy. A supply-constrained market could signal inflationary pressures, while a demand-constrained one would build the case for more aggressive rate cuts.

Many analysts argue that the unemployment rate remains the most critical real-time indicator to watch, as it may more clearly reflect the actual health of the labor market.

03

Impact on Stock Sentiment

The equity market's reaction will hinge less on the headline January number and more on the narrative shaped by the revisions and the subsequent Fed policy expectations.

A report that confirms a significant downward revision to past data, coupled with a soft January reading, would likely solidify market expectations for imminent Federal Reserve easing.

This scenario has already triggered a pre-emptive response:

The US dollar has weakened for four consecutive sessions as investors increase bets on Fed rate cuts.

For stocks, this could be a double-edged sword.

On one hand, lower interest rates are generally supportive of equity valuations, particularly for rate-sensitive sectors and growth-oriented tech stocks. A "dovish" interpretation of the data could extend the market's rally, potentially fueling a rotation into previously lagging sectors.

On the other hand, if the revisions paint a picture of an economy that is substantially weaker than previously believed, concerns about corporate earnings and a potential recession could outweigh the positive impetus from rate cut hopes. This could introduce volatility and lead to a risk-off sentiment.

The market's ideal outcome, as noted by analysts, would be a "goldilocks" number—soft enough to justify Fed support but not so weak as to spark fears of an imminent downturn.

Ultimately, traders will parse the data to assess whether the labor market is in a "gradual cooling" phase, which supports a soft landing narrative, or on the brink of a more severe deterioration. The reaction in the bond market, particularly the shape of the yield curve, will be a critical indicator for equity sector performance.

In a climate where the US dollar is already under pressure, the nonfarm payrolls report could be the catalyst that determines the next major directional move for US stocks.